BU127 Lecture 3: BU127 Lecture 3 on The Statement of Financial Position and Transaction Specifics

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

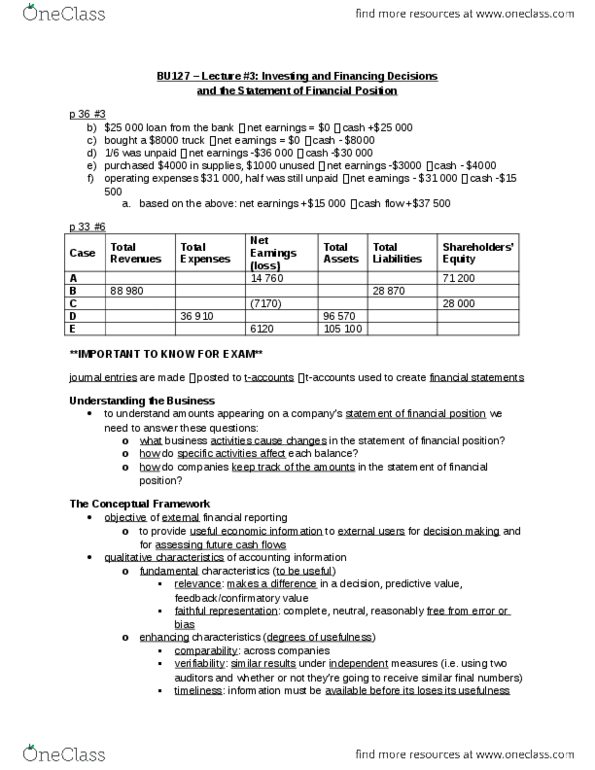

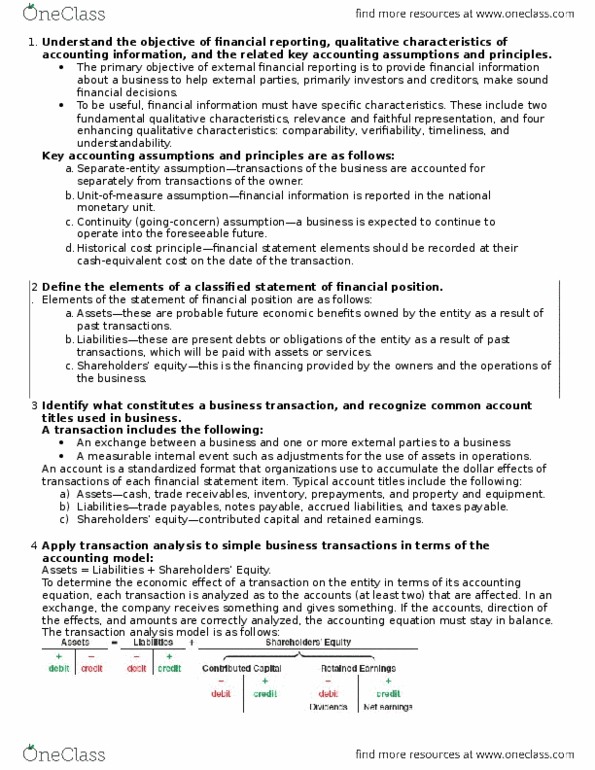

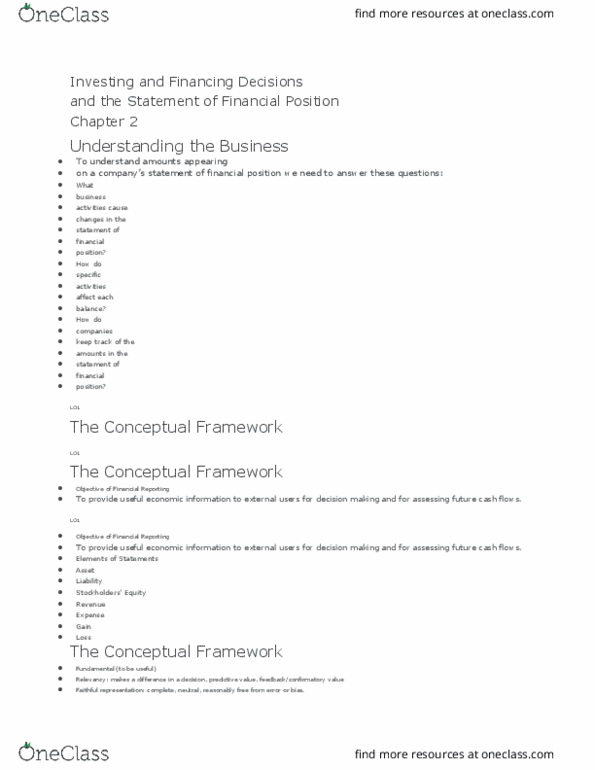

Day 3 - monay sept 16 (chpt 2) Asset - a debit is (+), a credit is (-) Liabilities and se - a credit is (+), a debit is (-) ex. when a business pays back a loan, their debt goes down. If net income is positive, shareholder equity increases, therefore income is credit. **consider the income statement a part of the financial position - income statement relates directly to retained earnings. Relevancy (makes a diff. in decision, predictions) - fundamental. Faithful representation (complete, neutral, free of bias or error) - fundamental. Timeliness(reported before it loses its usefulness) - enhances. Understandability (significance should be clear) - enhances. Business activities are separate from those of owners. Accounting info should be measured by national monetary unit. Business in continuing operations into foreseeable future. Cost principle - assets are recorded at the historical cost.