ECON202 Lecture Notes - Lecture 10: Normal Type, Complementary Good, Socalled

Document Summary

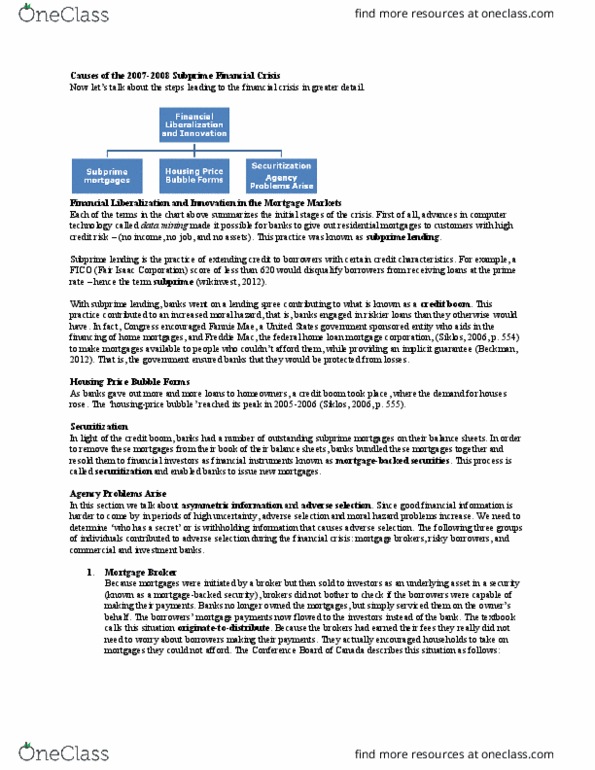

Applied analysis 2. 1: the housing market boom and bust (and boom and bust again in. One part of the story of the 2008-09 recession is the housing market boom and bust in canada and the united states, especially in the united states. Figure aa2. 1. 1 below shows the housing price indices for canada, the united states and. Be careful about the index values: they are indexed to january 2000=100, the fact that the. Saskatchewan values are above the canadian and u. s. values just means that the saskatchewan values have risen more since 2000 than the u. s. or canadian values, not that they are higher in value. The initial housing boom (2002-2006 in the u. s. and somewhat later in canada and. Second, there were strong reductions in the required household income needed to get the loans banks and mortgage companies moved to ninja loans (no income no job or assets) the so-called subprime mortgages.