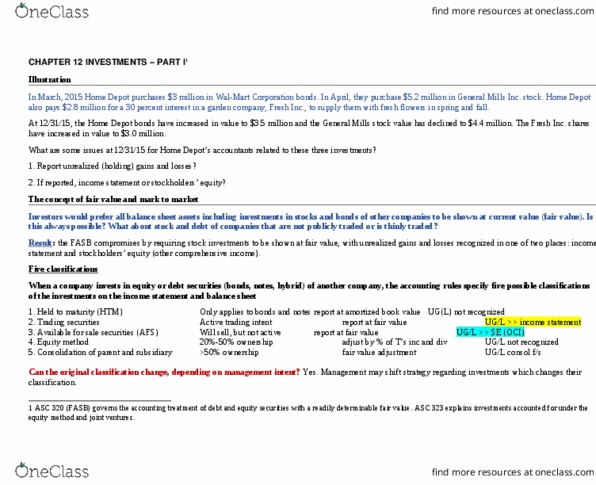

ACCT 4050 Lecture Notes - Lecture 1: Finance Lease, Operating Lease, Financial Statement

Document Summary

Get access

Related Documents

Related Questions

# Warren Co. recorded a right-of-use asset of $800,000 in a10-year Type A lease. The interest rate charged by the lessor was8%. Under the new ASU, the balance in the right-of-use asset aftertwo years will be:

#Refer to the following lease amortization schedule. The 10payments are made annually starting with the inception of thelease. Title does not transfer to the lessee and there is nobargain purchase option or guaranteed residual value. The asset hasan expected economic life of 12 years. The lease isnoncancelable.

| Payment | Cash Payment | Effective Interest | Decrease in balance | Balance |

| 63,282 | ||||

| 1 | 10,000 | 10,000 | 53,282 | |

| 2 | 10,000 | 6,394 | 3,606 | 49,676 |

| 3 | 10,000 | 5,961 | 4,039 | 45,638 |

| 4 | 10,000 | 5,477 | 4,523 | 41,114 |

| 5 | 10,000 | 4,934 | 5,066 | 36,048 |

| 6 | 10,000 | 4,326 | 5,674 | 30,373 |

| 7 | 10,000 | 3,645 | 6,355 | 24,018 |

| 8 | 10,000 | 2,882 | 7,118 | 16,901 |

| 9 | 10,000 | ? | ? | ? |

| 10 | 10,000 | ? | ? | ? |

What would the lessee record as annual depreciation on the assetusing the straight-line method?

#XYZ Company leased equipment to West Corporation under a leaseagreement that qualifies as a capital lease to West but not as aresult of a bargain purchase option or a title transfer. Thepresent value of the asset is $600,000. The expected economic lifeof the asset is 10 years. The lease term is five years. Using thestraight-line method, what would West record as annualdepreciation?

# If the lessee and lessor use different interest rates toaccount for a capital lease, then:

Total expenses for the lessee will be different from thelessor's total revenues.

Total expenses for the lessee will equal the lessor's totalrevenues.

GAAP has been violated by at least one party.

The lessee will report more net income for the year.

##

Technoid Inc. sells computer systems. Technoid leases computersto Lone Star Company on January 1, 2016. The manufacturing cost ofthe computers was $12 million.

This noncancelable lease had the following terms:

⢠Lease payments: $2,466,754 semiannually; first payment at January1, 2016; remaining payments at June 30 and December 31 each yearthrough June 30, 2020.

⢠Lease term: five years (10 semiannual payments).

⢠No residual value; no bargain purchase option.

⢠Economic life of equipment: five years.

⢠Implicit interest rate and lessee's incremental borrowing rate:5% semiannually.

⢠Fair value of the computers at January 1, 2016: $20million.

Collectibility of the rental payments is reasonably assured, andthere are no lessor costs yet to be incurred.

Lone Star Company would account for this as:

A capital lease.

A direct financing lease.

A sales type lease.

An operating lease.

##

Refer to the following lease amortization schedule. The 10payments are made annually starting with the inception of thelease. Title does not transfer to the lessee and there is nobargain purchase option or guaranteed residual value. The asset hasan expected economic life of 12 years. The lease isnoncancelable.

| Payment | Cash Payment | Effective Interest | Decrease in balance | Balance |

| 63,282 | ||||

| 1 | 10,000 | 10,000 | 53,282 | |

| 2 | 10,000 | 6,394 | 3,606 | 49,676 |

| 3 | 10,000 | 5,961 | 4,039 | 45,638 |

| 4 | 10,000 | 5,477 | 4,523 | 41,114 |

| 5 | 10,000 | 4,934 | 5,066 | 36,048 |

| 6 | 10,000 | 4,326 | 5,674 | 30,373 |

| 7 | 10,000 | 3,645 | 6,355 | 24,018 |

| 8 | 10,000 | 2,882 | 7,118 | 16,901 |

| 9 | 10,000 | ? | ? | ? |

| 10 | 10,000 | ? | ? | ? |

What would be the outstanding balance after payment 10?

