ADMS 4503 Lecture Notes - Lecture 9: Royal Aircraft Factory B.E.2, Arbitrage, Risk Neutral

2 Apr 2013

School

Department

Course

Professor

Document Summary

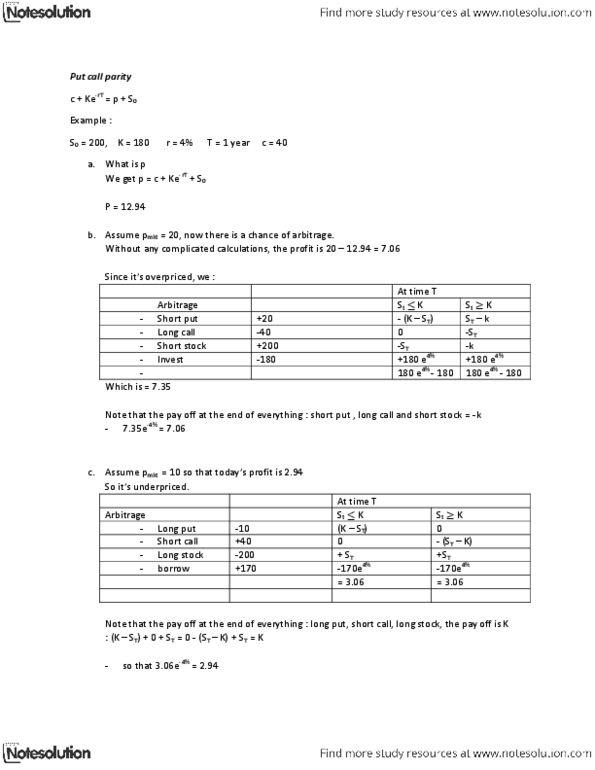

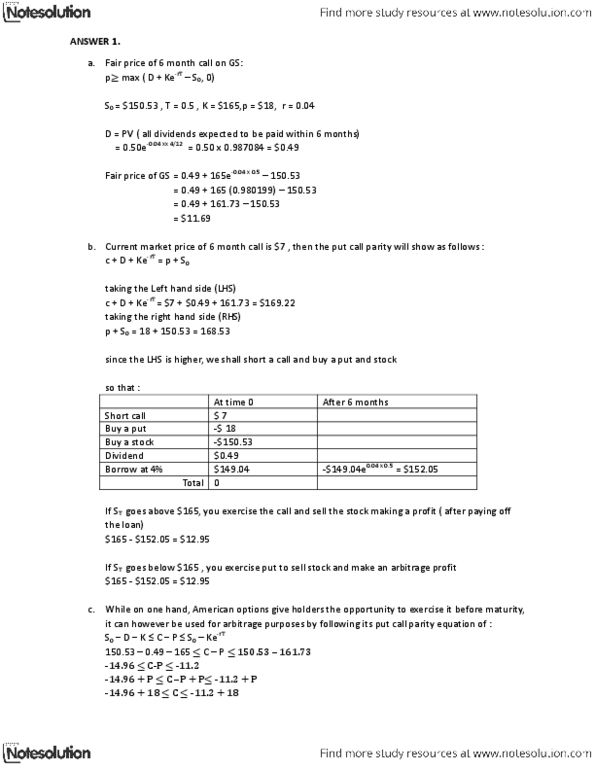

Note: all black lines are initial positions, all red lines are the second step. S = 100, k = 100 div = 4 (time = 0. 5) r = 4% t = 1 cmkt = 40, pmkt = 20. C + ke-rt s0 pv(div) + p. Call put parity is not satisfied , so we can arbitrage. So we short expensive side and go long on the cheaper side: ( long put + short call + long stock = k at maturity ) We can find a rough estimate of how much we can make from the arbitrage = 136. 0789 116. 0792 = Now, if we discount the value 20. 82 , we will get 19. 9997. Max profit : k2 k1 ( c1 + c3 -2c2. Max loss : - (c1 +c3 - 2c2) Be1 = k1 + (c1 +c3 - 2c2) Be2 = k3 (c1 +c3 - 2c2)