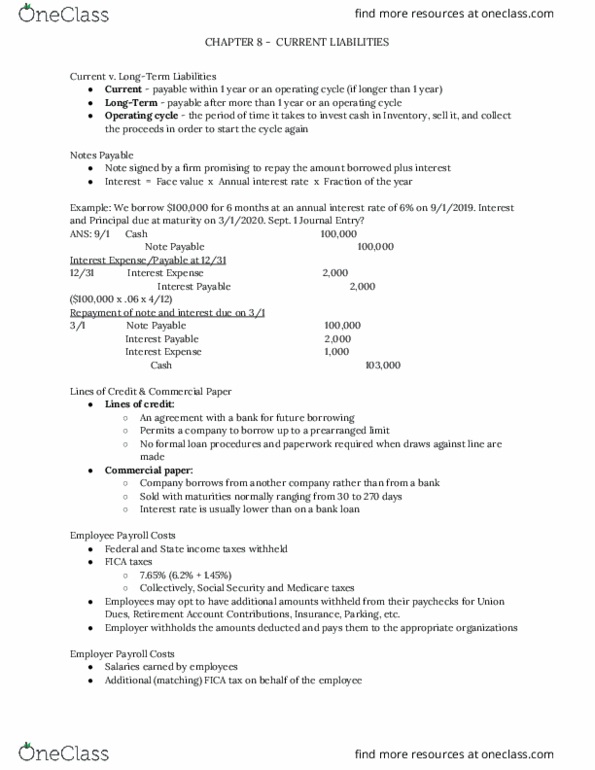

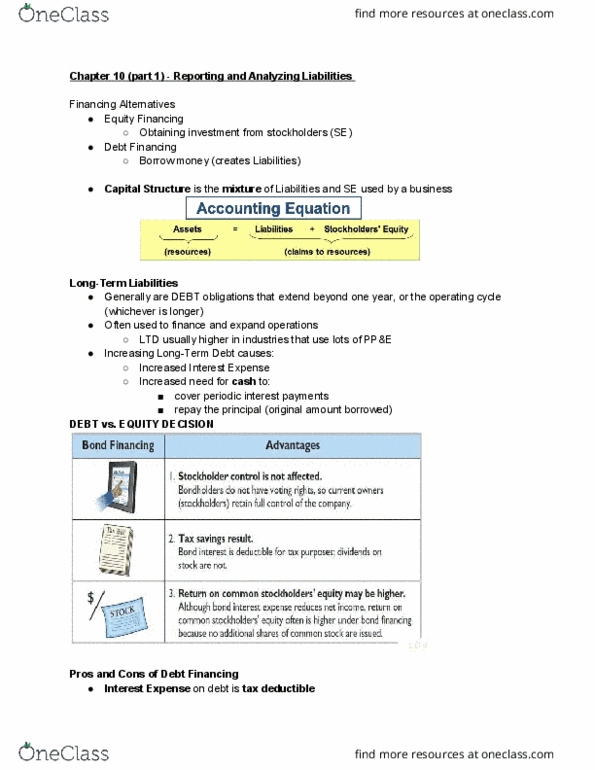

ACC 210 Lecture Notes - Lecture 8: Cash Flow, Savings Account, Working Capital

Chapter 8 Notes

• Current vs Long-term liabilities

o Current

▪ Payable within one year of an operating cycle

o Long-Term

▪ Payable after more than one year of an operating cycle

o Operating cycle

▪ Period of time it takes to invest cash in inventory, sell it

and collect the proceeds in order to start the cycle again

• Notes payable

o Note signed by a firm promising to repay the amount borrowed

plus interest

o Interest on notes is calculated as

▪ Interest = Face Value x annual interest rate x fraction of

the year

• Lines of credit

o An agreement that permits a company to borrow up to a

prearranged limit without having to follow formal loan

procedures and prepare paperwork

▪ Notes payable is recorded each time the company borrows

money under the line of credit

• Commercial Paper

o If a company borrows from another company rather than from a

bank

o Recording same as above

find more resources at oneclass.com

find more resources at oneclass.com

2

o sold with maturities normally ranging from 30 to 270 days

o interest rate on commercial paper is usually lower than on a

bank loan

o commercial paper has thus become an increasingly popular way

for large companies to raise funds.

• Employee Payroll Costs

o Federal and state income taxes withheld

o FICA Taxes

▪ 7.65%

▪ Collectively, social security and medicare taxes

o Employees may opt to have additional amounts withheld from

their paychecks for union dues, retirement acct contributions,

insurance, parking, etc.

o Employer withholds the amounts deducted and pays them to

the appropriate organizations

• EmployEr Payroll costs

o Salaries earned by employees

o Additional FICA tax on behalf of the employee

o Employers also pay federal and state unemployment taxes on

behalf of its employees

▪ Federal unemployment tax act and the state

unemployment tax act

o Additional employee benefits paid for by the employer are

referred to as fringe benefits

▪ Ofte pay all or part of eployees’ isurae preius

and make contributions to retirement or savings plans

o Recording employer-provided fringe benefits

▪ Debit salaries expense (fringe benefits)

find more resources at oneclass.com

find more resources at oneclass.com