RSM222H1 Lecture : Chapter eight.docx

7 Apr 2013

School

Department

Course

Professor

Document Summary

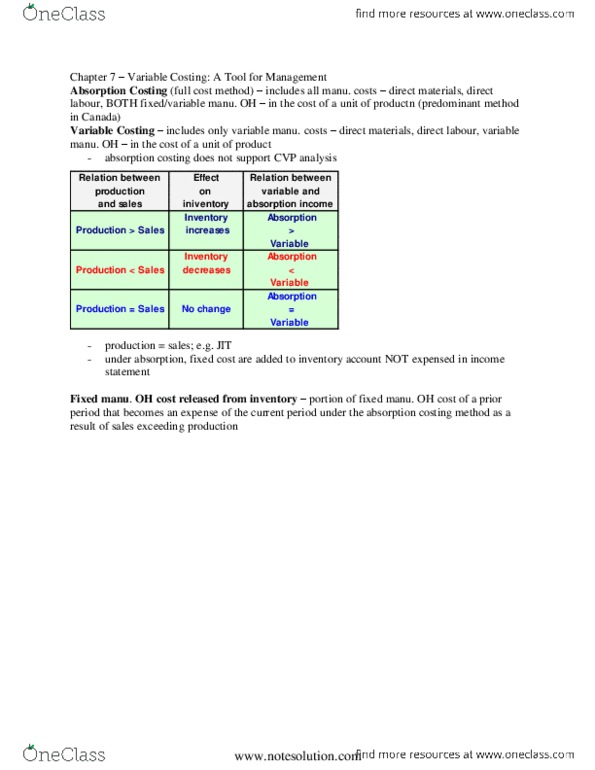

Chapter eight: variable costing: a tool for management. Absorption costing assigns both variable and fixed costs to products the bully them in a way that makes it difficult for managers to distinguish between them. Variable costing focuses on cost behavior, clearly separating fixed from variable costs one of the strength of variable costing is that it harmonize with both the contribution approach and the cost volume profit concept. Variable costing: a costing method that includes only variable manufacturing cost direct materials, direct labor, and variable manufacturing overhead in the cost of a unit of product. Fixed manufacturing overhead is not treated as a product cost under this profit better, fixed manufacturing overhead is treated as period cost like selling and administrative expenses and it is expensed in its entirety as revenue each. Cost of unit of product in inventory or the cost of goods sold under the variable cost and market does not take a fixed overhead costs.