CAS EC 101 Lecture Notes - Lecture 7: Form 10-Q, Marginal Cost, Fixed Cost

1 May 2018

School

Department

Course

Professor

CHAPTER 11: PRODUCER THEORY

Objective 1: Total, Average and Marginal Costs

• Total Cost (TC) – the total cost of producing q units of output

o ex: TC = 10q (simplistic)

▪ Results in an upwards sloping line on a graph

o However, this is not descriptive of most firms’ cost situation

o ex: TC = q3 + 2q3 + 3q + 5 (complex and more realistic)

▪ Results in a cubic sloping line on a graph

▪ Costs initially rise steeply, level off, then continue to rise steeply

• Average Cost (AC) – the average cost at any given output (q)

o Formula =

o ex: go from TC to AC for a simplistic TC

▪ TC = 10q, AC = 10q/q = 10

▪ Results in a horizontal line on a graph

o ex: go from TC to AC for a realistic TC

▪ TC = TC = q3 + 2q3 + 3q + 5, AC = q2 + 2q + 3

▪ Results in a parabolic shaped graph

• Marginal Cost (MC) – the cost of producing an additional unit of output

o Formula =

=

o ex: go from TC to MC for a realistic TC

▪ TC = 10Q, MC = 10q/q = 10

▪ Results in a horizontal line on a graph

o ex: go from TC to MC for a realistic TC

▪ TC = q3 + 2q3 + 3q + 5

▪ MC = 3q2 + 4q + 3

▪ Results in a fishhook shaped graph

• Relationship Between MC and AC

• The marginal value will always pull the average value in the direction it is going

o When the marginal cost is less than average cost, the average cost will be

declining (on a graph)

▪ This holds true even if average cost is rising

o When the marginal cost is equal to the average cost, the average cost will

remain flat (on a graph)

▪ Minimum Average Cost – when the average cost is at its lowest

▪ Will always be a singular point

o When the marginal cost is higher than average cost, the average cost will be

rising (on a graph)

Objective 2: Fixed and Variable Costs

• Total Cost = Total Fixed Costs + Total Variable Cost

o Total Fixed Costs (TFC) – costs that do not vary due to output (q)

▪ Essentially the costs that firms’ must pay even when they are not

producing goods

find more resources at oneclass.com

find more resources at oneclass.com

▪ ex: go from TC to TFC for a realistic TC

• TC = q3 + 2q3 + 3q + 5, TFC = 5

• Results in a graph with a distinct vertical intercept

▪ Important to note that TFC = TC when q is 0

o Total Variable Costs (TVC) – costs that do vary due to output (q)

▪ ex: go from TC to TVC for a realistic TC

• TC = q3 + 2q3 + 3q + 5, TVC = q3 + 2q3 + 3q

• Results in a graph with no vertical intercept (no starting output,

line will begin at 0)

• Average Cost = Average Fixed Costs (AFC) + Average Variable Costs (AVC)

o If q Increases – AFC decreases (away from AC), AVC increases (towards AC)

o If q Decreases – AFC increases (towards from AC), AVC decreases (away from

AC)

• Marginal Cost = Marginal Fixed Costs + Marginal Variable Costs

o Marginal Fixed Costs (MFC) – will always equal zero

o So: Marginal Cost = 0 + Marginal Variable Costs

o Marginal Cost = Marginal Variable Costs

Objective 3: Summary of Costs

Total

Fixed

Variable

Total

TC

TFC

TVC

Average

AC = TC/q

AFC = TFC/q

AVC = TVC/q

Marginal

MC = TC/q

MFC = TFC/q = 0

MVC = TVC/q = MC

• ex: find the AC, AFC, AVC and MC

o TFC = 6 at every level of output

o q – given

o TC – given

o AC –

o AFC –

o AVC – AC – AFC

o MC –

o TFC – when q = 0, TC = 6

q

TC

AC

AFC

AVC

MC

TFC

0

6

0

0

0

0

6

1

8

8

6

2

2

6

2

9

4.5

3

1.5

1

6

3

11

3.67

1

2.67

2

6

4

14

3.5

1.5

2

3

6

5

18

3.6

1.2

2.4

4

6

6

23

3.83

1

2.83

5

6

Objective 4: Revenue Concepts

• Total Revenue (TR) – the total revenue from producing q

find more resources at oneclass.com

find more resources at oneclass.com

o Formula = p x q, with p = the price per unit and q = the quantity of units sold

