MGAB01H3 Lecture Notes - Lecture 10: Accounts Receivable

Document Summary

Get access

Related Documents

Related Questions

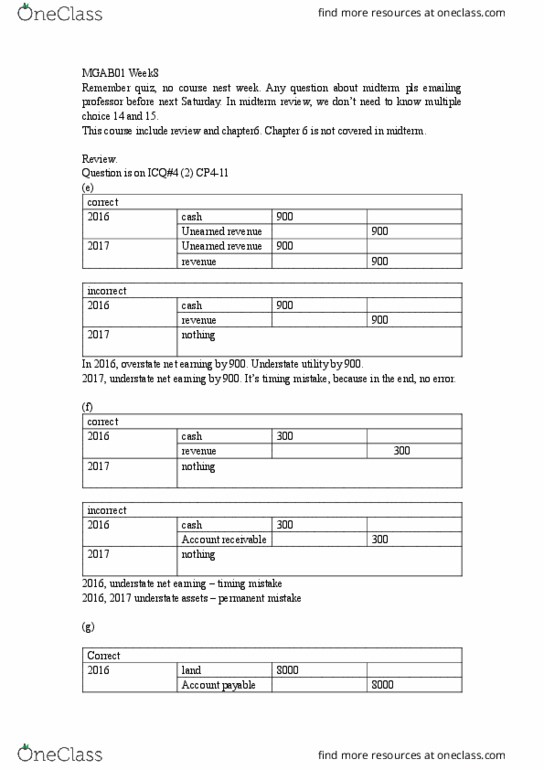

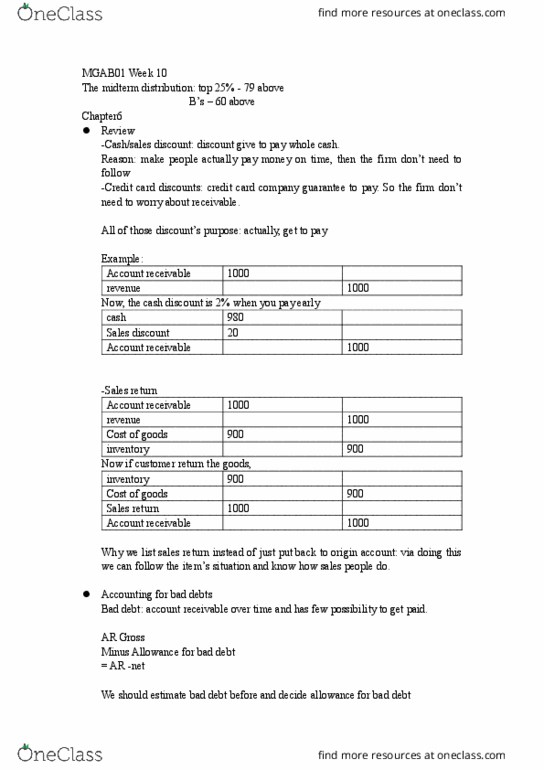

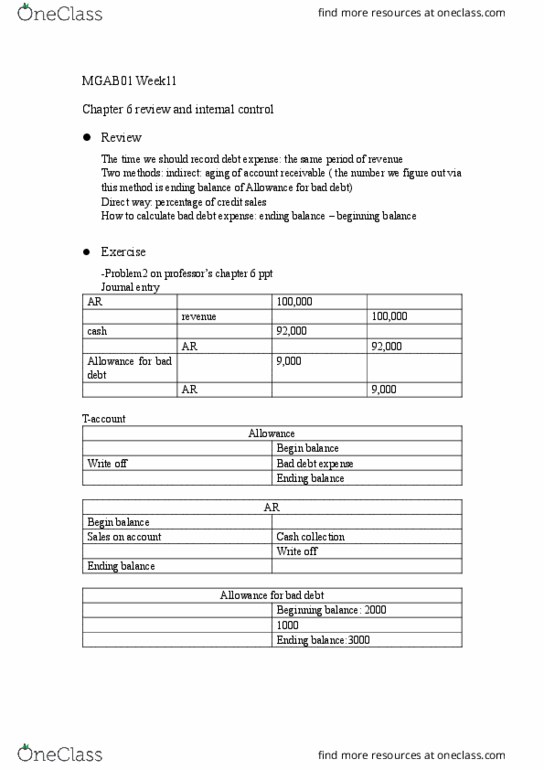

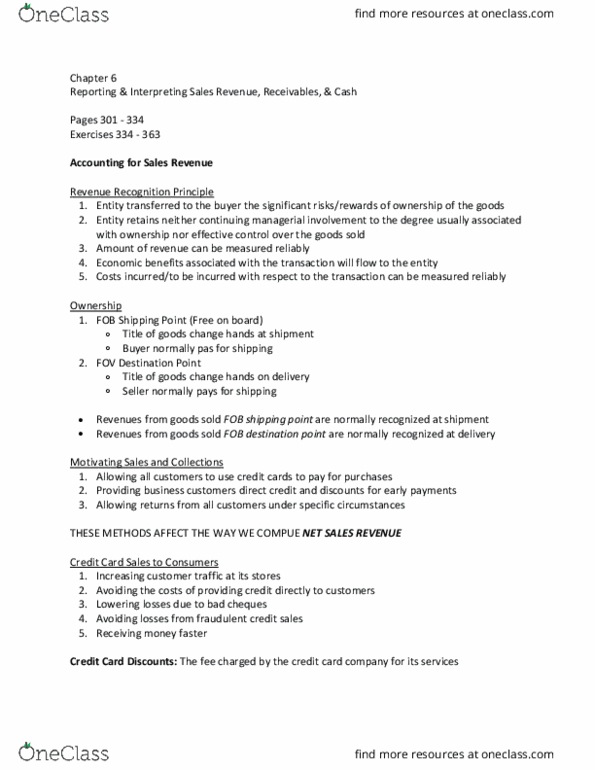

1. Total each column of the special journals. Show that thetotal debits equal the total credits in each special journal.

2. Balance or reconcile the amounts receivable subsidiary ledgerand accounts receivable in the general ledger. Do the same for theaccounts payabel subsidiary ledger and accounts payable in thegeneral ledger.

