Economics 2162A/B Lecture Notes - Lecture 9: Systematic Risk, Uncorrelated Random Variables, Rade People

2 May 2016

School

Department

Course

Professor

Document Summary

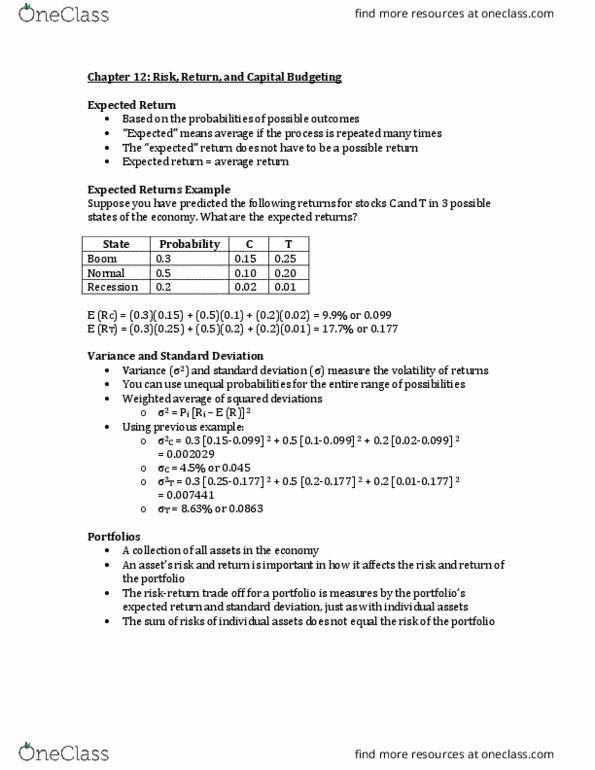

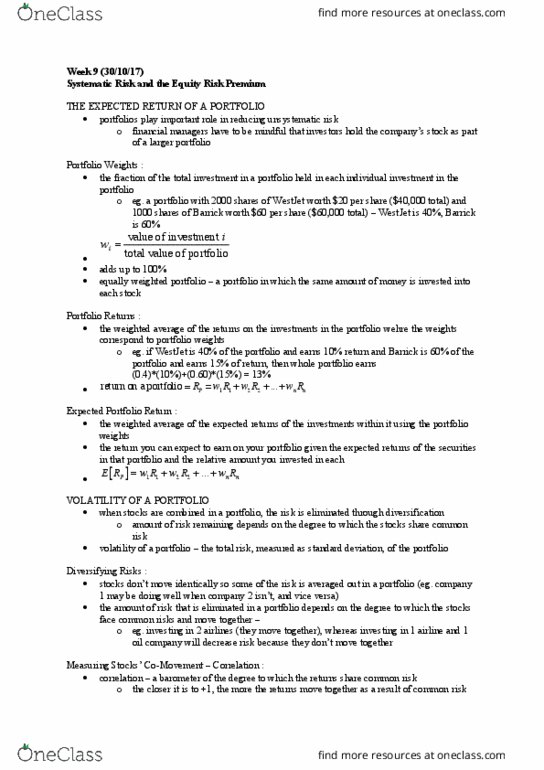

Perfect correlation with two perfectly correlated securities all portfolios will lie on a straight line (r=1) ex. when corr (p) = +1. With uncorrelated assets it is possible to create a two asset portfolio with lower risk than either asset ( r=. 00) With positively correlated assets a two asset portfolio lies between the first two curves r=. 50. With negatively correlated assets it is possible to create a portfolio with much lower risk r=-. 5 ww2 + p=. 5. With pnc assets, it is possible to create a two asset port with no risk. Security returns are much less correlated across countries than within a country. This is so because economic, political, institutional and even psychological factors affecting security returns tend to vary across countries, resulting in low correlations among international securities. Business cycles are often high asynchronous across countries. international diversification can sharply reduce risk.