ACC 210 Lecture Notes - Lecture 7: Accelerated Depreciation, Profit Margin, Asset Turnover

Chapter 7 notes

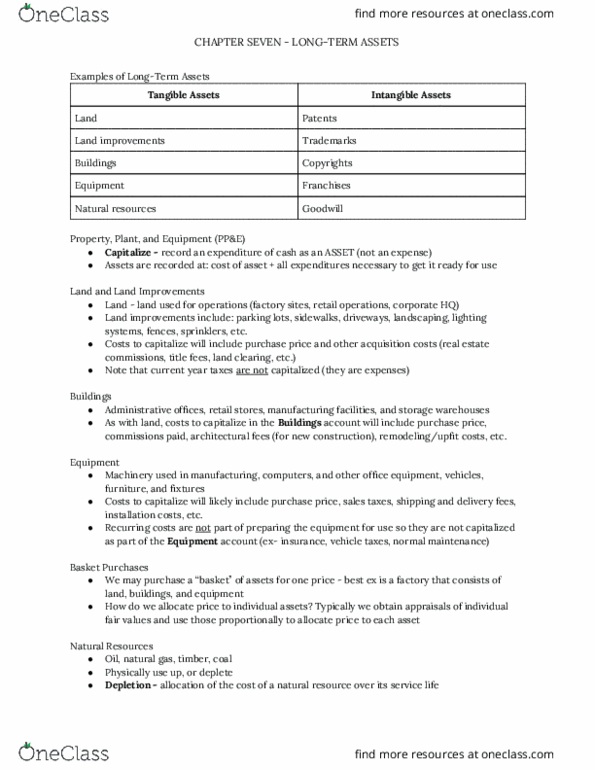

• Tangible Assets

o Land

o Land improvements

o Buildings

o Equipment

o Natural Resources

• Intangible Assets

o Patents

o Trademarks

o Copyrights

o Franchises

o Goodwill

o Lack of physical substance

▪ Existence based on a legal contract

o Acquired in 2 ways

▪ Purchase from others

• Recorded at their original cost plus all other costs

o Legal and filing fees, necessary to get the asset

ready for use

▪ Create internally

• Most of the costs are expensed to the income

statement as they are incurred

• Property Plant and Equipment

find more resources at oneclass.com

find more resources at oneclass.com

2

o Capitalize

▪ Recording an expenditure of cash as an asset (not an

expense)

o Assets are recorded at

▪ Cost of asset + all expenditures necessary to get it ready

for use

• Land and Land Improvements

o Land

▪ Used for operations (factory sites, retail operations,

corporate HQ)

o Land Improvements

▪ Parking lots, sidewalks, driveways

o Costs to capitalize will include purchase price and other

acquisition costs

▪ Real estate commissions, title fees, land clearing

o Current year taxes are not capitalized

▪ Expenses

o Depreciation is the allocation of the cost of a tangible asset over

its service life

▪ Land is an asset (do not depreciate) bc life is indefinite

▪ Do depreciate land improvements

o Buildings

▪ Administrative offices, retail stores, manufacturing

facilities, storage warehouses

• Costs to capitalize in the buildings account include

o Purchase price, commissions paid,

architectural fees, remodeling fees

find more resources at oneclass.com

find more resources at oneclass.com

3

o Equipment

▪ Machinery used in manufacturing, computers and other

office equipment

▪ Costs to capitalize will likely include purchase price, sales

taxes, shipping and delivery fees, installation costs

▪ Recurring costs are not part of preparing the equipment

for use so not capitalized in the equipment account

• Insurance, vehicle taxes, normal maintenance costs

• Basket Purchases

o Purchase of more than one asset for one purchase price

o Allocate total purchase price based on estimated individual fair

values

• Natural resources

o Oil, natural gas, timber, coal

o Physically use up or deplete

▪ Depletion: allocation of the cost of a natural resource over

its service life

o Identical to the activity based method of recording depreciation

• Patent

o Exclusive right to manufacture a product or to use a process

▪ Right for 20 years

o When a firm purchases a patent it records the patent at its

purchase price + other costs such as legal and filing fees to

secure the patent

o When a firm develops a patent internally, it expenses the

research and development costs as it incurs them

o Any legal and filing fees to get the patent are capitalized

find more resources at oneclass.com

find more resources at oneclass.com