ECON 2010 Lecture Notes - Lecture 8: Inferior Good, Normal Good

25 Sep 2018

School

Department

Course

Professor

ECON 2010 verified notes

8/47View all

Ch. 5 Elasticity & Its Application

Wednesday, September 12, 2018

10:02 AM

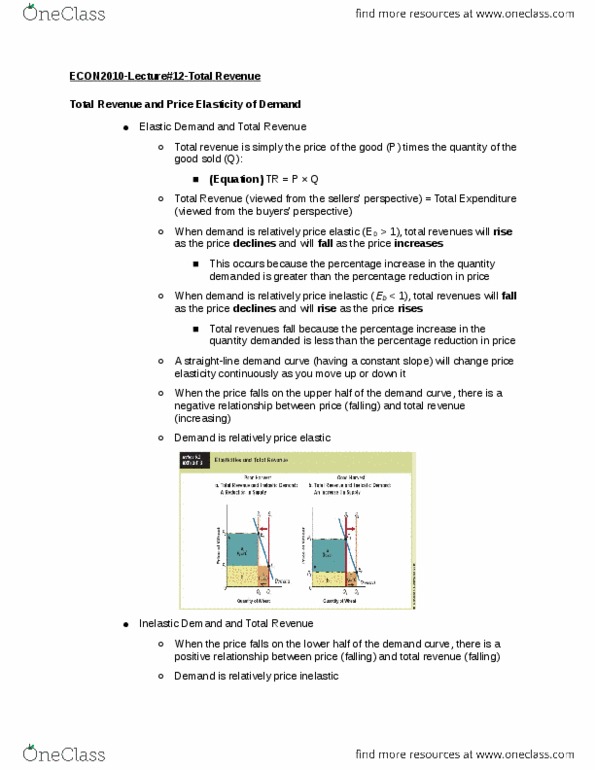

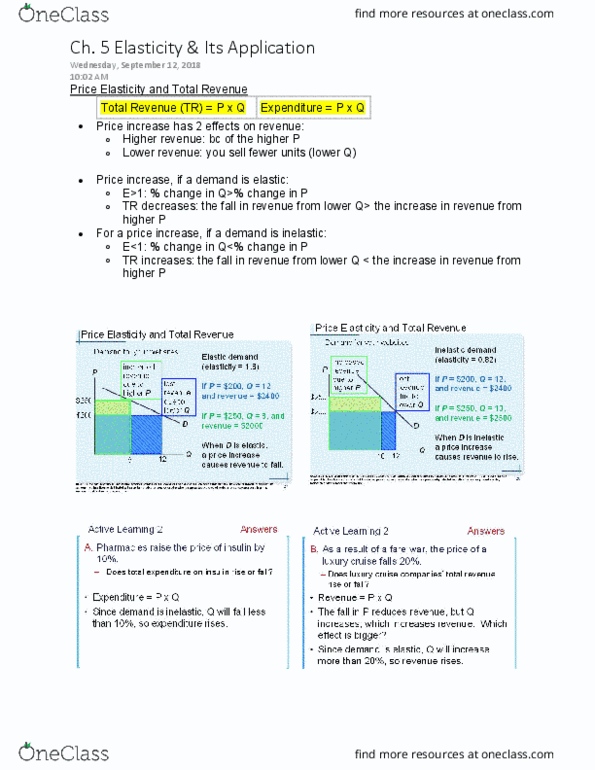

Price Elasticity and Total Revenue

Total Revenue (TR) = P x Q

Expenditure = P x Q

• Price increase has 2 effects on revenue:

o Higher revenue: bc of the higher P

o Lower revenue: you sell fewer units (lower Q)

• Price increase, if a demand is elastic:

o E>1: % change in Q>% change in P

o TR decreases: the fall in revenue from lower Q> the increase in revenue from

higher P

• For a price increase, if a demand is inelastic:

o E<1: % change in Q<% change in P

o TR increases: the fall in revenue from lower Q < the increase in revenue from

higher P

Ch. 5 Elasticity & Its Application

Wednesday, September 12, 2018

10:02 AM

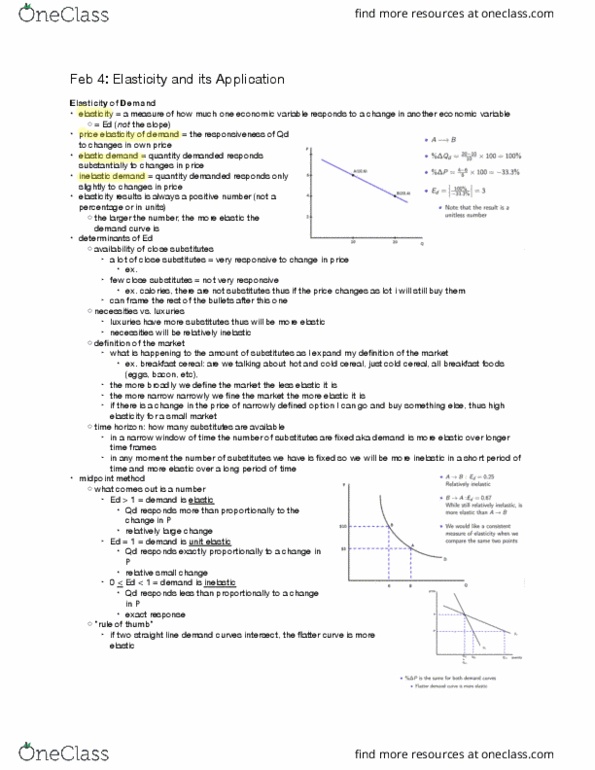

Price Elasticity of Supply

• Price elasticity of supply: how much the quantity supplied of a good responds to a

change in the price of that good

o % change in quantity supplied

% change change in price

o Measures sellers' price-sensitivity

• Variety of supply curves

o Supply is unit elastic

▪ Price elasticity of supply = 1

o Supply is elastic

▪ Price elasticity of supply > 1

o Supply is inelastic

▪ Price elasticity of supply < 1

o Supply is perfectly inelastic

▪ Price elasticity of supply = 0

▪ Supply curve is vertical

o Supply is perfectly elastic

▪ Price elasticity of supply = infinity

▪ Supply curve is horizontal

• The flatter the supply curve, the greater the price elasticity of supply

• Magnitude of the change in quantity is greater than the change in supply

Document Summary

Price elasticity of supply: price elasticity of supply: how much the quantity supplied of a good responds to a change in the price of that good, % change in quantity supplied. In the long run: firms can build new factories, or new firms may be able to enter the market. Normal good: any good for which demand increases when income increases (i. e. with positive income elasticity of demand) Inferior good: any good for which demand declines when income rises a. Income elasticities of demand: how much the quantity demanded of a good responds to a change in comsumers" income, % change in quantity demanded, divided by the percentage change in income, normal goods: income elasticity > 0. Increase of price of beef causes an increase in demand for chicken: complements: cross-price elasticity < 0. Increase in price of computers causes decrease in demand for software.