ACC 131 Lecture Notes - Lecture 7: Fixed Asset, Land Development, Historical Cost

Document Summary

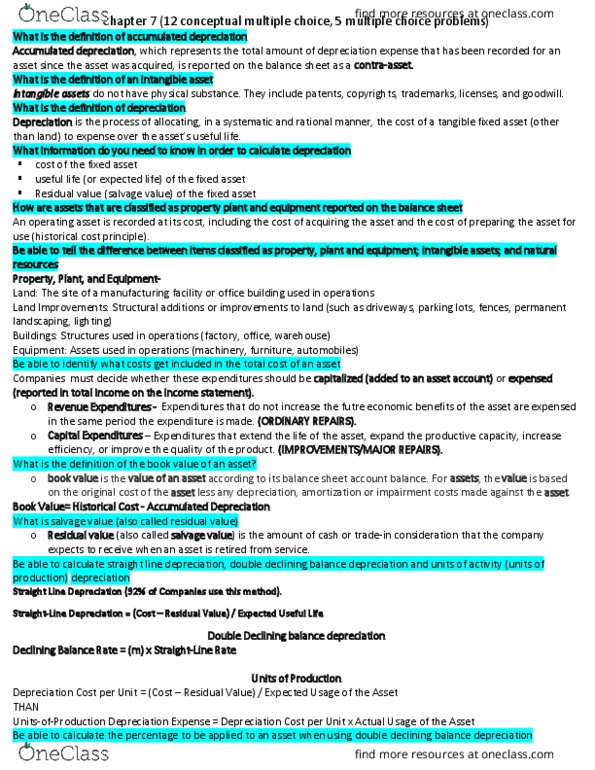

Operating assets are the long-lived assets that are used by the company in the normal course of operations. Operating assets are divided into three categories: Instead, operating assets are used by a company in the normal course of operations to generate revenue. Property, plant, and equipment are often called fixed assets or plant assets. You can see them, look at them, touch them. They include patents, copyrights, trademarks, licenses, and goodwill. La(cid:272)ks physi(cid:272)al su(cid:271)stan(cid:272)e. can"t tou(cid:272)h it, feel it. They include timberlands and deposits such as coal, oil, and gravel. A company for instance, uses trees, cuts them down, to make paper. Operating assets represent future economic benefits, or service potential, that will be used in the normal course of operations. At acquisition, an operating asset is recorded at its cost, including the cost of acquiring the asset and the cost of preparing the asset for use (historical cost principle).