ECON 2 Lecture Notes - Lecture 8: Comprehensive Income, Deferred Compensation, Pension Fund

Document Summary

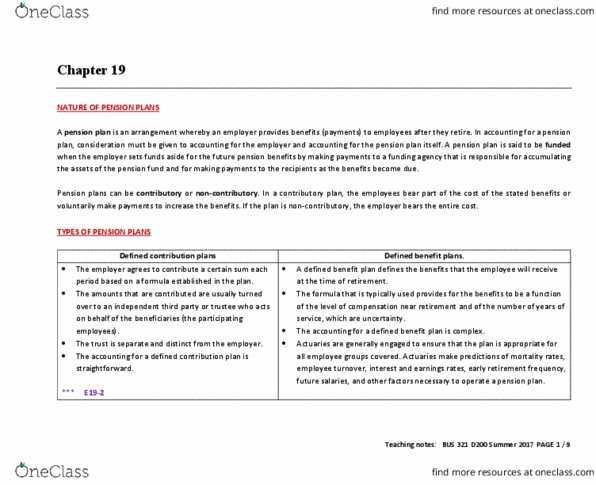

Chapter 20 accounting for pensions and postretirement benefits. Pension plan: arrangement whereby an employer provides benefits (payments) to retired employees for services they provided in their working years. Funded when the employer makes payments to a funding agency. Contributory: employees bear part of the cost of the stated benefits or voluntarily make payments to increase their benefits. Qualified pension plans: plans that offer tax benefits: deductibility of the employer"s contribution to the pension fund and tax-free status of earnings from pension fund assets, should be separate legal and accounting entity. Actuaries: ensure that a pension plan is appropriate for the employee group covered. Are individuals trained through a long and rigorous certification program to assign probabilities to future events and their financial effects. Make predictions actuarial assumptions: mortality rates, employee turnover, interest and earnings rates, early retirements frequency, future salaries, and other factors to operate pension plans.