Management and Organizational Studies 1023A/B Lecture Notes - Cash Flow, Photocopier, The Need

1 Mar 2013

School

Department

Professor

9

MOS 1023A/B Full Course Notes

Verified Note

9 documents

Document Summary

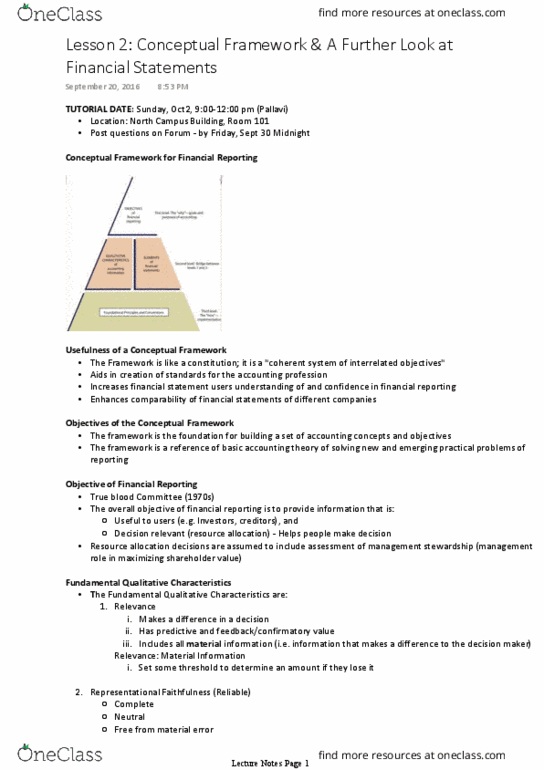

Jan 23 financial statements framework, presentation and. To develop a coherent set of standards and principles. To solve new and emerging practical problems. Framework provides investors and creditors information to make comparisons with other companies. Committee formed to determine what the objectives are. The ability to assess the amount, time and certainty of future cash flow. Predictive value: ability to decipher future cash values. Substance over form: look at substance of transaction and determine if it"s an asset, liability etc. eg. apartment rent payment. Look at the true substance of the economic situation not what it says. Comparability: the more estimates, the less reliable it tends to be. If you change something, it must be because it provides better information. Understandability: whether an investor who is reasonably informed can comprehend the information. Tradeoffs: giving up one characteristic over the other eg. being timely, giving up some completeness. Cost vs. benefits: eg. the cost of giving information, rounding money up.