BU127 Lecture Notes - Lecture 4: Accrual, Deferral, Deferred Income

6

BU127 Full Course Notes

Verified Note

6 documents

Document Summary

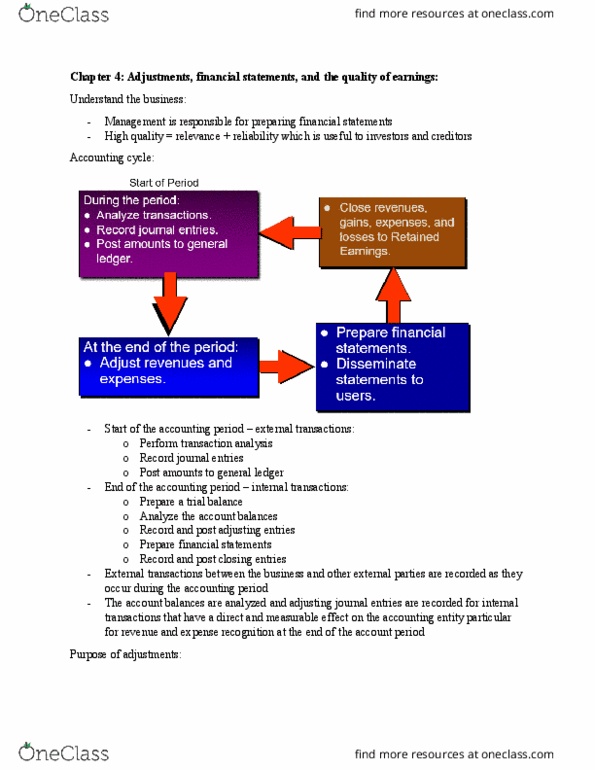

Chapter 4 adjustments, financial statements, and the quality of earnings. First run an unadjusted trial balance: error corrections, revenue adjustments. Ensure: all sales for current period are included and none for the next period. Accrued: non operating revenues, interest revenue investments, rental revenue. Received in the period but not yet recorded (no suppliers" invoices, yet recorded) Phase 1: during the accounting period (primarily external transactions) Phase 2: end of the accounting period (internal transactions) During the accounting period, external transactions between the business and other external parties are recorded as they occur. At the end of the accounting period, the account balances are analyzed and adjusting journal entries are recorded for internal transactions that have a direct and measurable effect on the accounting entity, particularly for revenue and expense recognition. Because transactions occur over time, adjustments are required at the end of each fiscal period to get the revenues and expenses into the right period.