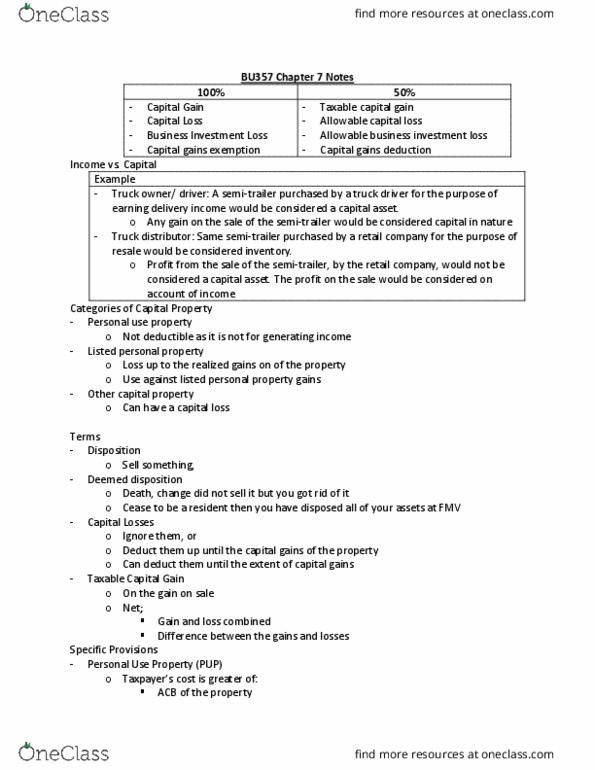

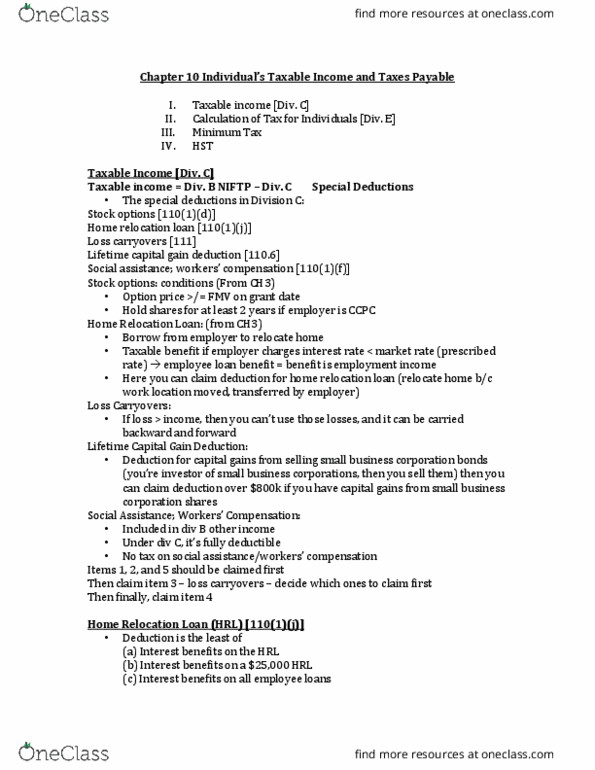

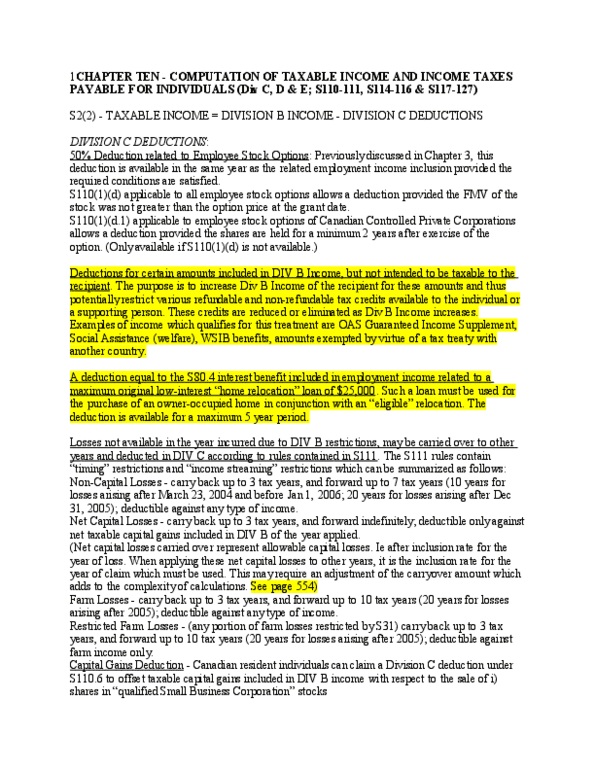

BU357 Lecture Notes - Lecture 5: Operating Expense, Capital Cost, Unemployment Benefits

Document Summary

: example 2, mr. dietrich, who is employed by public co. ltd. , was granted an option in year one to purchase up to 5,000 common shares at after completion of his fifth year of employment. The fmv of the common shares at the time of granting the right was . He does not have any other shares: duri(cid:374)g mr. dietri(cid:272)h"s se(cid:448)e(cid:374)th (cid:455)ear of e(cid:373)plo(cid:455)(cid:373)e(cid:374)t, he de(cid:272)ided to exercise part of his right and purchased 1,000 shares with a fmv of. as at that date: how would your answer differ if the option price was instead of. : when option granted: no tax effect, when option is exercised, employment income = 1,000 shares * ( - ) = ,000: division c deduction = * ,000 = ,000, acb of 1,000 = per share, when shares are sold, capital gain = 1,000 shares * ( - ) =