ECON 301 Lecture Notes - Lecture 16: Marginal Cost, Economic Surplus

Document Summary

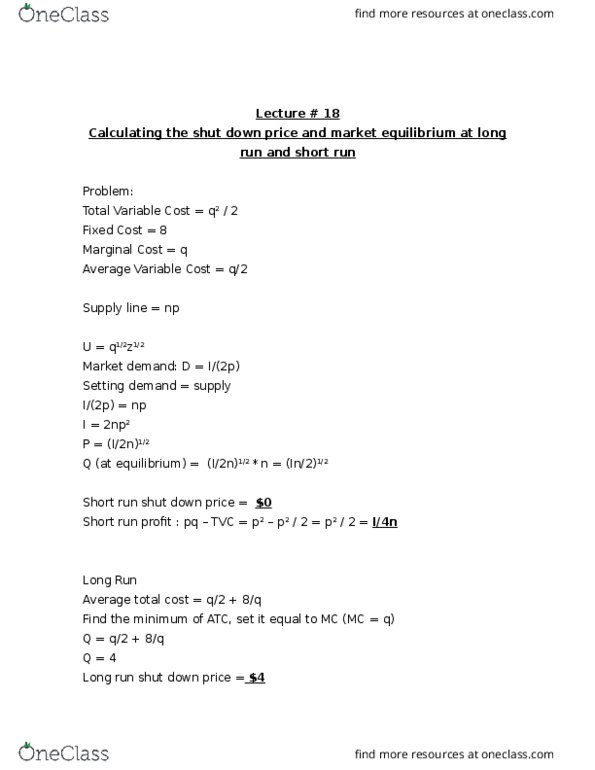

However, deinition of proit is diferent in short and long term. Fixed costs are sunk in the short run, but not in the long run. Short term supply curve = marginal cost above the avc line and 0 below the avc line. Long term supply curve = marginal cost above atc line and 0 below the. Long run shut down price is the minimum of atc. Short run shut down price is the minimum of avc. Short run maximizes producer surplus (because ixed costs are ignored) Long run maximizes proits (where ixed costs are included) Firms will continue to enter if economic proits are positive; stop or quit if economic proits are negative: constant cost industry. Long run supply = horizontal line at minimum average cost of production: increasing cost industry. Note: supply curves are marginal cost curves in essence, so if increasing production increases mc curves, supply curves are going to increase as well: decreasing cost industry.