COMM 353 Lecture Notes - Lecture 15: Debenture, Life Insurance, Canadian Cancer Society

Document Summary

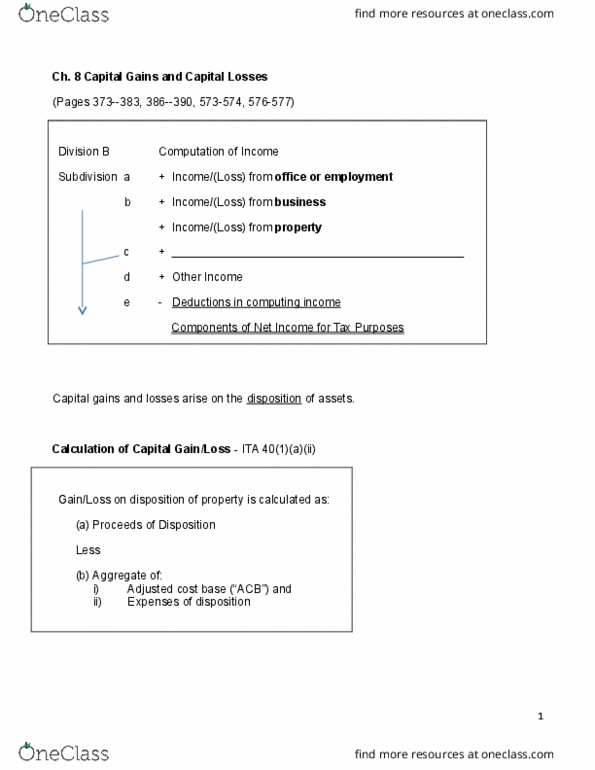

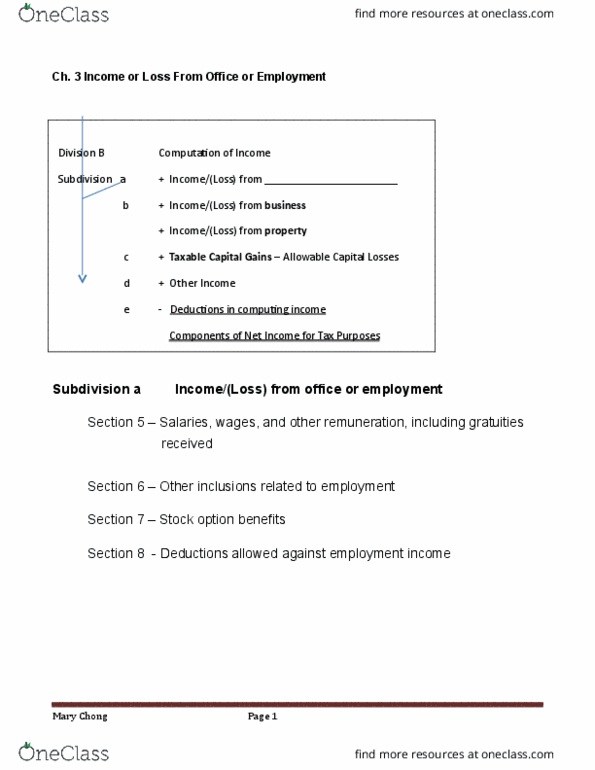

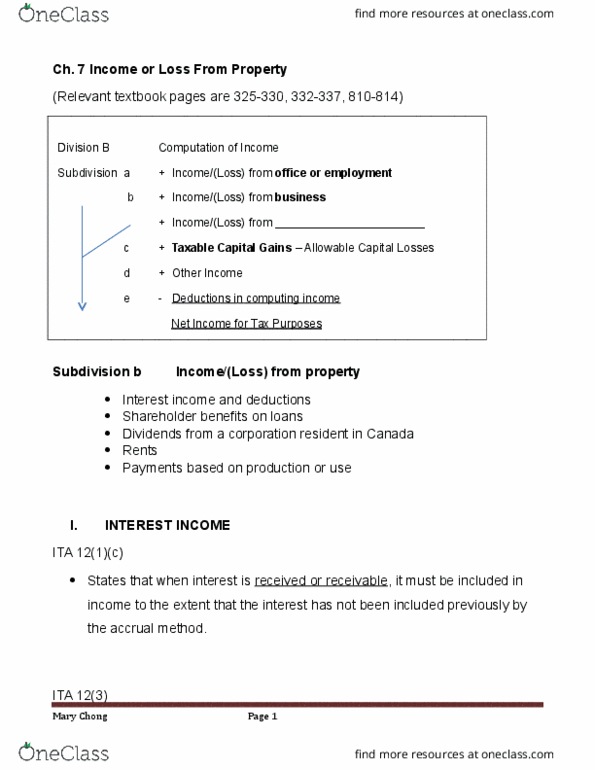

6 income or loss from a business (pages 245-267, 273-277) + taxable capital gains allowable capital losses. Section 18 - deductions - general limitation (purpose test) subject to this part, a taxpayers profit from that business or property for the year. 1/2 of a capital gain is taxable ( taxable capital gain ) 1/2 of a capital loss is deductible ( allowable capital loss ) Note: allowable capital losses can only offset taxable capital gains. 100% of business income is taxable and 100% of business losses are deductible. Business losses (non-capital losses) are deductible against any type of income. Therefore, if there is a gain, taxpayer would prefer __________________. If there is a loss, the taxpayer would prefer - Capital asset - capital asset are acquired and held to produce income through their use. Disposition will give rise to a capital gain/loss.