ACC 201 Lecture Notes - Lecture 11: Treasury Stock, Retained Earnings

24 Apr 2017

School

Department

Course

Professor

Document Summary

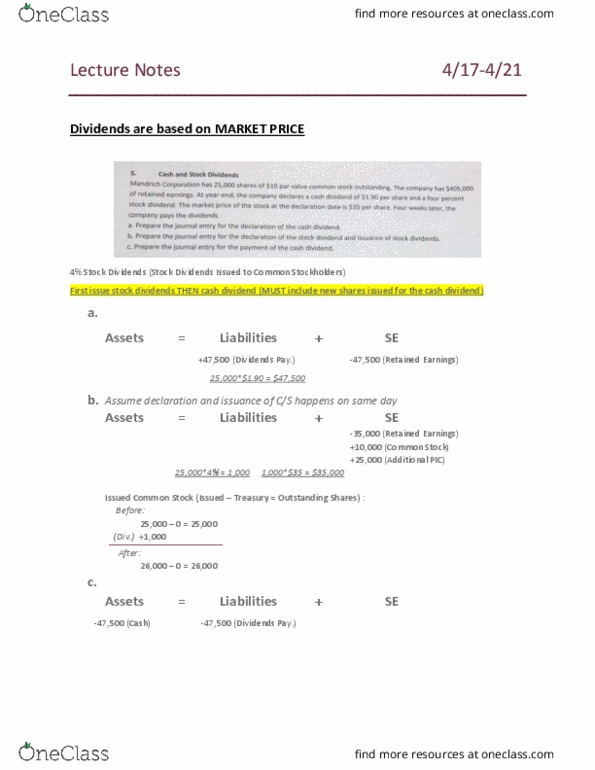

Treasury stock (shares repurchased by company) (se dec. ) Authorized shares maximum number of shares a company can issue. Advantages: dividends are decided in advance, preference in case of liquidation. Dividend = 8%*50=/share annually: issues 25,000 of par value stock for per share, purchases 3,000 c/s for per share (turns into treasury stock) sets new par value for the treasury stock: sells 2,000 shares of treasury stock at per share, sells 1,000 shares of treasury stock at per share. Liabilities: +425,000 (cash, -60,000 (cash, +52,000 (cash, +19,000 (cash) 4,000 shares at (4,000 shares total) 1,000 shares sold at ( pv) (3,000 t/s outstanding) 500 shares sold at ( pv) (2,500 t/s outstanding) 5,000 shares sold at ( pv) (45,000 p/s outstanding) Common stock: 50,000 + 125,000 35,000 + 122,500 + 75,000 = ,500.