ACCT 4050 Lecture Notes - Lecture 4: Contingent Liability, Current Liability, Gift Card

Document Summary

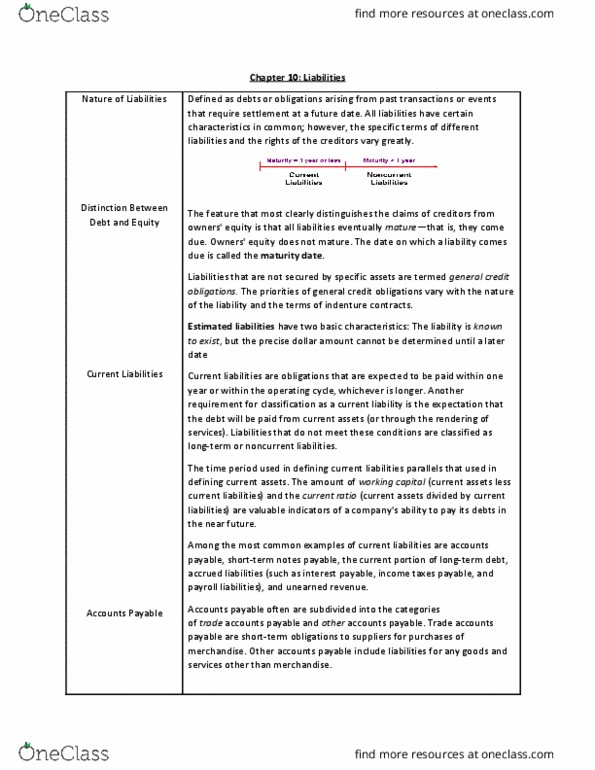

From a financial reporting perspective, a liability has three essential characteristics: are probable, future sacrifices of economic benefits, arise from present obligations (to transfer assets or provide services) to other entities, result from past transactions or events. Current liability: those expected to be satisfied with current assets or by the creation of other current liabilities. (most current liabilities are expected to require current assets and usually are payable within one year) Benefit of classification: helps investors and creditors assess the risk that the liabilities will require expenditure of cash or other assets in the near term. Accounts payable: obligations to suppliers of merchandise or of services purchased on open account. Most trade credit is offered on open account. This means that the only formal credit instrument is the invoice. Because the time until payment usually is short (often 30, 45, or 60 days), these liabilities typically are noninterest-bearing and are reported at their face amounts.