BU353 Lecture Notes - Lecture 6: Cash Flow, Net Present Value

Chapter 6: Loss Control

Numerous activities reduce expected losses by reducing the frequency of losses (loss prevention). An

extreme example of loss prevention is to avoid completely the activity that potentially gives rise to the

loss (loss avoidance).

Activities that reduce expected losses by decreasing the size of the loss conditional on a loss occurring

are called loss reduction; they can occur before or after a loss. Pre-loss activities occur before a loss;

they decrease the magnitude of a loss if one occurs. Post-loss activities occur subsequent to an event

that causes a loss. An important type of pre-loss reduction activity is disaster response or catastrophe

planning.

Segregation of Exposure Units – when a firm diversifies risk by segregating loss exposures into smaller

exposure units; reduces the variance of direct losses and the maximum probable direct loss

Optimal loss control decisions required that loss control expenditures be made up to the point that the

marginal benefits no longer exceed the marginal costs. Directing resources towards safety measures

that are the most cost-effective saves lives and reduces the total cost of risk.

Loss control decisions often need to assess the value of human life.

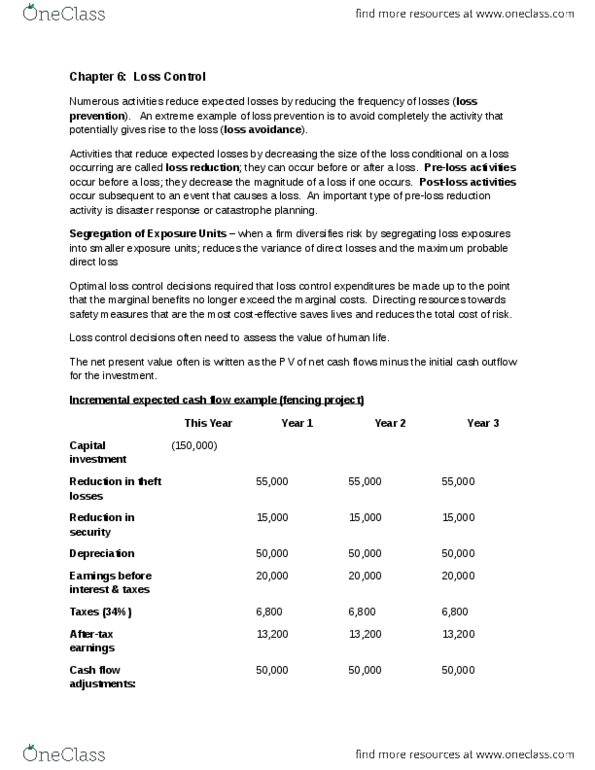

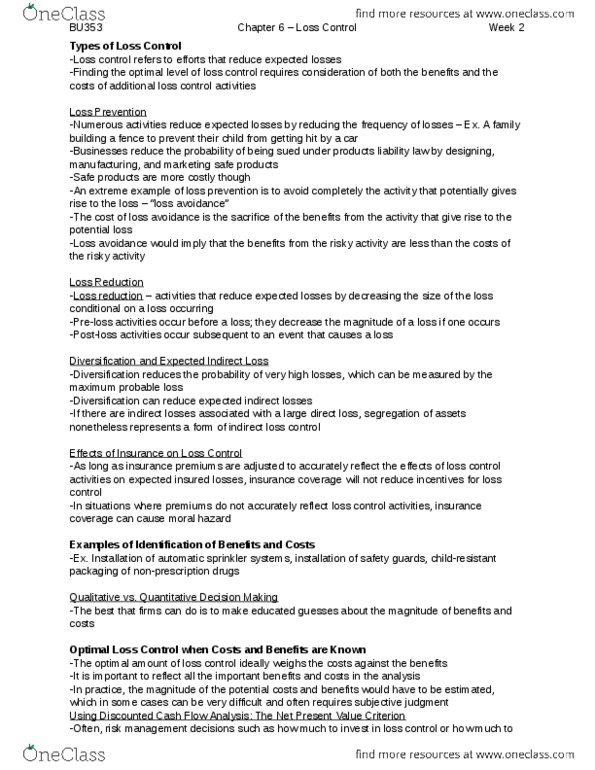

The net present value often is written as the PV of net cash flows minus the initial cash outflow for the

investment.

Incremental expected cash flow example (fencing project)

This Year

Year 1

Year 2

Year 3

Capital investment

(150,000)

Reduction in theft

losses

55,000

55,000

55,000

Reduction in

security

15,000

15,000

15,000

Depreciation

50,000

50,000

50,000

Earnings before

interest & taxes

20,000

20,000

20,000

Taxes (34%)

6,800

6,800

6,800

After-tax earnings

13,200

13,200

13,200

Cash flow

adjustments:

Add depreciation

50,000

50,000

50,000

Expected net cash

flow

63,200

63,200

63,200

PV of cash flow

(10% discount rate)

(150,000)

57,454

52,231

47,483

NPV =

$7,169

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Numerous activities reduce expected losses by reducing the frequency of losses (loss prevention). An extreme example of loss prevention is to avoid completely the activity that potentially gives rise to the loss (loss avoidance). Activities that reduce expected losses by decreasing the size of the loss conditional on a loss occurring are called loss reduction; they can occur before or after a loss. Pre-loss activities occur before a loss; they decrease the magnitude of a loss if one occurs. Post-loss activities occur subsequent to an event that causes a loss. An important type of pre-loss reduction activity is disaster response or catastrophe planning. Segregation of exposure units when a firm diversifies risk by segregating loss exposures into smaller exposure units; reduces the variance of direct losses and the maximum probable direct loss. Optimal loss control decisions required that loss control expenditures be made up to the point that the marginal benefits no longer exceed the marginal costs.