BU487 Lecture Notes - Lecture 23: Income Statement, Purch Group, Spot Contract

Document Summary

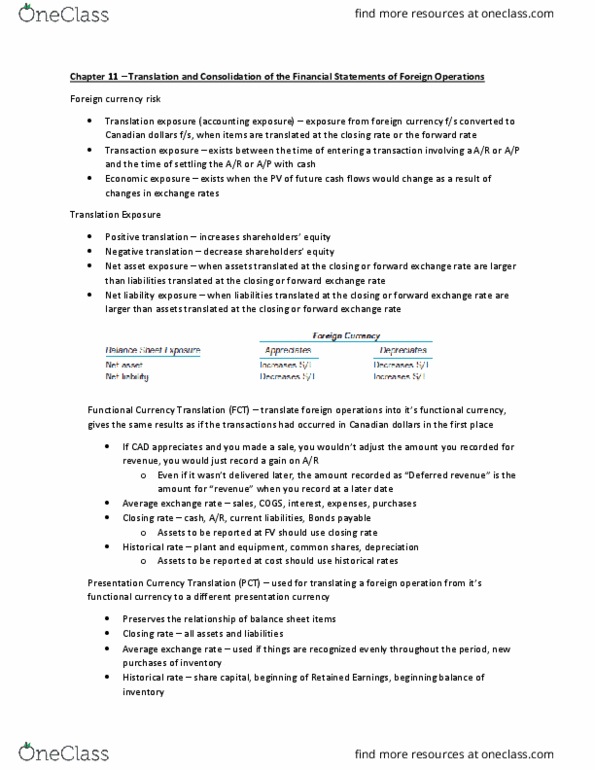

Pv of future cash flows from the sub varies in a long run: translation exposure accounting exposure results from the translation of foreign-currency-denominated financial statements into. Canadian dollar-denominated, giving rise to exchange gains and losses: translation adjustments, translating at the closing rate creates an accounting exposure to rate changes. The abc ltd. has a foreig(cid:374) u(cid:271) i(cid:374) u. Acquisition differential is 3,000 usd at t=0, which is allocated to: equipment, building. Assume: both assets have a10 year useful life. Required: translation gain or loss from amortization of ad using different methods. Fct (use same exchange rate as on acquisition date): 3,300-2,970= 330 therefore, no gain and no loss. Pct (use average, report under oci) ***finish up**** 3,300 348= 2,952 (not the same as y/e numbers so translation gain/loss) 3,294 2,952= 342 (this will be an asset, and the 342 is a translation gain)