Management and Organizational Studies 3370A/B Lecture 4: lecture 4

7 Oct 2016

School

Department

Professor

Document Summary

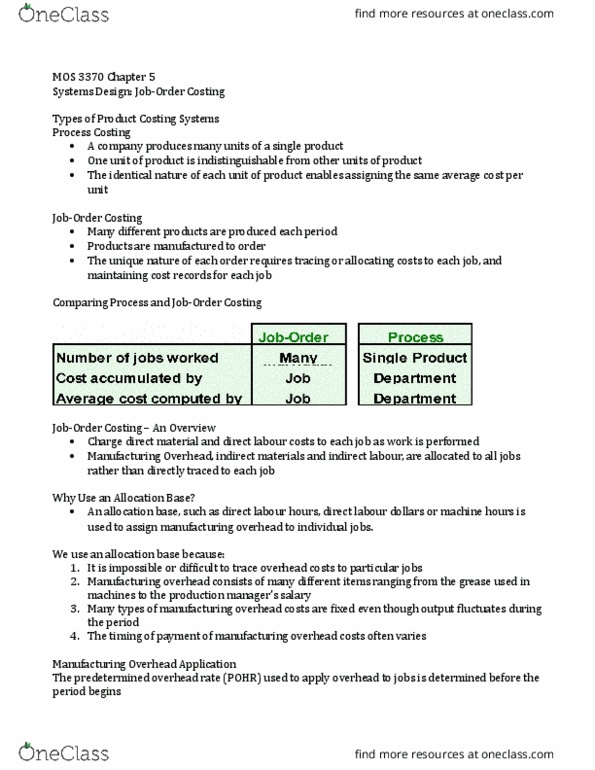

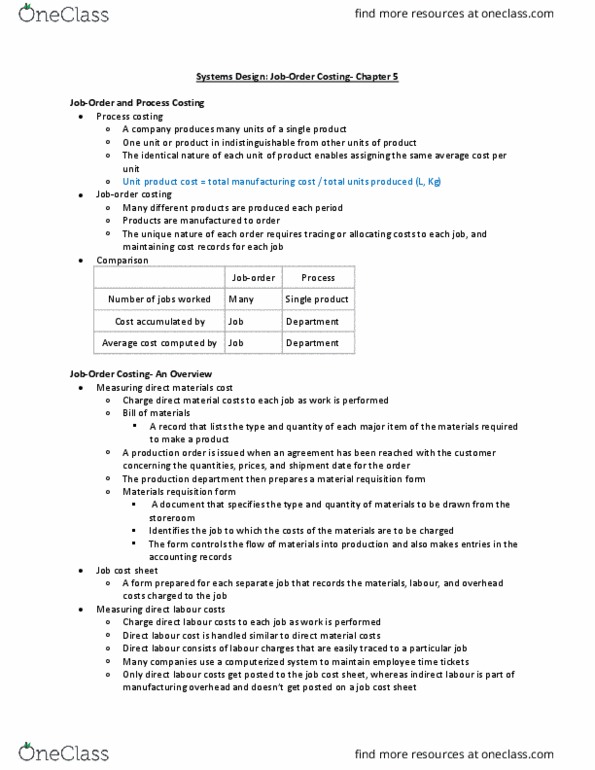

Lecture 4 types of product costing systems. A company produces many units of a single product. One unit of product is indistinguishable from other units of product. The identical nature of each unit of product enables assigning the same average cost per unit: i. e. cement mixing, petroleum, mixing and bottled beverages. Many different products are produced each period. The unique nature of each order requires tracing or allocating costs to each job, and maintaining. Department: i. e. bombardier, hallmark multiple products charge direct material and direct labour costs to each job as work is performed. Manufacturing overhead indirect materials and labour, are allocated to all jobs rather than directly traced to each job. The job cost sheet theory based question possible. Shows difference between direct material, labour, moh and are able to calculate a per unit cost/ per job. An allocation base is used to assign moh to individual jobs (e. g. dl hours, dollars, machine hours)