o ex: a gas station sells 1000 gallons of gas at $3 per gallon

▪ TR = 1,000 x $3 = $3,000

• Average Revenue (AR) – the average revenue a firm will make

o Formula =

=

= p

o Essentially, average revenue is the price

• Marginal Revenue (MR) – the additional revenue from selling the last unit

o Formula =

=

o ex: the 110th widget is sold for $40, so delta TR = 40 and delta q = 1

▪ MR = 40/1 = 40

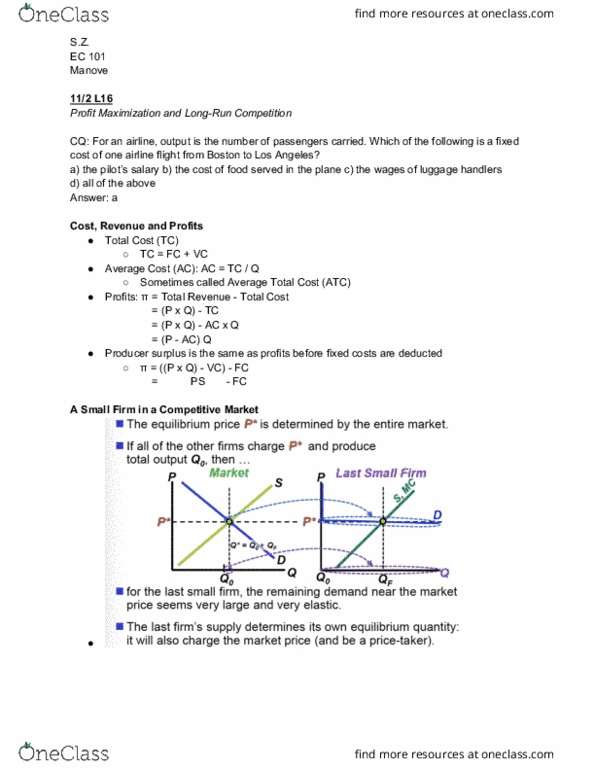

Objective 5: Perfectly Competitive Firm

• How is price determined?

o

• Market v. Firm

• Market – how many firms are in the market and how do they compete

o There will be a very large number of firms which prevents any single firm from

affecting price (ex: setting or changing prices)

o They determine price based on the market given price (which is determined by the

intersection of supply and demand)

▪ This results in firms being able to sell as much as they can produce

▪ But this means they can only sell as much as they produce

o Results in a graph with the supply and demand curves intersecting at the market

determined price (P*)

• Firm – must take and use the market determined price (P*)

o Results in a graph with a flat line (perfectly elastic) representing the market

determined price (P*)

o P* = Demand = Average Revenue = Marginal Revenue

• ex: what would happen if an individual firm tried to raise its price?

o They would sell zero products as buyers would consume goods from other firms

selling at the lower market determined price

• ex: what would happen if an individual firm tried to lower its price?

o They would continue to sell the same amount of product (would not make more or

less revenue)

find more resources at oneclass.com

find more resources at oneclass.com

56

CAS EC 101 Full Course Notes

Verified Note

56 documents

Document Summary

Ac: marginal cost = marginal fixed costs + marginal variable costs, marginal fixed costs (mfc) will always equal zero, so: marginal cost = 0 + marginal variable costs, marginal cost = marginal variable costs. Marginal mc = tc/ q mfc = tfc/ q = 0 mvc = tvc/ q = mc: ex: find the ac, afc, avc and mc. Tvc: tfc = 6 at every level of output, q given, tc given, ac (cid:3044, afc (cid:3044, mc (cid:3044, avc ac afc, tfc when q = 0, tc = 6. = p: essentially, average revenue is the price, formula = (cid:3019)(cid:3044) = (cid:4666)(cid:3043) (cid:3044)(cid:4667)(cid:3044, formula = (cid:3019) (cid:3018) = c(cid:2918)a(cid:2924)(cid:2917)e (cid:2919)(cid:2924) (cid:2930)(cid:2925)(cid:2930)al (cid:2928)e(cid:2932)e(cid:2924)(cid:2931)e c(cid:2918)a(cid:2924)(cid:2917)e (cid:2919)(cid:2924) (cid:2930)(cid:2925)(cid:2930)al (cid:2925)(cid:2931)(cid:2930)(cid:2926)(cid:2931)(cid:2930, mr = 40/1 = 40. In the short run, a firm has fixed costs. In the long run, a firm has variable costs. Objective 9: firms" supply curve market supply curve.