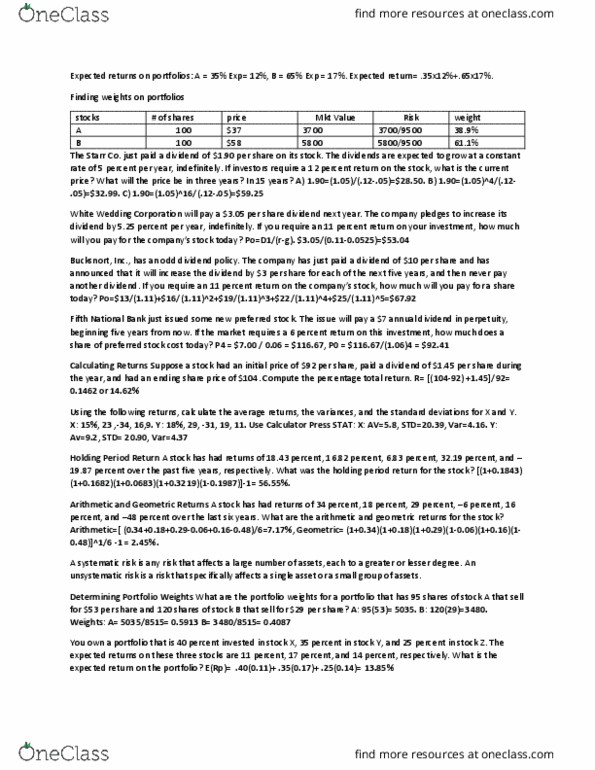

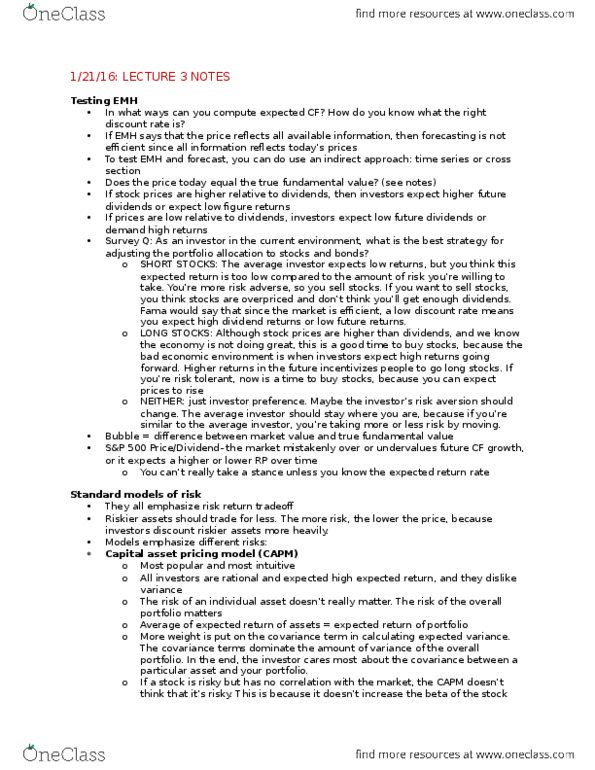

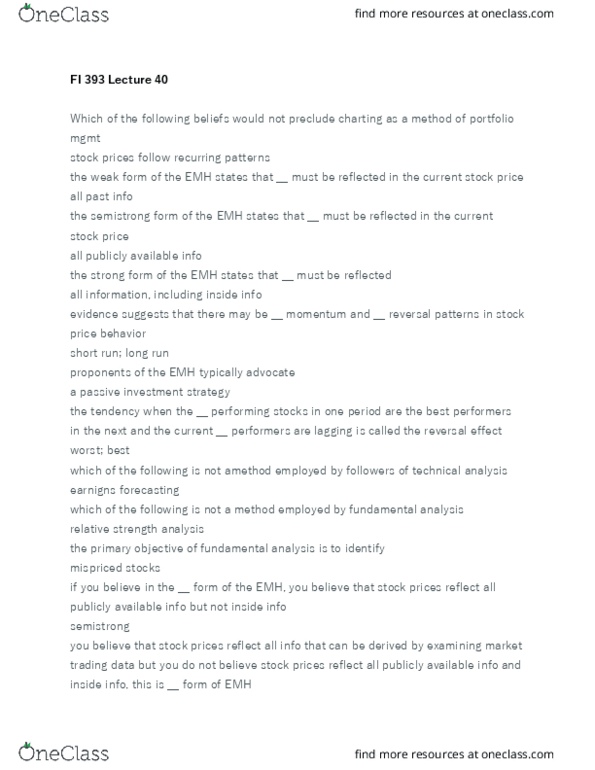

SOCIOL 182 Lecture Notes - Lecture 18: Capital Asset, Capital Asset Pricing Model, Efficient-Market Hypothesis

Document Summary

The tendency of poorly performing stocks and well-performing stocks in one period to continue their performance into the next period is called the. In the context of the capital asset pricing model, the systematic measure of risk is captured by. The weak form of the emh states that ________ must be reflected in the current stock price. All past information, including security price and volume data. In a well-diversified portfolio, __________ risk is negligible. Market value of assets minus liabilities divided by shares outstanding. Joe bought a stock at per share. Joe held on to the stock until it again reached , and then he sold it once he had eliminated his loss. If other investors do the same to establish a trading pattern, this would contradict. The beta of a security is equal to. The covariance between the security and market returns divided by the variance of the market"s returns. The expected return on the market is 18%.