MGT338H5 Lecture Notes - Interest Rate Risk, Nominal Interest Rate, Credit Risk

Document Summary

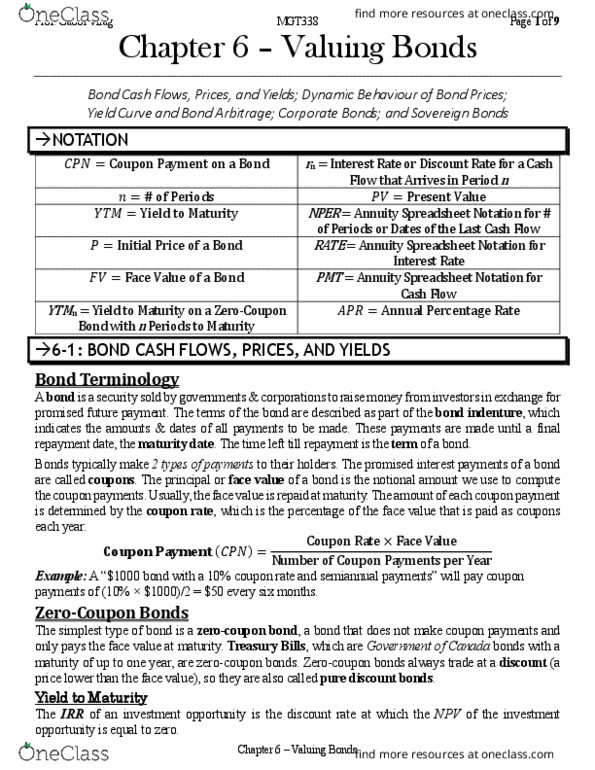

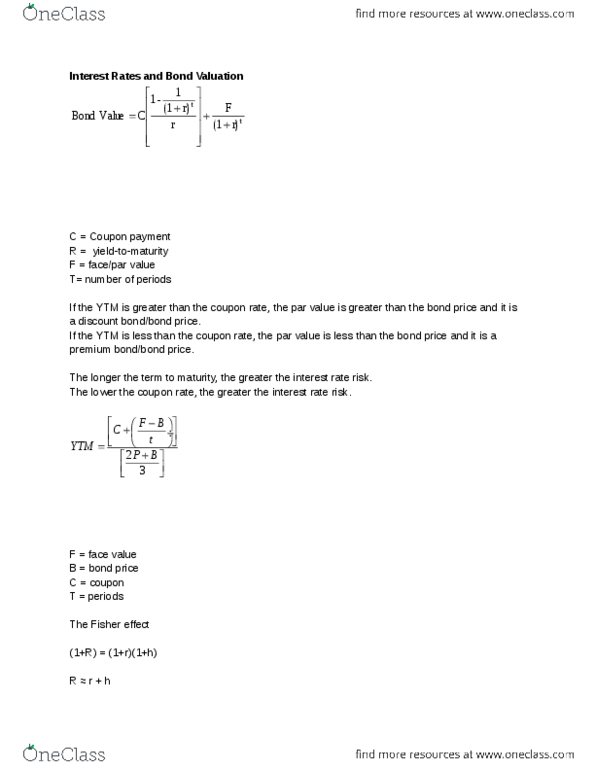

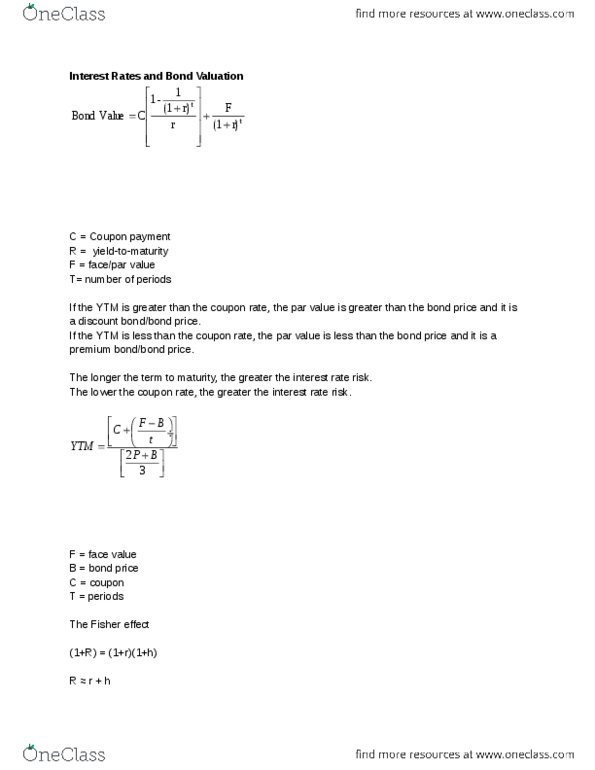

The risk-free rate is an abstract concept, and usually the yield on short-term government treasury bills is used as a proxy for practical purposes. The nominal risk-free rate is comprised of two components. > the real rate, which is compensation for deferring consumption. > the expected inflation rate, which is compensation for the expected loss of purchasing power over the term of the short-term t-bill (the fisher effect: bond price sensitivity: interest rate risk factors. Lower coupon bond --> bond is more sensitive to changes in interest rates. Lower ytm level --> more sensitive --> greater price change: risks for bondholders. Interest rate risk (change in price due to change in interest rates) Inflation risk (fisher effect, i. e. nominal interest rate = real rate + inflation) Default risk (measured as yield spread, or default risk premium) Exchange rate risk: three theories of the term structure.