ECON 2720 Lecture Notes - Lecture 4: Earnings Before Interest And Taxes, Contribution Margin, Income Statement

21 Jan 2017

School

Department

Course

Professor

Document Summary

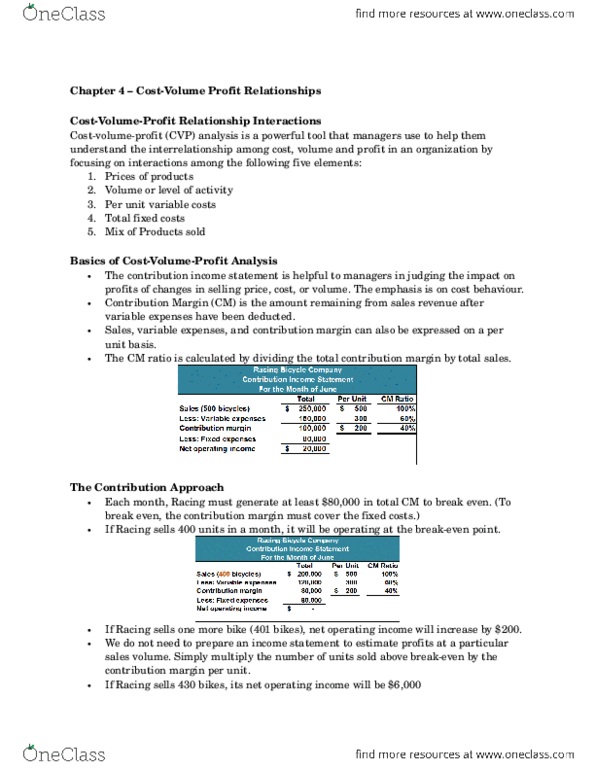

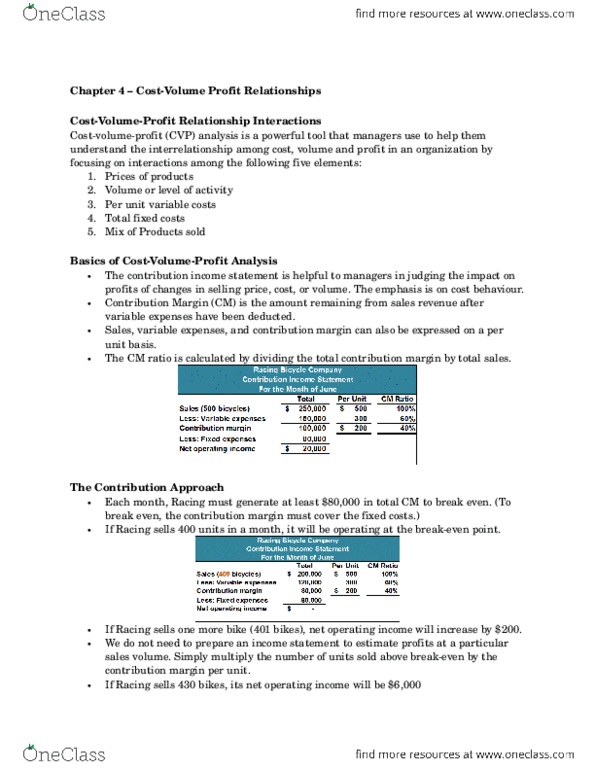

The contribution income statement is helpful to managers in judging the impact on profits of changes in selling price, cost, or volume. Contribution margin (cm) is the amount remaining from sales revenue after variable expenses have been deducted. Thus, it is the amount available to cover fixed expenses and then to provide profits for the period. The cm ratio is calculated by dividing the total contribution margin by total sales. The contribution margin ratio in terms of units is: Break-even point: the level of sales at which profit is zero. The break-even point can also be defined as the point where total sales equals total expenses, or as the point where total contribution margin equals total fixed expenses. Sales variable expenses fixed expenses = sh. Note: we do not need to prepare an income statement to estimate profits at a particular sales volume. Simply multiply the number of units sold above break-even by the contribution margin per unit.