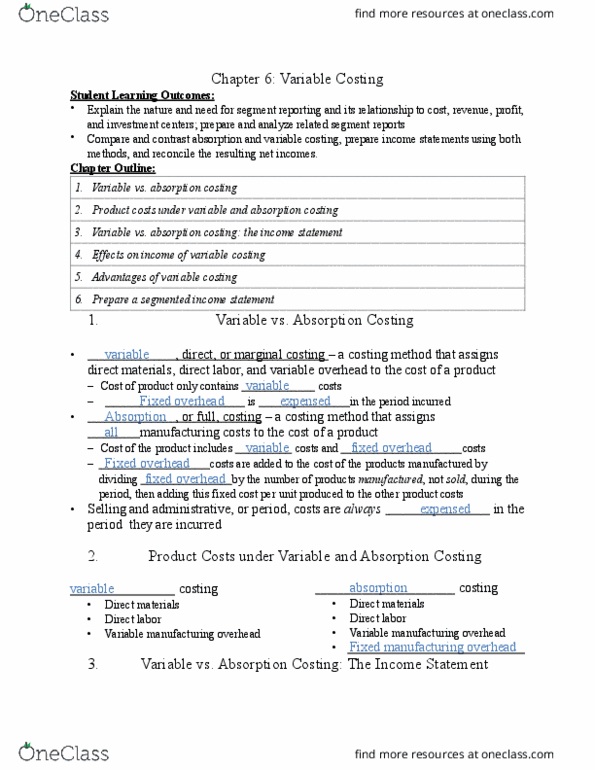

ACCT 311 Lecture Notes - Lecture 3: Cost Driver

25 Jun 2018

School

Department

Course

Professor

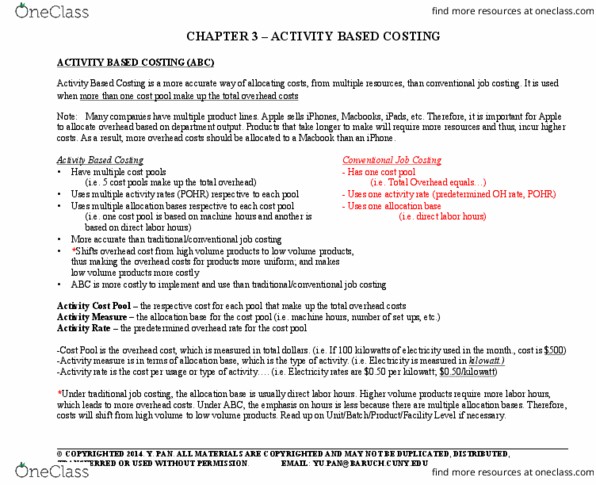

Chapter 3: Activity-Based Costing

Student Learning Outcomes:

•Discuss the impact of technology on the business environment, its implications for product and

service costs, and the development of activity-based costing and management.

Chapter Outline:

1. Assigning Overhead Costs to Products – 3 Methods

1. Plant - wide overhead rate

–Uses a single allocation base and overhead rate to assign overhead to products

–Is simple and usually uses direct labor as a base, but…

–Direct labor is becoming a smaller part of product costs and is not as meaningful in allocating

overhead as it once was

–No single allocation base may accurately allocate overhead for the whole plant

–Result is inaccurate product costs

2. Departmental overhead rate

–Uses a different allocation base and overhead rate for each processing department, but…

–Usually assumes that overhead is caused by machine hours

–Result is still inaccurate product costs

3. Activity - Based costing (ABC) – tries to trace overhead to the products that

cause it by using a number of allocation bases and overhead rates

2. Designing an ABC System

•Identifying the components of an ABC system

–Activity – an event that causes overhead to be used

–Activity cost pool – an accumulation of costs related to a particular activity

• unit -level activities – performed each time a unit is produced

• batch -level activities – performed each time a batch is made

• product -level activities – performed each time a product is made

• facility -level (organization-sustaining) activities – activities performed to sustain the

company

–Activity measure , allocation base, or cost driver – a measure of whatever

causes the costs in the pool

–Activity rate – predetermined overhead rate for that activity

1. Assigning overhead costs to products – 3 methods

2. Designing an ABC system

3. Allocating overhead to products

4. Evaluation of ABC

find more resources at oneclass.com

find more resources at oneclass.com

Document Summary

Student learning outcomes: discuss the impact of technology on the business environment, its implications for product and service costs, and the development of activity-based costing and management. Chapter outline: assigning overhead costs to products 3 methods, designing an abc system, allocating overhead to products, evaluation of abc, assigning overhead costs to products 3 methods. 3. allocation base and overhead rate to assign overhead to products. Is simple and usually uses direct labor as a base, but . Direct labor is becoming a smaller part of product costs and is not as meaningful in allocating overhead as it once was. No single allocation base may accurately allocate overhead for the whole plant. Uses a different allocation base and overhead rate for each processing department, but . Usually assumes that overhead is caused by machine hours. Activity an event that causes overhead to be used. An accumulation of costs related to a particular activity unit is made.