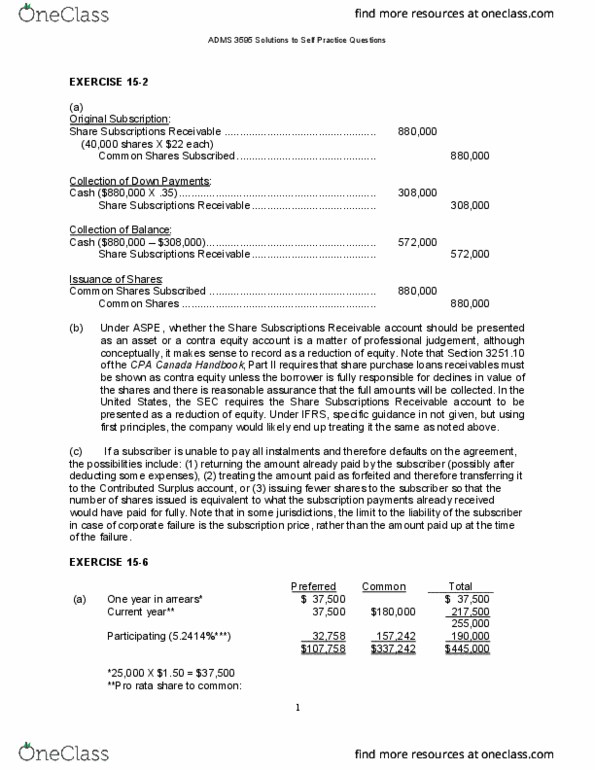

ADMS 3595 Lecture Notes - Share Capital, Issued Shares, Capital Account

Get access

Related Documents

Related Questions

May I get step by step approach on the following question. I need help on (b). But could you please check the accuracy for my answers in (a)? Please know the "Answer" areas are supposed to be blank and supposed to be filled in. Thank you for your time.

Identifying and Analyzing Financial Statement Effects of Stock Transactions

The stockholders' equity of Verrecchia Company at December 31, 2011, follows:

| Common stock, $ 5 par value, 350,000 shares authorized; 150,000 shares issued and outstanding | $ 750,000 |

| Paid-in capital in excess of par value | 600,000 |

| Retained earnings | 346,000 |

During 2012, the following transactions occurred:

Jan. 5 Issued 10,000 shares of common stock for $12 cash per share.

Jan. 18 Purchased 4,000 shares of common stock for the treasury at $14 cash per share.

Mar. 12 Sold one-fourth of the treasury shares acquired January 18 for $17 cash per share.

July 17 Sold 500 shares of the remaining treasury stock for $13 cash per share.

Oct. 1 Issued 5,000 shares of 8%, $25 par value preferred stock for $35 cash per share. This is the first issuance of preferred shares from the 50,000 authorized shares.

(a) Use the financial statement effects template to indicate the effects of each transaction.

Use negative signs with answers, when appropriate.

| Balance Sheet | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Transaction | Cash Asset | + | Noncash Asset | = | Liabilities | + | Contributed Capital | + | Earned Capital | |

| Jan. 5 | 110,000 | Answer | Answer | 110,000 | Answer | |||||

| Jan. 18 | -60,000 | Answer | Answer | -60,000 | Answer | |||||

| Mar. 12 | 17,000 | -17,000 | Answer | Answer | Answer | |||||

| July. 17 | 7,000 | Answer | 7,000 | Answer | Answer | |||||

| Oct. 1 | 190,000 | Answer | Answer | 190,000 | Answer | |||||

| Income Statement | |||||

|---|---|---|---|---|---|

| Revenue | - | Expenses | = | Net Income | |

| Answer | Answer | Answer | |||

| Answer | Answer | Answer | |||

| Answer | Answer | Answer | |||

| Answer | Answer | Answer | |||

| Answer | Answer | Answer | |||

(b) Prepare the December 31, 2012, stockholders' equity section of the balance sheet assuming that the company reports net income of $72,500 for the year.

Use a negative sign with your answer for treasury stock.

| Stockholders' Equity | ||

|---|---|---|

| Paid-in capital | ||

| 8% Preferred stock, $25 par value, 50,000 shares authorized, 5,000 shares issued and outstanding | $Answer | |

| Common stock, $5 par value, 350,000 shares authorized; 160,000 shares issued | Answer | $Answer |

| Additional paid-in capital | ||

| Paid-in capital in excess of par value-preferred stock | Answer | |

| Paid-in capital in excess of par value-common stock | Answer | |

| Paid-in capital from treasury stock | Answer | Answer |

| Total paid-in capital | Answer | |

| Retained earnings | Answer | |

| Answer | ||

| Less: Treasury stock (2,500 shares) at cost (use a negative sign with your answer) | Answer | |

| Total Stockholders' Equity | $ Answer | |