ACC 201 Lecture Notes - Lecture 2: Operating Lease, Accrued Interest, Deferred Tax

Document Summary

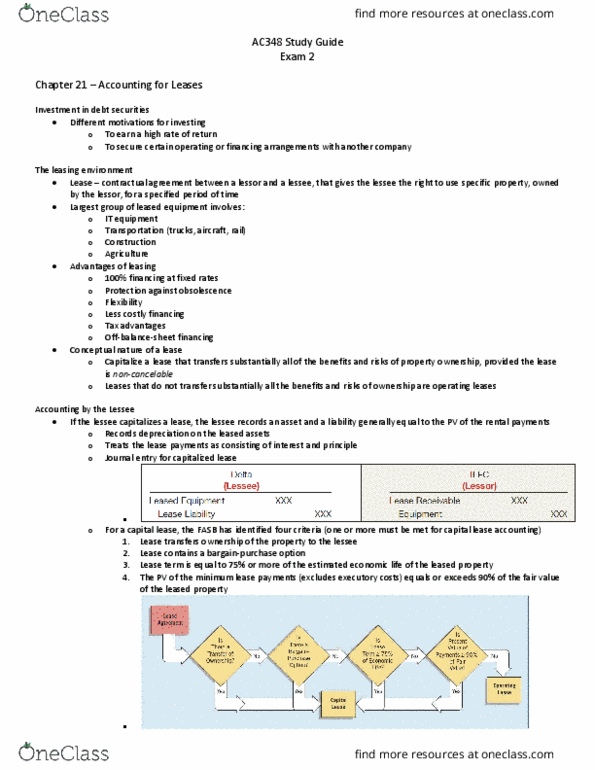

Record depreciation and treat lease payments like (cid:494)interest and principle. (cid:495) Lease term =or more than 75% of economic life of lease property (bargain renew included) Present value of minimum lease payments(without executory costs insurance maintenance taxes)=or more than 90% of fair value (compute pv with lower of their or lessors, if they know lessors) If it(cid:495)s not one of those, operating lease. Asset and liability recorded at lower of fmv or pv of lease payments +pv of bargain purchase option (without other costs) If lease transfers ownership, depreciate over economic life, if no transfer, depreciate over term of lease. Record accrued interest at end of year: (no interest on first payment) If guaranteed, then included in minimum lease payments. Adj fs for each period for new principle and adj carrying amounts from first year of asset or liability, and opening re. No entry to record correction, just record going forward.