ACTG 2011 Lecture Notes - Inventory Control, Perpetual Inventory, Inventory Turnover

23 Feb 2011

School

Department

Course

Professor

Document Summary

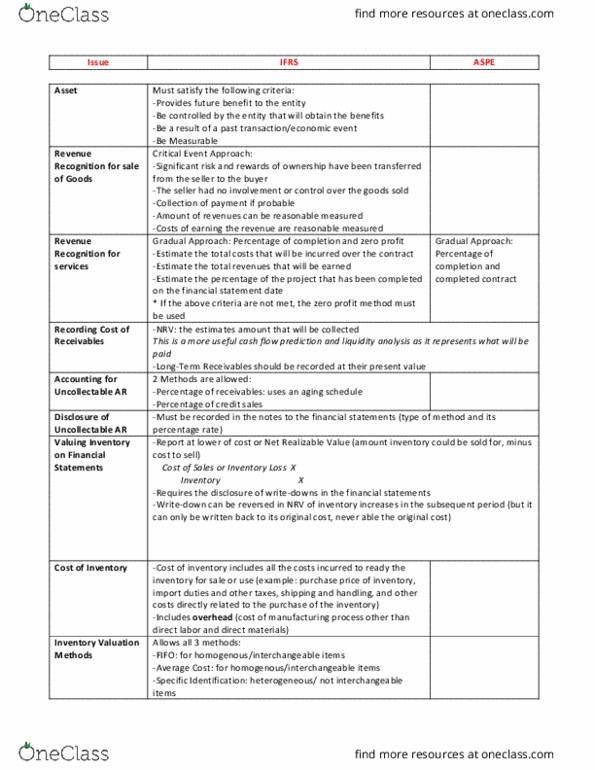

Inventory is assets held for sale or assets used to produce goods that will be sold as part of the business. Work-in-progress of wip inventory: partially completed product to date. Finished goods: inventory that has been completed and ready for sale. Requires inventory to be valued at costs on the balance sheet. Net realizable value (nrv) of inventory is less than costs, the inventory must be written down to its nrv. Costs of inventory includes all costs incurred to ready the inventory for sale or use: purchase price, import duties, and other taxes, shipping and handling, and any other costs directly related to the purchase of the inventory. Ifrs requires that the cost of inventory include the cost of materials, labor costs plus an allocation of overhead incurred in the production process. Overhead is the costs in manufacturing process other than direct labor and direct material.