COMM 455 Lecture Notes - Lecture 9: Stock Transfer Agent, Eaves, Internal Control

Document Summary

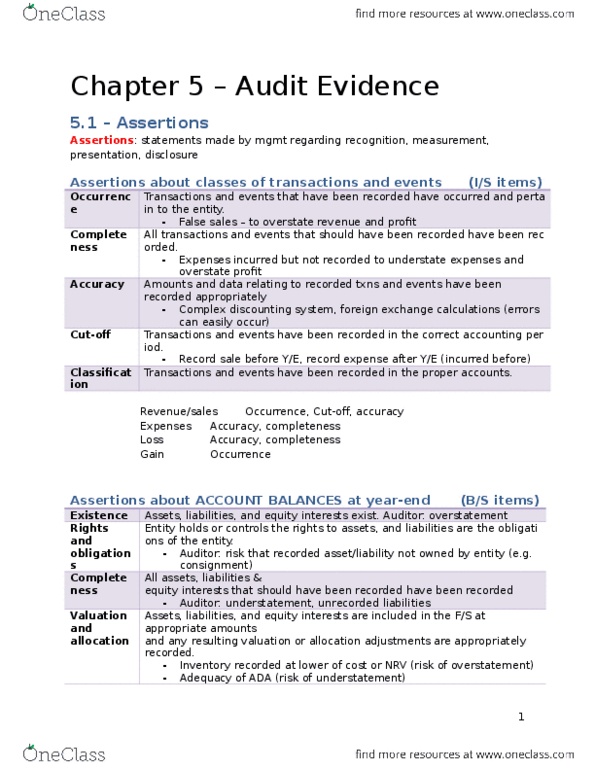

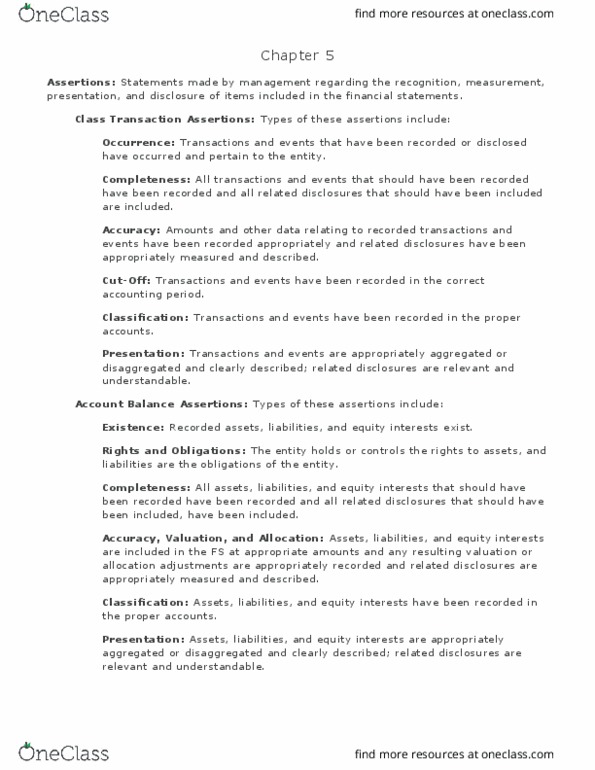

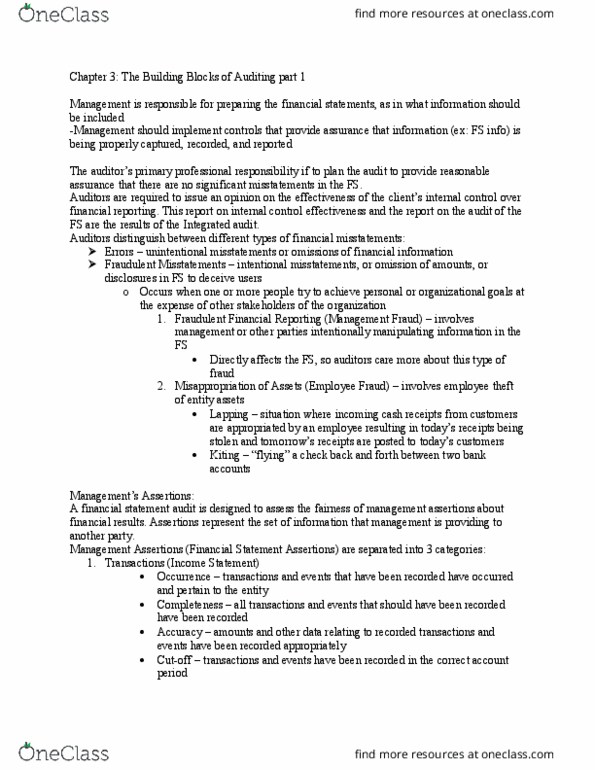

Chapter 1 - 6 for midterm assurance engagement - must be independent non-assurance (compilation) - independence not an issue. Usually - risk in one particular area because controls aren"t proper same assertions for all cycles, but different cycles focus on different assertions sometimes have 1 or 2 most important assertions. Presentation and disclosure: not on exam: but for cpa: all disclosures that should have been included in the f/s have been. Occurrence, rights, obligations: disclosed events and transactions have actually occurred and pertain to the entity classification and understandability disclosures are clearly expressed. Accuracy and valuation: financial information is appropriately presented and described, and, financial information is disclosed fairly and at appropriate amounts. Which assertion most important? (after midterm - what procedure will you do?) Do work when there is risk with assertion every one has a different professional judgement. When you didn"t find something you"re supposed to e. g. revenues - million, test 50.