MGEA06H3 Lecture Notes - Lecture 3: Shortage, Autarky

30 Nov 2010

School

Department

Course

Professor

2

MGEA06H3 Full Course Notes

Verified Note

2 documents

Document Summary

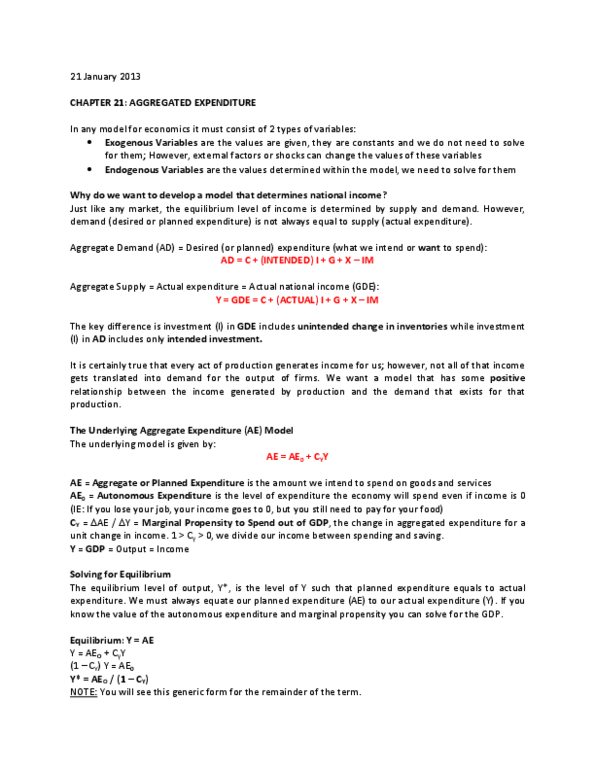

N build a simple model that determines equilibrium national income. N consider how does a change in aggregate expenditure affect national income (we will also discuss the multiplier). Simple model consists of consumption and investment only (will take into account of government and foreign sector next week). It is certainly true that every act of production generates income for canadians; however, not all of that income gets translated into demand for the output of firms. N we want a model that has some positive relationship between. The demand that exists for that production and. Y where cy basically says that every time income increases by that amount will be divided between spending and saving. cy is the amount that will be spent. So, if cy is 0. 85, then 85 cents will be spent for every increase in income. In canada, the cy rate is about 0. 7 right now.