MTHEL131 Lecture Notes - Lecture 12: Retirement Age, Kijiji, Pension

12 Mar 2014

School

Department

Course

Professor

Document Summary

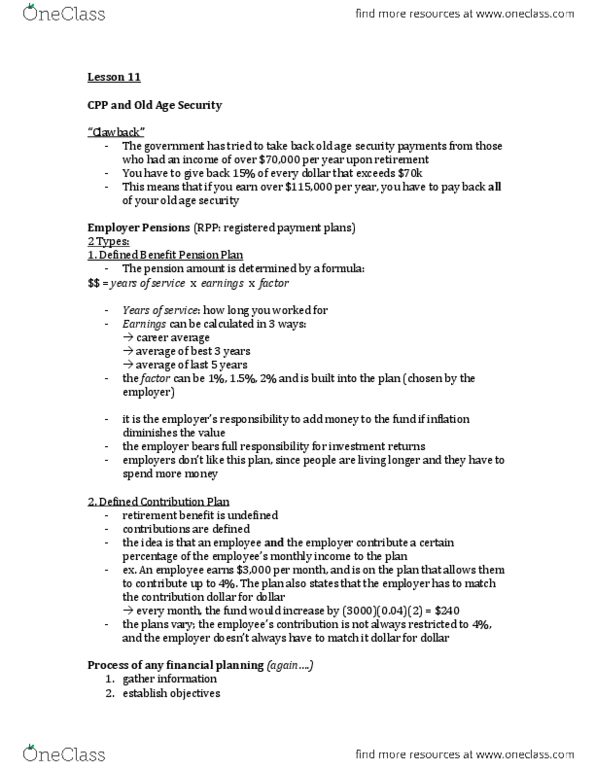

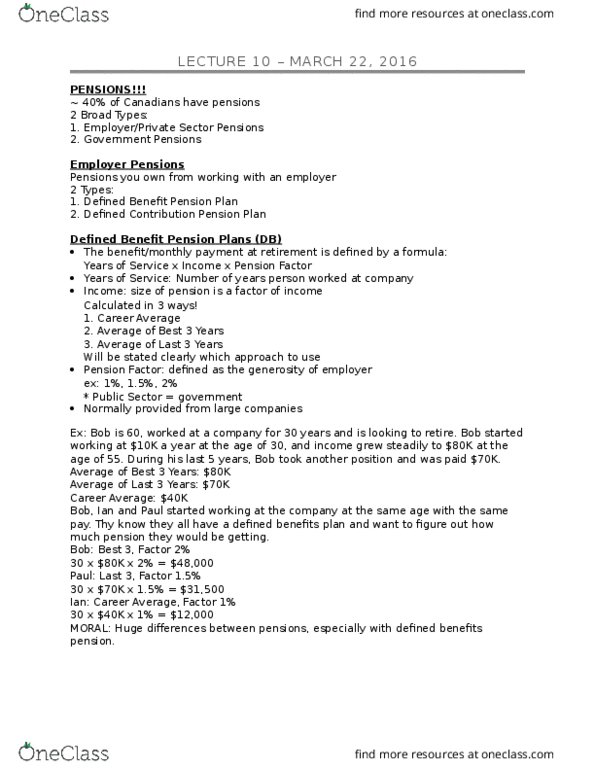

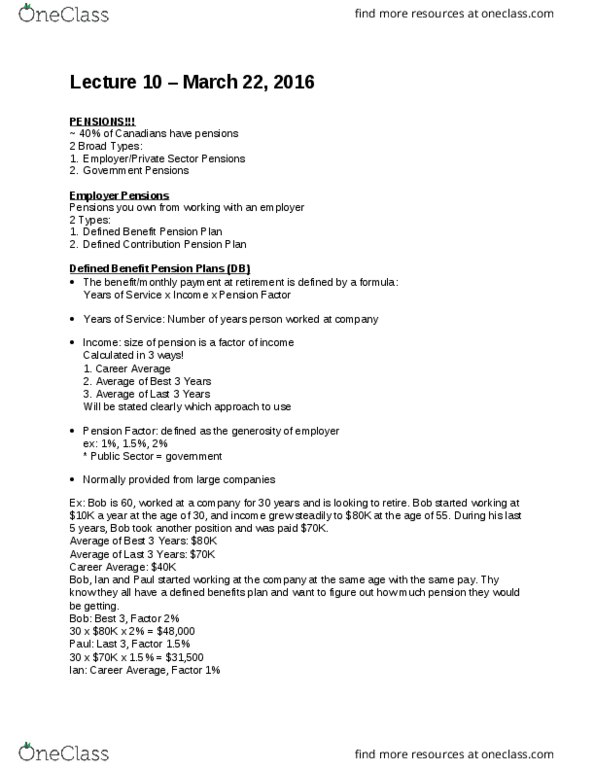

Government thought there was an opportunity to save my money by taking away oas from high earnings seniors. Job seekers should look at rpp to decide where they want to work. 2 types: defined benefit pension (db, defined contribution plan (dc) Defined benefit pension plan: pension amount received at retirement defined by a formula, considers, years of service, earnings, factor. Can be calculated in 3 different ways (with variations: career average earnings, ex: ,000, average of best 3 years, ex: ,000, average of last 5 years, ex: ,000. Not all defined benefit plans are equal important to understand your pension. Only the largest employers have defined benefit plans (+100k employees) The employer takes on the full risk of investment returns. Most started in early 60s and 70s (when average age of death was lower) People are living longer, these pensions must be paid for life. Employer takes on risk of longevity (old age)