BUS 215 Lecture Notes - Lecture 3: Cost Driver

Document Summary

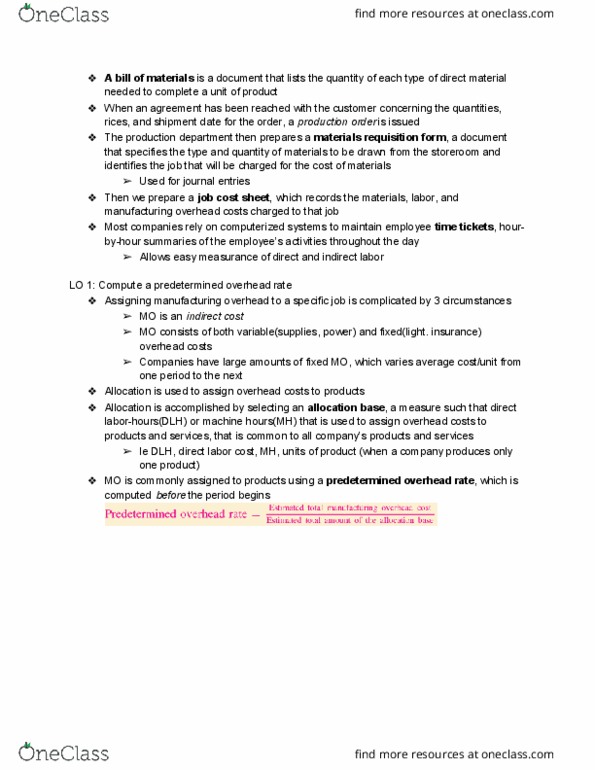

Direct materials + direct labor +manufacturing overhead applied = Manufacturing costs: charge direct material and direct labor costs to each job as work is performed, manufacturing overhead, including indirect materials and indirect labor, are allocated to all jobs rather than directly traced to each job. Compute predetermined overhead rate: step 1: estimated variable + estimated fixed manufacturing. Overhead divided by cost driver = pohr (direct labor hours, direct machine hours, direct labor $: step 2: pohr x actual cost driver = manufacturing overhead. Applied (ignore all estimates once this rate is found) It is impossible or difficult to trace overhead costs to particular jobs. Manufacturing overhead consists of many different items ranging from the grease used in machines to the production manager"s salary. Many types of manufacturing overhead costs are fixed even though output fluctuates during the period. Account for nonmanufacturing cost: nonmanufacturing costs are not assigned to individual jobs, rather they are expensed in the period incurred.