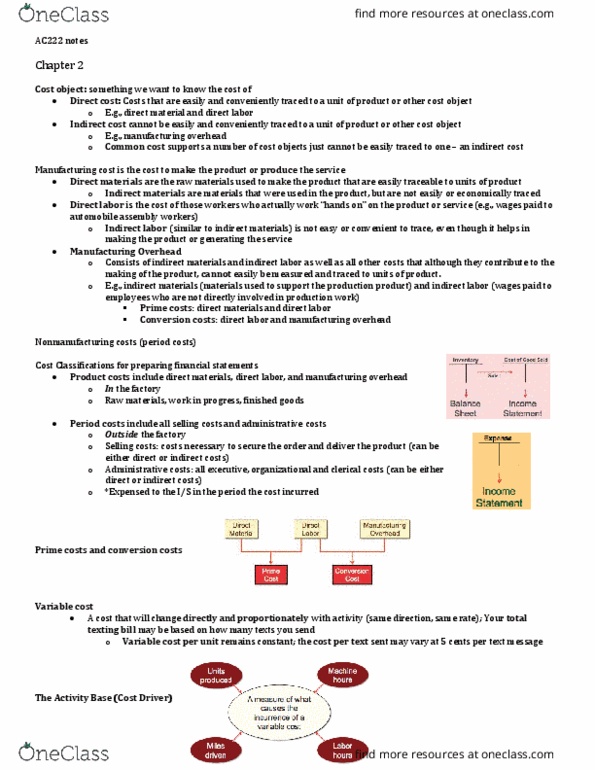

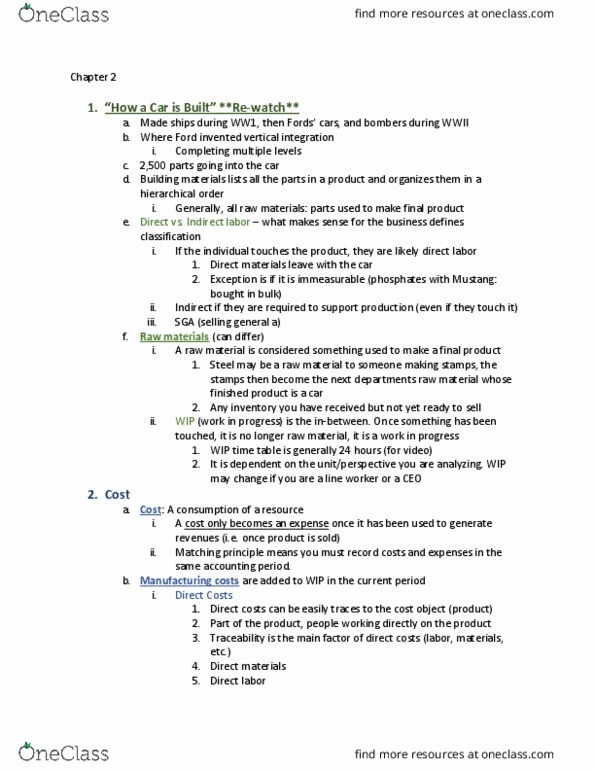

SMG AC 222 Lecture 10: AC Notes Chapter 10

Get access

Related Documents

Related Questions

The? Sudbury, South? Carolina, plant of Shannon Sports Companyhas the following standards for its soccer ball? production:

Standards: | 0.1 yard |

Material (leather) per soccer ball | $21 |

Material price per yard | 0.40 Hour |

Direct labor hours per soccer ball | $11 per hour |

Wage rate per direct labor hour | $12 per direct labor hour |

Variable support cost rate | |

Actual results for October: | |

| Used 13500 yards of raw material, purchased for $280,530.00. Paid for 8,200 direct labor hours at $11.30 per hour. Incurred $82,000 of variable support costs Manufactured 25,000 soccer balls |

Requirements

Determine the following variances for? October:

?(a) | Total direct material cost variance and indicate whether thevariance is favorable or unfavorable |

?(b) | Total direct labor cost variance |

?(c) | Total variable support cost variance |

?(d) | Direct material price variance |

?(e) | Direct material quantity variance |

?(f) | Direct labor rate variance |

?(g) | Direct labor efficiency variance |

?(h) | Variable support rate variance |

?(i) | Variable support efficiency variance |

AH? = Actual number of direct labor hours

AP? = Actual price per unit of materials

AQ? = Actual quantity of materials used

AR? = Actual wage rate

SH? = Number of direct labor hours allowed given the level ofoutput achieved

SP? = Estimated or standard price per unit of materials

SQ? = Standard quantity of materials allowed for the productionlevel achieved

SR? = Standard wage rate

Tharaldson Corporation makes a product with the following standard costs:

| Standard Quantity or Hours | Standard Price or Rate | Standard Cost per Unit | |

| Direct material | 6.6 ounces | $ 5.00 per ounce | $33.00 |

| Direct labor | 0.8 hours | $ 10.00 per hour | $8.00 |

| Variable overhead | 0.8 hours | $ 5.00 per hour | $4.00 |

The company reported the following results concerning this product in June.

| Originally budgeted output | 2,000 units |

| Actual output | 2,500 units |

| Raw materials used in production | 19,000 ounces |

| Purchases of raw materials | 21,500 ounces |

| Actual direct labor-hours | 4,900 hours |

| Actual cost of raw materials purchases | $40,500 |

| Actual direct labor cost | $12,000 |

| Actual variable overhead cost | $3,000 |

The company applies variable overhead on the basis of direct labor hours. The direct material purchases variance is computed when the materials are purchased .

The materials quantity variance for June is:

| Huron Company produces a commercial cleaning compound known as Zoom. The direct materials and direct labor standards for one unit of Zoom are given below: |

| Standard Quantity or Hours | Standard Price or Rate | Standard Cost | |||||

| Direct materials | 4.6 | pounds | $ | 2.50 | per pound | $ | 11.50 |

| Direct labor | 0.2 | hours | $ | 12.00 | per hour | $ | 2.40 |

| | |||||||

| During the most recent month, the following activity was recorded: |

| a. | Twenty thousand pounds of material were purchased at a cost of $2.35 per pound. |

| b. | The company produced only 3,000 units, using 14,750 pounds of material. (The rest of the material purchased remained in raw materials inventory.) |

| c. | 750 hours of direct labor time were recorded at a total labor cost of $10,425. |

| Required: | |||||||

| Compute the materials price and quantity variances for the month. (Indicate the effect of each variance by selecting "F" for favorable, "U" for unfavorable, and "None" for no effect (i.e., zero variance).)

| |||||||