MGT120H5 Lecture Notes - Lecture 3: Accounts Payable, Railways Act 1921, General Ledger

12

MGT120H5 Full Course Notes

Verified Note

12 documents

Document Summary

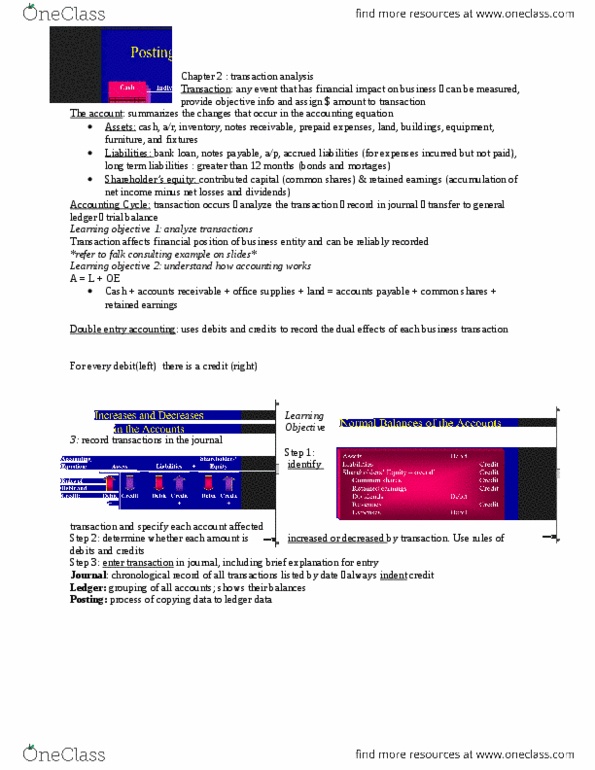

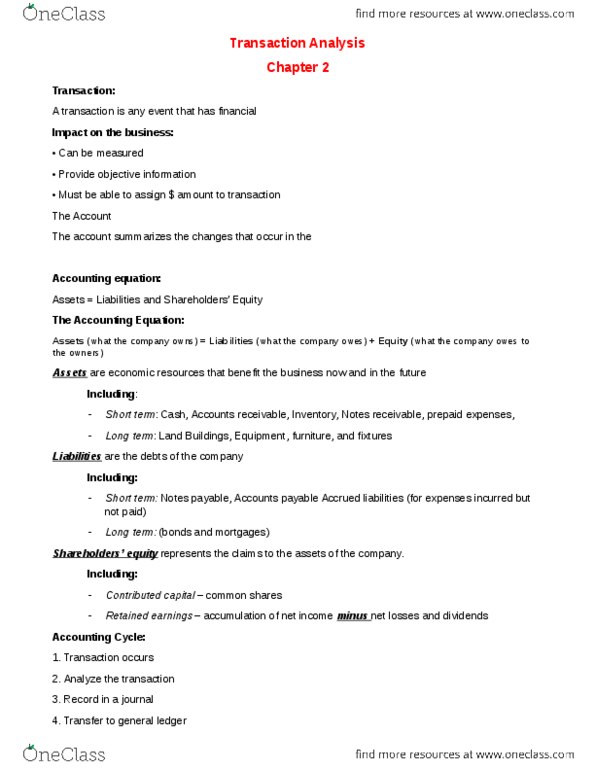

Analyzing business transactions (quantified with dollar value) T-accounts (tool, rough work to balance accounts) Debits and credits: and journal entries. Using trial balance: with software system, makes sure credits and debits balance. Conceptual framework: useful information for decision makers. Accounting assumptions: separate entity, going-concern, historical cost, stable monetary unit. Expenses: statement of retained earnings, balance sheet. Accounting equation: net i(cid:374)(cid:272)o(cid:373)e i(cid:374)(cid:272)(cid:396)eases assets a(cid:374)d i(cid:374)(cid:272)(cid:396)eases sha(cid:396)eholde(cid:396)"s e(cid:395)uity. Main income measures to watch: gross margin/profit, operating income, net income. How can we tell if company can pay debt: short-term: look at current ratio (assets/liabilities, long-term: look at total assets over total debt. Summarizes changes that occur in accounting equation (a=l+e: assets provide future benefits, liabilities are debts, e(cid:395)uity is o(cid:449)(cid:374)e(cid:396)"s (cid:272)lai(cid:373) to assets (company owes owners) Double-entry accounting: double-entry bookkeeping uses debits and credits to record the dual effects of each business transaction. Bought supplies, 750 to be paid in 30 days (accounts payable, because paying in 30 days)