BU111 Lecture Notes - Stock Valuation, Effective Interest Rate

19

BU111 Full Course Notes

Verified Note

19 documents

Document Summary

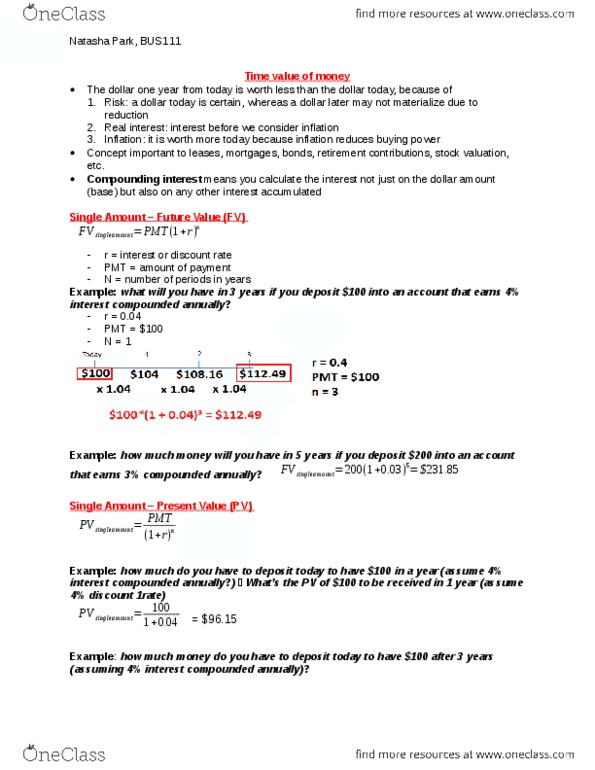

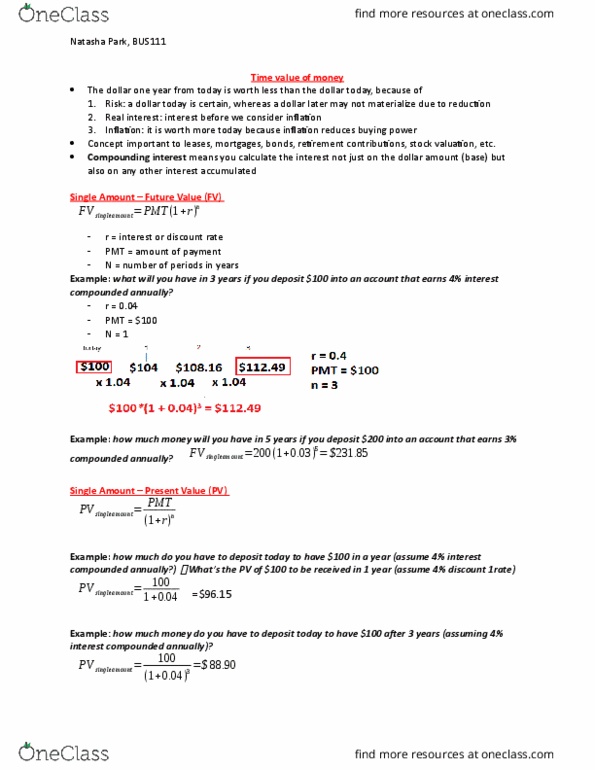

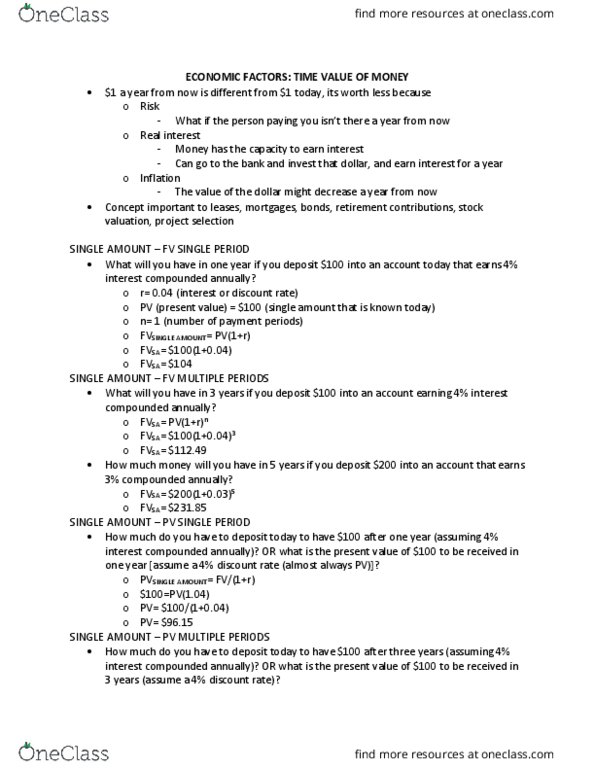

Inflation: it is worth more today because inflation reduces buying power. Concept important to leases, mortgages, bonds, retirement contributions, stock valuation, etc. Compounding interest means you calculate the interest not just on the dollar amount (base) but also on any other interest accumulated. Single amount future value (fv) r = interest or discount rate. N = number of periods in years. Example: what will you have in 3 years if you deposit into an account that earns 4% interest compounded annually? r = 0. 04. Example: how much do you have to deposit today to have in a year (assume 4% interest compounded annually?) What"s the pv of to be received in 1 year (assume 4% discount 1rate) Annuity: multiple payments of the same value, equally apart from each other in time. ] used when you deposit starting today, time zero. ] used when you deposit starting at the end of this year.