ACCT 1201 Lecture Notes - Federal Insurance Contributions Act Tax, Accounts Payable, Quick Ratio

22 Mar 2013

School

Department

Course

Professor

Document Summary

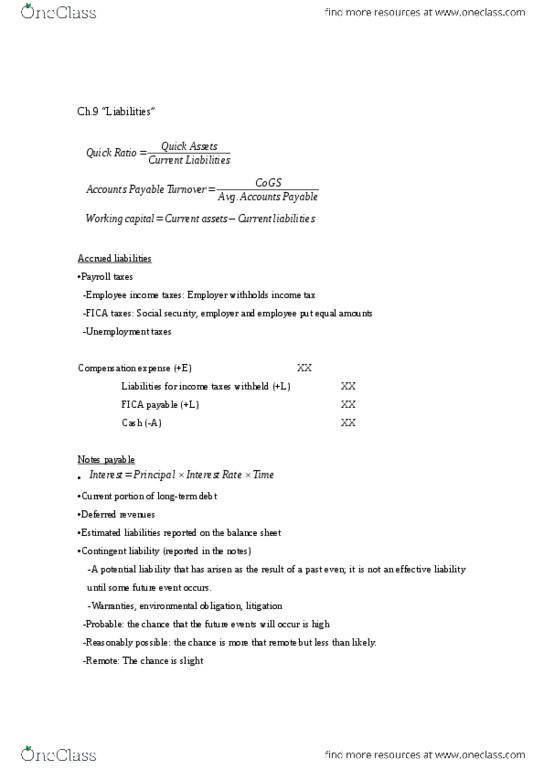

Short-term liabilities: income taxes payable, accrued compensation, payroll taxes payable***, notes payable, current portion of long-term debt, deferred revenues. Liabilities defined and classified: liabilities - are probable debts or obligations that result from past transactions, which. Quick ratio: liquidity ratio similar to current ratio, the only difference is the numerator. Quick ratio = quick assets current liabilities. Quick assets = cash + marketable securities + accounts receivable. High quick ratio normally suggests good liquidity; too high a ratio suggests inefficient use of resources. Which of the following accounts would not be considered when calculating the quick ratio: marketable securities, inventory, accounts receivable, accounts payable. A company has a quick ratio of 1. 9 before paying off a large current liability with cash. Quick assets go down / current liabilities go down. Less: credit card discounts, sales returns & allowances, sales discounts. Less: operating expenses (sg&a: rent, utilities, salaries/wages, supplies, bad debt, Less: peripheral activities (asset/goodwill impairment, gain/loss on sale)