MGAB01H3 Lecture : Natural Resources

16

MGAB01H3 Full Course Notes

Verified Note

16 documents

Document Summary

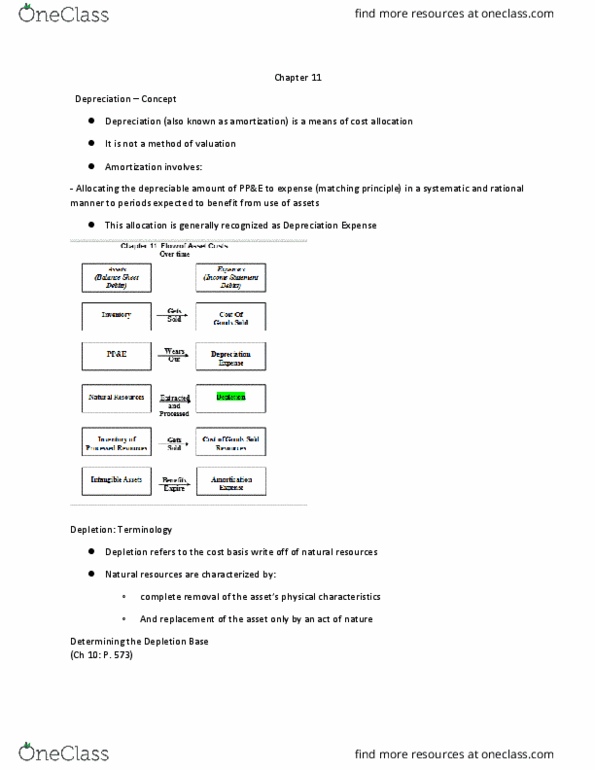

Natural resources consist of timber, oil, gas, and minerals. These assets have two distinguishing characteristics: they are physically extracted and they are replaceable only by an act of nature. This is why they are also called wasting assets. Cost of these assets is the price paid for the property. The amortization of these assets are the same as all other assets, but the amortizable cost of natural resource is affected by residual value and future removal or site restoration costs. Future removal and site restoration costs the matching principle suggests that restoration and removal costs should be estimated in advance and allocated over the useful life of the natural resource. Units-of-activity method the total cost of the natural resource less residual value plus restoration cost is divided by the number of units estimated to be in the resource. Some companies do not use an accumulated amortization account, thus the amount is credited directly to the natural resource account.