COMM 455 Lecture 7: C455 - Lecture 7 Notes

Document Summary

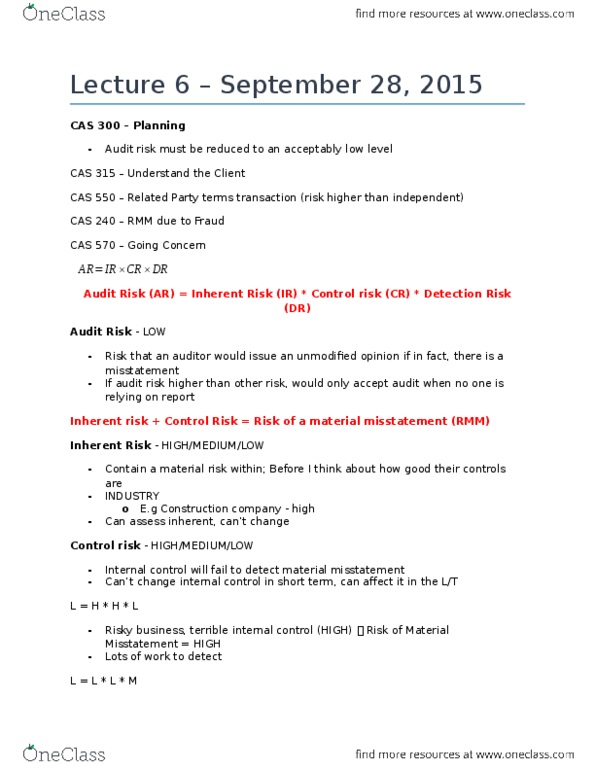

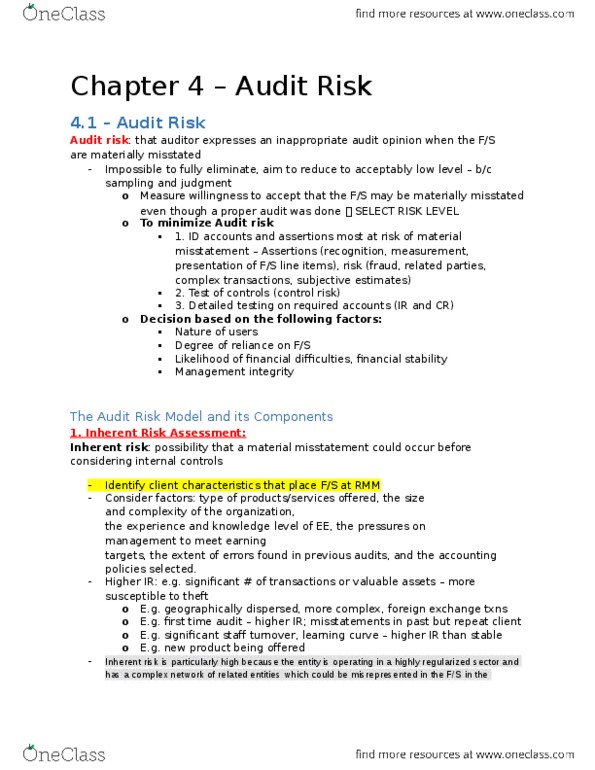

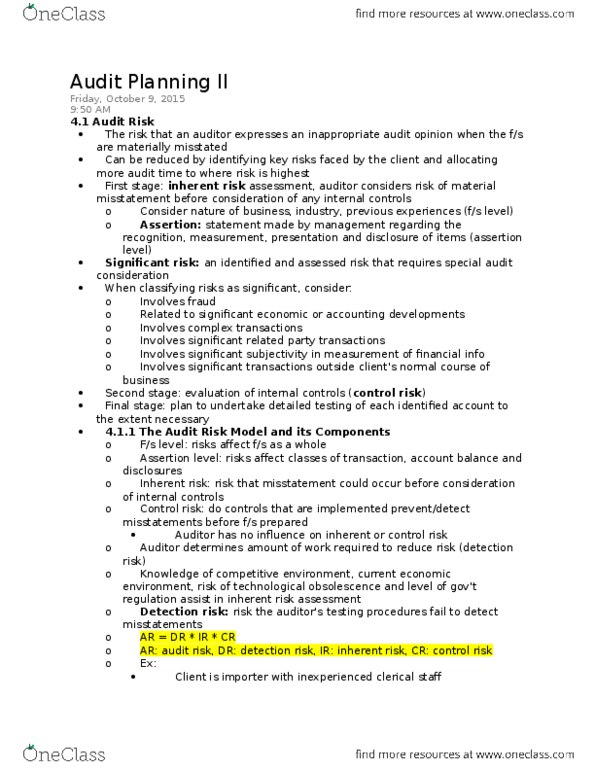

Audit risk (ar) = inherent risk (ir) * control risk (cr) * detection risk (dr) Low, could be medium if no one relying on f/s (rare) Risk of a material misstatement before considering the internal control. Do not have to test control: auditor make assessment and call if they should. Understanding must be obtained: flowcharts e. g. how the document flows through system, internal control questionnaire (icq, narratives. Cycles: walkthrough: take document from inception of transaction to accounting record. Do not rely on internal control, rather expand substantive test (verify account balances) If you can"t rely on control, then expand work you do. Look like they will work not enough to fully rely on them. Controls work if there were errors, likely to be identified and corrected. But does not address whether account balances are right. One amount or aggregate of amounts; all companies different. % of net income before taxes: 5-10% % of assets: 1-2% of total assets.