SalesJournal PAGE 7 | ||||||

DATE | INVOICE NO. | ACCOUNTS DEBITED | POST. REF. | ACCOUNTS RECEIVABLE | COST OF GOODS SOLD | |

July | 2 | 913 | Ishikawa Corp | 24600 | 10800 | |

July | 9 | 914 | Bell Ltd | 33300 | 13860 | |

July | 15 | 915 | M.O.Brown | 3990 | 1440 | |

July | 18 | 916 | Ishikawa Corp | 2142 | 762 | |

July | 29 | 917 | Bell Ltd | 2976 | 1320 | |

Cash ReceiptsJournal PAGE 5 | |||||||||

DEBITS | CREDITS | COST OF GOODS SOLD DR. INVENTORY CR. | |||||||

OTHER ACCOUNTS | |||||||||

DATE | CASH | SALES DISCOUNTS | ACCOUNTS RECEIVABLE | SALES REVENUE | ACCOUNT TITLE | POST. REF. | AMOUNT | ||

July | 5 | 6462 | 6462 | Cash sales | 2880 | ||||

July | 8 | 6650 | Interest revenue | 6650 | |||||

July | 9 | 32967 | 333 | 33300 | Bell Ltd | ||||

July | 12 | 24354 | 246 | 24600 | Ishikawa Corp | ||||

July | 31 | 2142 | 2142 | Ishikawa Corp | |||||

Req.

PurchasesJournal PAGE 10 | ||||||||||||

CREDITS | DEBITS | |||||||||||

OTHER ACCOUNTS | ||||||||||||

DATE | ACCOUNT CREDITED | INVOICE DATE | TERMS | POST REF. | ACCOUNTS PAYABLE | INVENTORY | SUPPLIES | ACCOUNT TITLE | POST. REF. | AMOUNT | ||

July | 3 | Nakkach | 14802 | |||||||||

July | 20 | Burgess | 12282 | |||||||||

July | 28 | Manley | 8050 | |||||||||

Cash PaymentsJournal PAGE 8 | |||||||||

DEBITS | CREDITS | ||||||||

DATE | CHQ. NO. | ACCOUNTS DEBITED | POST REF. | OTHER ACCOUNTS | ACCOUNTS PAYABLE | INVENTORY | CASH | ||

July | 5 | Furniture | 13110 | ||||||

July | 10 | Purchases | 6858 | ||||||

July | 13 | Nakkach | 14802 | 14358 | |||||

July | 22 | Prepaid insurance | 6000 | ||||||

July | 25 | Utilities | 6718 | ||||||

July | 30 | Manley Inc | 8050 | 7889 | |||||

July | 31 | Salaries | 14082 | ||||||

Accounts Receivable SubsidiaryLedger

ACCOUNT BELLLTD. | ||||||

DATE | ITEM | JRNL. REF. | DEBIT | CREDIT | BALANCE | |

July | 9 | Bell Ltd | 6 | 33300 | 33300 | |

July | 19 | Bell Ltd | 13 | 32967 | 32967 | |

July | 19 | Bell Ltd Discount | 13 | 333 | 333 | |

July | 29 | Bell Ltd | 21 | 2976 | 2976 | |

ACCOUNT M.O.BROWN | ||||||

DATE | ITEM | JRNL. REF. | DEBIT | CREDIT | BALANCE | |

July | 15 | M.O.Brown (credit sale) | 11 | 3990 | 3990 | |

July | 15 | M.O.Brown (Sold to) | 11 | 1440 | 1440 | |

ACCOUNT ISHIKAWAINC. | ||||||

DATE | ITEM | JRNL. REF. | DEBIT | CREDIT | BALANCE | |

July | 2 | Ishikawa Inc (credit sale) | 1 | 24600 | 24600 | |

July | 10 | Ishikawa Inc (discount) | 8 | 246 | 246 | |

July | 10 | Ishikawa Inc | 8 | 24354 | -24354 | |

July | 18 | Ishikawa Inc (credit sale) | 13 | 2142 | -2142 | |

Accounts Payable SubsidiaryLedger

ACCOUNT BURGESSDISTRIBUTINGLTD. | ||||||

DATE | ITEM | JRNL. REF. | DEBIT | CREDIT | BALANCE | |

July | 15 | Burgess Distribution Ltd (Purchases) | 15 | $12,282 | -$12,282 | |

ACCOUNT NAKKACHCORP. | ||||||

DATE | ITEM | JRNL. REF. | DEBIT | CREDIT | BALANCE | |

July | 3 | Nakkach Corp (purchase of inventory) | 2 | $14,802 | -$14,802 | |

July | 13 | Nakkach Corp (Discount) | 9 | $444.06 | $444.06 | |

July | 22 | Nakkach Corp (Furniture Purchase) | 16 | $3870 | -$3870 | |

ACCOUNT MANLEY,INC. | ||||||

DATE | ITEM | JRNL. REF. | DEBIT | CREDIT | BALANCE | |

July | 13 | Manley Inc (Purchase of supplies) | 10 | $8646 | -$8646 | |

July | 28 | Manley Inc | 19 | $805 | -$805 | |

July | 29 | Manley Inc (Return) | 20 | $4050 | $4050 | |