MGT120H5 Lecture 9: Lecture 9 (Chapter 8+9) .pdf

12

MGT120H5 Full Course Notes

Verified Note

12 documents

Document Summary

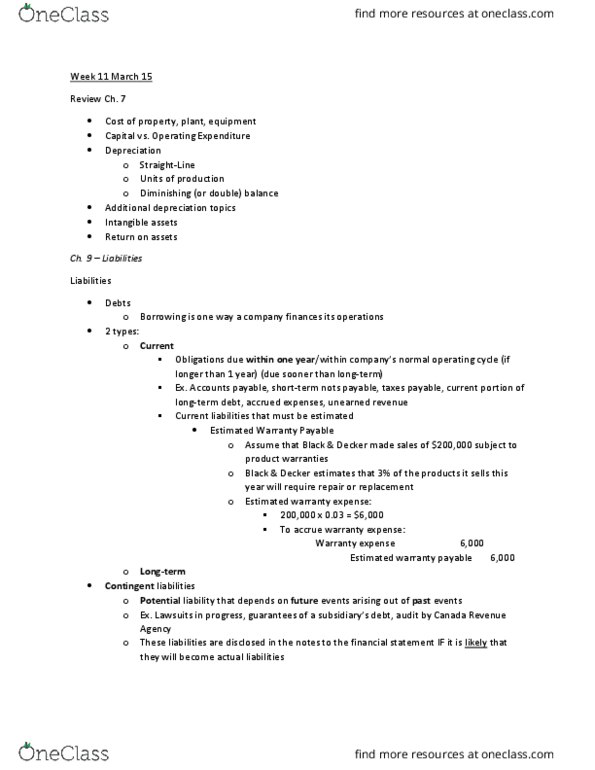

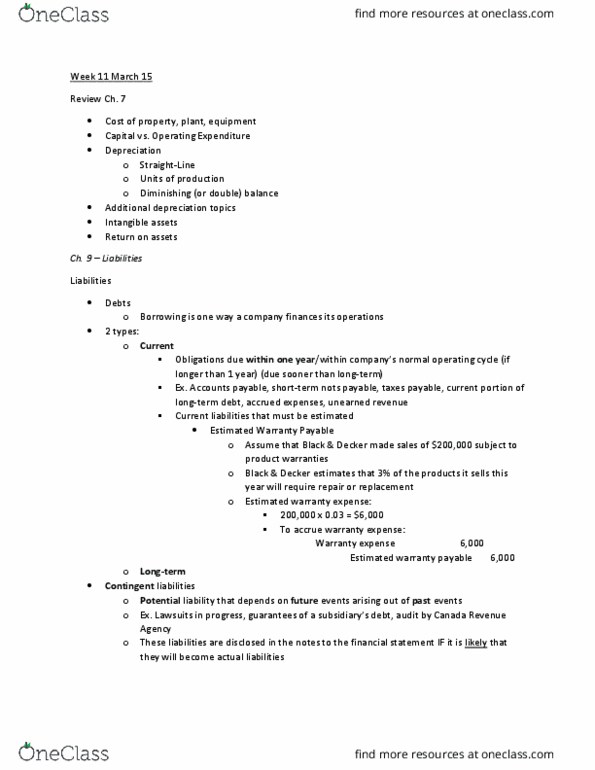

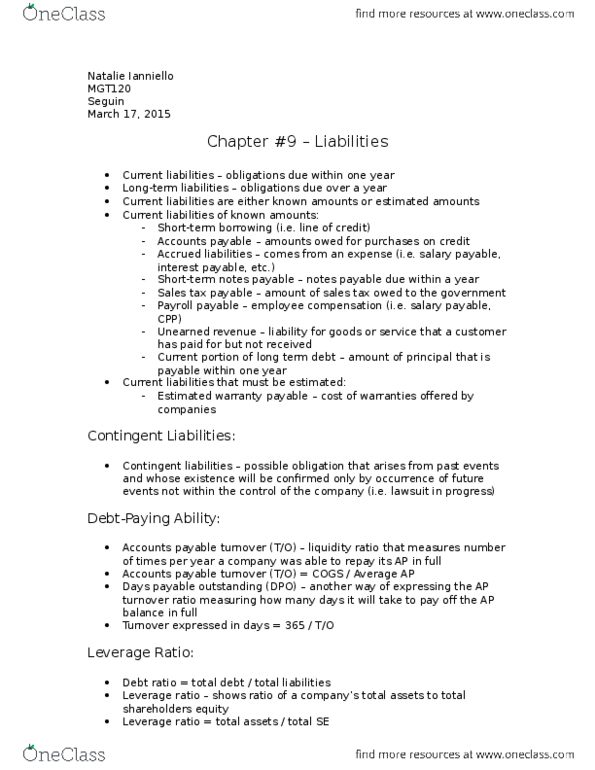

Depreciation straight-line (assuming it wears out overtime), units of operating cycle if it is longer. portion of long- term debt, accrued expenses, unearned revenue, etc. Production(delivery fan, over use) and diminishing balance (more so in the earlier years - ignore residual value) ! Additional depreciation topics intangible assets (lacks physical form, useful to the company) ! Current: one year, long term: mortgage like: 25 years ! Borrowing is one way a company nances its operations ! Liabilities are classi ed as current or long-term ! Current liabilities are obligations due within one year or within the company"s normal. Examples: accounts payable, short-term notes payable, taxes payable, current. Bs: portion of long term debt, and what is owning ! Unearned revenue: cash , and service in the future ! Assume that black & decker made sales of ,000 subject to product warranties. Black & decker estimates that 3% of the products it sells this year will require repair or replacement.