## Cady Salons leased equipment from Smith Co. on January 1,2016, in a Type B lease. The present value of the lease paymentsdiscounted at 10% was $80,000. Ten annual lease payments of $12,000are due at each January 1 beginning January 1, 2016. Following theguidance of the new ASU, the amortization of the right-of-use assetfor the reporting year ending December 31, 2016, would be:

## Karla Salons leased equipment from Smith Co. on July 1, 2016,in a Type A lease. The present value of the lease paymentsdiscounted at 10% was $80,000. Ten annual lease payments of $12,000are due each year beginning July 1, 2016. Smith Co. had constructedthe equipment recently for $66,000, and its retail fair value was$80,000.

Under the new ASU, what amount of interest revenue from the leaseshould Smith Co. report in its December 31, 2016, incomestatement?

### If the leaseback portion of a sale-leaseback transaction isclassified as an operating lease:

Any gain is deferred and recognized as a reduction of rentexpense.

Any gain is deferred and recognized as a reduction ofdepreciation.

Any gain is recognized at the lease's inception.

There can be no gain.

Analyzing and Interpreting Footnote on Operating and Capital Leases

Assume Verizon Communications, Inc., provides the following footnote relating to its leasing activities in its 10-K report. The aggregate minimum rental commitments under noncancelable leases for the periods shown at December 31, 2010, are as follows:

| Years (dollars in millions) | Capital Leases | Operating Leases |

|---|---|---|

| 2011 | $ 83 | $ 1,449 |

| 2012 | 71 | 1,316 |

| 2013 | 67 | 1,056 |

| 2014 | 63 | 806 |

| 2015 | 46 | 527 |

| Thereafter | 161 | 1,937 |

| Total minimum rental commitments | 491 | $ 7,091 |

| Less interest and executory costs | (89) | |

| Present value of minimum lease payments | 402 | |

| Less current installments | (46) | |

| Long-term obligation at December 31, 2010 | $ 356 |

(a) Confirm that the implicit discount rate for Verizon's capital leases is 5.01%.

| N | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 |

| Amount | Answer | Answer | Answer | Answer | Answer | Answer | Answer | Answer | Answer | Answer |

| IRR | Answer % |

(b) What effect does the failure to capitalize operating leases have on Verizon's balance sheet? Over the life of its leases, what effect does this lease classification have on net income?

There is no effect on the balance sheet and income statement as a result of the classification of leases.

Total assets and total liabilities are higher than if the operating lease had been classified as a capital lease. Over the lease term, total rent expense under operating leases will be equal to the interest and depreciation expense that the company would record under capital leases.

Total assets and total liabilities are lower than if the operating lease had been classified as a capital lease. Over the lease term, total rent expense under operating leases will be equal to the interest and depreciation expense that the company would record under capital leases.

Total assets and total liabilities are lower than if the operating lease had been classified as a capital lease. Over the lease term, total rent expense under operating leases will be greater than the interest and depreciation expense that the company would record under capital leases.

1.00 points out of 1.00

(c) Compute the present value of Verizon's operating leases, assuming an 5.01% discount rate and rounding the remaining lease term to 3 decimal places. (Use a financial calculator or Excel to compute. Do not round until your final answers. Round each answer to the nearest whole number.)

| ($ millions) | Present Value |

|---|---|

| Year 1 | Answer |

| Year 2 | Answer |

| Year 3 | Answer |

| Year 4 | Answer |

| Year 5 | Answer |

| After 5 | Answer |

| Total* | Answer |

* (Use subsequent rounded answers for calculation.)

Which of the following statements best describes how we might use this additional information in our analysis of the company?

To assess the company's financial condition and performance, we might add the present value of its operating leases to both operating assets and nonoperating liabilities. No adjustment is necessary for the income statement.

To assess the company's financial condition and performance, we might add the sum of the contractual payments under the operating leases to both assets and nonoperating liabilities, and we can replace rent expense with the depreciation of the lease assets and the interest on the lease liability.

To assess the company's financial condition and performance, we might add the present value of its operating leases to both operating assets and nonoperating liabilities, and we can replace rent expense with the depreciation of the lease assets and the interest on the lease liability.

Verizon's balance sheet and income statement are prepared in accordance with GAAP. No adjustments are necessary to evaluate the financial condition of the company.

1.00 points out of 1.00