RSM225H1 Lecture Notes - Certified General Accountant, Financial Accounting, Accounting

Document Summary

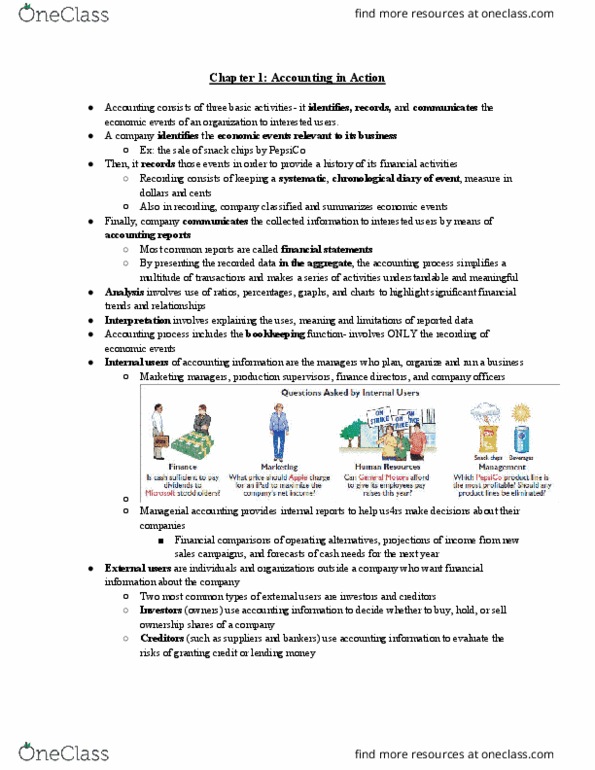

1. 1 accounting is an information system that identifies, records, and communicates economic events of an organization to interested users. 1. 1. 1 identifying involves selecting those events that are considered evidence of economic activity, relevant to a particular business organization. 1. 1. 2 once identified and measured in dollars and cents, economic events are recorded to provide a permanent history of the financial activities of the organization. Recording consists of keeping a chronological diary of the measured events in an orderly and systematic manner. 1. 1. 3 the information is communicated through the preparation and distribution of accounting reports, the most common of which are called financial statements: users and uses of accounting. 2. 1 internal users are those who manage the business and use accounting data in planning, controlling, and evaluating business operations. Examples include marketing managers, production supervisors, finance directors, and company officers. 2. 2 external users are those users outside of the business who need information about the financial position and performance of the company.