DOZIER INDUSTRIES (B)

Richard Rothschild, the chief financial officer of DozierIndustries, was still contemplating how best to manage the exchangerisk related to the company's new sales contract. The £1,057,500balance of the contract was due in three months on April 14, 1986,creating a long position in British pounds. Rothschild had spokenpreviously to John Gunn, an officer in the International Divisionof Southeastern National Bank, about hedging his long poundexposure. Gunn had explained two alternatives available to Dozierto reduce the exchange risk: a forward contract or a spottransaction. Either transaction would ensure that Dozier receive aset dollar value for its pound receivable, regardless of any changein the value of the pound. Given his previous analysis of theforeign exchange market, Rothschild was concerned that both ofthese hedging alternatives would lock in a profit margin below the6% he had originally anticipated for the contract. He wondered ifthere were some way to get the upside potential without all therisk.

The pound had weakened since his bid submission date on December3 (see Exhibit 1), but he was not entirelyconvinced it would continue to fall, or at least not as much as theforward rate indicated. If the future spot rate were greater thanthe current forward rate, an unhedged position could lead to again, whereas a hedged position would create an opportunity lost.Rothschild wondered if other alternatives were available, and heagain called John Gunn at the bank for advice.

Gunn explained that Rothschild could also use currency optionsto hedge against his uncertain foreign exchange exposure. Optionsprovide a means of hedging against volatility without taking aposition on expected future rates. Gunn explained that there aretwo basic varieties of options contracts: "puts" and "calls." A putgives the holder the right, but not the obligation, to sell foreigncurrency at a set exercise or "strike" price within a specifiedtime period. A call gives the holder the right to buy foreigncurrency at a set price. In comparison with a forward or futurescontract, the holder of an option does not have to transact at theagreed-upon price, but has the choice or option to do so. Gunn toldRothschild that options are complicated and increase the front endcost of hedging in comparison with a forward hedge. He saidRothschild could find the prevailing option contract prices in theWall Street Journal (see Exhibit 2).

EXHIBIT 1

HISTORICAL SPOT RATE AND FORWARD POUND IN U.S DOLLARS

DATE SPOT 3- MONTH FORWARD RATE

07/08/85 1.3640 1.3490

07/16 1.3880 1.3744

07/23 1.4090 1.3963

07/30 1.4170 1.4067

08/6 1.3405 1.3296

08/13 1.3940 1.3828

08/20 1.3900 1.3784

08/27 1.3940 1.3817

09/4 1.3665 1.3553

09/10 1.3065 1.2960

09/17 1.3330 1.3226

09/24 1.4200 1.4089

10/1 1.4120 1.4005

10/8 1.4155 1.4039

10/15 1.4120 1.4007

10/22 1.4290 1.4171

10/29 1.4390 1.4270

11/5 1.4315 1.4194

11/12 1.4158 1.4037

11/19 1.4320 1.4200

11/26 1.4750 1.4628

12/3 1.4820 1.4704

12/10 1.4338 1.4214

12/17 1.4380 1.4249

12/23 1.4245 1.4114

12/30 1.4390 1.4260

01/7/86 1.4420 1.4284

1/14/86 1.4370 1.4198

EXHIBIT 2

FOREIGN CURRENCY OPTIONS ON JANUARY 14,1986

OPTION& STRIKEPRICE CALLS-LAST PUTS-LAST

UNDERLYING CENT PERUNIT JAN. FEB.MAR. JAN. FEB. MAR.

Bpound 130 S R 13.50 S R R

144.41 135 S R 9.20 S 0.20 0.50

144.41 140 S 4.50 4.75 S 0.80 1.55

144.41 145 s 1.35 2.50 s 3.10 4.40

144.41 150 s 0.40 0.90 s r r

r- not traded s- no option offered. andLast is premium (purchase price)

Dozier Industries (B)

FOREIGN CURRENCY IPTIONS ON DECEMBER 3,1985

OPTIONS& STRIKEPRICE CALLS-LAST PUTS-LAST

UNDERLYING CENT PERUNIT DEC. JAN. MAR. DEC. JAN. MAR.

