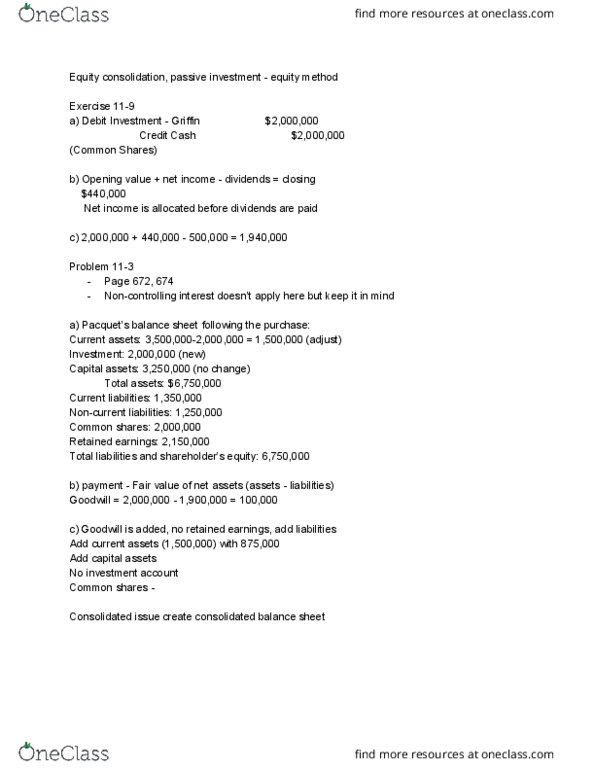

ADMS 4520 Lecture Notes - Lecture 3: Current Liability, Retained Earnings, Homestar Runner

11 May 2018

School

Department

Course

Professor

Chapter 3 – Business Combinations

CHAPTER 3

Business Combinations

SOLUTIONS TO PROBLEMS

P3-1

a. Statement of financial position:

Alternatives:

1 2 3 4

Current assets

$6,650,000

$5,700,000

$8,550,000

$8,550,000

Capital assets

13,450,000

13,450,000

13,450,000

13,450,000

Investments

350,000

350,000

350,000

350,000

Goodwill

500,000

500,000

500,000

500,000

Total Assets

$20,950,000

$20,000,000

$22,850,000

$22,850,000

Current liabilities

$4,150,000

$4,000,000

$4,150,000

$4,150,000

Long-term liabilities

6,800,000

6,000,000

6,800,000

6,800,000

Deferred income taxes

2,000,000

2,000,000

2,000,000

2,000,000

Common shares

1,500,000

1,500,000

3,400,000

3,400,000

Retained earnings

6,500,000

6,500,000

6,500,000

6,500,000

Total Equities

$20,950,000

$20,000,000

$22,850,000

$22,850,000

Only in the fourth alternative is Prairie’s statement of financial position really a

consolidated statement. In the first three alternatives, Prairie is buying the assets (or net

assets) of Savannah, and those assets will be recorded directly on Prairie’s books.

b. Share ownership and intercompany relationship:

Alternative

Company

Shares owned by

Intercompany

relationship

1

Prairie

Prairie’s prior shareholders

none

Savannah

2

Prairie

Prairie’s prior shareholders

none

Savannah

3

Prairie

80% by Prairie’s prior shareholders;

20% by Savannah Inc.

Prairie partially owned

by Savannah Inc.

Savannah

Savannah’s prior shareholders

4

Prairie

80% by Prairie’s prior shareholders;

Savannah wholly

find more resources at oneclass.com

find more resources at oneclass.com

Chapter 3 – Business Combinations

20% by Savannah Inc.

owned by Prairie Ltd.

Savannah

Prairie Ltd.

P3-2

Measure Step:

Case

A

B

C

D

E

F

Purchase price (a)

$120

$120

$100

$80

$100

$80

Carrying value of net identifiable assets (b)

80

100

80

100

120

120

Fair value of net identifiable assets (c)

100

80

120

120

80

100

Net fair value adjustment (a – b)

40

20

20

(20)

(20)

(40)

Fair value adjustment allocated to net identifiable assets

(c–b)

(20)

20

(40)

(20)

40

20

Balance = goodwill/(gain on bargin purchase) (a – c)

20

40

(20)

(40)

20

(20)

find more resources at oneclass.com

find more resources at oneclass.com

Chapter 3 – Business Combinations

P3-3

Measure Step:

100% Purchase of West Company Ltd., December 31, 20X6

Purchase price*

$600,000

Fair value of preferred shares*

250,000

Less carrying value of West’s net identifiable assets (100%)

(660,000)

= Fair Value Adjustment, allocated below

190,000

Carrying value

Fair

Fair value

FVA Allocated

(a)

Value

Adjustment

(b)

(c)=(b)–(a)

Current assets

$200,000

$250,000

$50,000

Capital assets, net

750,000

850,000

100,000

Current liabilities

(140,000)

(175,000)

(35,000)

Long-term liabilities

(150,000)

(220,000)

(70,000)

Preferred shares

(250,000)

(250,000)

0

45,000

Total fair value adjustment allocated to net identifiable

assets and preferred shares

(45,000)

Net asset carrying value

$660,000

Fair value of net identifiable assets acquired

$705,000

Balance of FVA allocated to goodwill

$145,000

The total fair value of West Company, including the value of the preferred shares is

$850,000. Under IFRS, the full fair value of the acquiree can also be calculated as the

purchase price paid by the acquirer for its shares plus the fair value of the non-controlling

interest. Under IFRS the fair value of preferred shares is treated as a non-controlling

interest.

Acquisition

Current assets

$450,000

Capital assets, net

1,750,000

Goodwill

245,000

Total assets

$2,445,000

Current liabilities

$265,000

Long-term liabilities

420,000

Total liabilities

685,000

Common shares

1,300,000

Retained earnings

210,000

Total share equity of East Ltd.

1,760,000

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Only in the fourth alternative is prairie"s statement of financial position really a consolidated statement. In the first three alternatives, prairie is buying the assets (or net assets) of savannah, and those assets will be recorded directly on prairie"s books: share ownership and intercompany relationship: 20% by savannah inc. owned by prairie ltd. Fair value adjustment allocated to net identifiable assets (c b) Balance = goodwill/(gain on bargin purchase) (a c) 100% purchase of west company ltd. , december 31, 20x6. Less carrying value of west"s net identifiable assets (100%) Total fair value adjustment allocated to net identifiable assets and preferred shares. The total fair value of west company, including the value of the preferred shares is. Under ifrs, the full fair value of the acquiree can also be calculated as the purchase price paid by the acquirer for its shares plus the fair value of the non-controlling interest.