Bpound 120 29.00 S 28.95 R S R

148.86 130 19.10 R R R R R

148.86 135 13.80 R 14.60 0.05 R R

148.86 140 8.80 R 10.00 0.05 R S

148.86 145 4.00 4.50 5.70 0.20 1.05 3.20

148.86 150 0.65 1.65 3.35 R R 5.60

148.86 155 R 0.50 1.70 R R R

R- NOTTRADED S- NO OPTIONS OFFERED. LAST IS THE PREMIUM(PURCHASE PRICE)

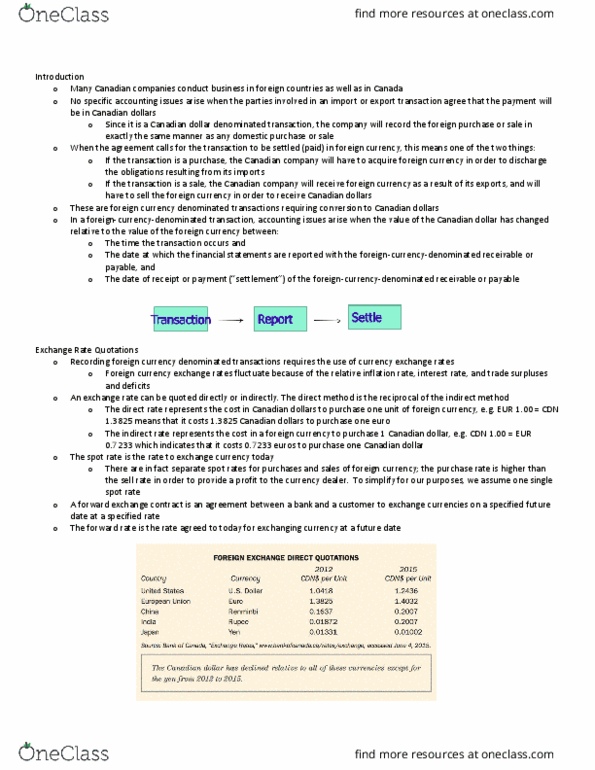

Case B: Additional Information

1. You should treat January 14, 1986 as the date when you areperforming your analysis and acting on the analysis (hedging or nothedging).

2. To reduce risk, Dozier will take the 10% initial deposit(pounds) and sell the pounds in the spot market on Jan 14.

3. Any dollars that Dozier receives on Jan 14 are deposited in thebank for 90 days.

4. For the purpose of your calculations, you may ignore the factthat currency option contracts for the pound come in 12,500 poundincrements. However, you may discuss this limitation qualitativelyin making your recommendation (last discussion question)below.

5. None of the option contracts mature on Apr 14, 1986. Ideally,Dozier would want an option that matures on that date for thepurpose of hedging. In deciding which option maturity is best (Febor Mar), you should consider this problem and choose the maturitythat best meets Dozierâs hedging objective. First choose the optionmaturity that best meets Dozierâs objective. Then in yourcalculations below, you may treat the options as if they mature Apr14. Qualitatively, however, you should consider this maturitymismatch in making your recommendation (last discussion question)below.

6. In exhibit 2, 144.41 U.S. cents per pound refers to the spotrate for the pound on Jan 14. This is inconsistent with what isreported elsewhere in both the A and B parts of this case. Continueto use the spot rate given in part A of this case for 1/14/86. Forthe rest of the table the rows correspond to a strike price between130 cents and 150 cents per pound. The columns correspond to eithercall options or put options with either Jan, Feb, or Marchmaturities. Any entry in the table (for example 0.50 cents perpound) is the option premium. In this example, 0.50 cents per poundis the premium for a put option with a March maturity and a strikeprice of 135 cents per pound.

First read the âBâ case, and then address the followingquestions:

1. Do you recommend using a call or put option to hedge theexchange rate risk? Explain.

2. Do you recommend an option with expiration in Feb. orMarch?

3. Calculate the U.S. dollar profit or loss for each possibleoutcome; there will be more than one possible outcome for eachoption. Recall that with an option, the option does not have to beexercised; the holder may choose to trade in the future spotmarket. The holderâs choice depends on the future spot rate. Note:You will do these calculations for either all of the call optionsor all of the put options and for either all of the Feb or all ofthe March options, depending on your answer to the first twoquestions above. Hint: Since Dozierâs motive is hedging, you firstcalculate the revenue in dollars that Dozier will receive for thePound receivable. Then subtract Dozierâs Costs given in Case Aexhibit 3.

4. Which option do you recommend? Explain. Note: You must nowselect one of the options with a given maturity and strikeprice.

5. Compare the option hedge to the forward hedge (in the A case)and to remaining unhedged. Which do you recommend? Explain.