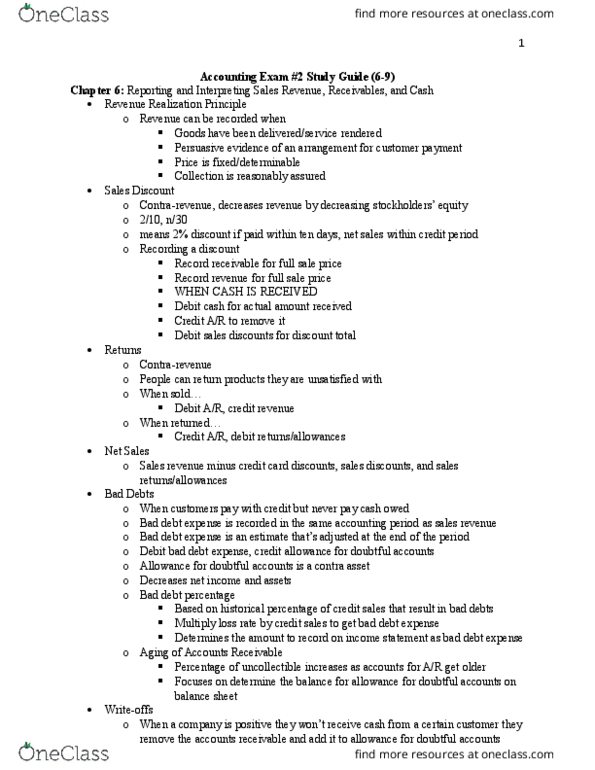

ACCT 1201 Lecture Notes - Uptodate, Income Statement

Document Summary

Get access

Related Documents

Related Questions

Czar was authorized to issue 3,000,000 shares of $1 par Common Stock but has only issued 520,000 shares of common stock as of 12/31/2018. No new shares were issued during 2018.

1. On the âAdjusting Journal Entriesâ worksheet, prepare in journal entry form all adjusting and correcting journal entries based on the following information. All information was provided to you as of 12/31/2018. (Round all numbers to the nearest dollar). Label journal entries a through t.

P- On 2,1, 2018, Czar rented a portion of one store to Pellston Inc. The contract was for 15 months and Czar required all of the cash up front. The rent is being earned equally each month. This is the only item in which rent is being earned by the company.

Q- Czar started to lease some new retail space in 2018 and added shelving and fixtures to this leased space. Based on your review of invoices, the previous accountant capitalized the cost of fixtures but did not capitalize the shipping and installation costs of $2,815. These costs were expensed and recorded as a miscellaneous selling expense. Czar has decided to use double declining balance (DDB) depreciation for this item and to take a full year of depreciation in the year of acquisition. The leasehold improvements have a useful life of 15 years with a salvage value of $12,000.

R- Czar uses the FIFO Inventory Method in valuing inventory. The inventory balance of $340,000 was based on a physical count at 12/31/2018. Based on your analysis, you have noted that $10,000 of marketing games that belonged to Pellston Inc. was included in the account. You also note that $5,600 of goods shipped to Czar f.o.b. destination were in transit on December 31, 2018 and included in the physical count.

| Czar Incorporated | ||||||

| End of Period Worksheet | ||||||

| For the Year Ended December 31, 2018 | ||||||

| Unadjusted | Adjusted | |||||

| Account Title | Trial Balance | Adjustments | Trial Balance | |||

| DR | CR | DR | CR | DR | CR | |

| Cash | 264,000 | - | ||||

| Accounts Receivable | 555,984 | - | ||||

| Allowance for Doubtful Accounts | - | 13,600 | ||||

| Interest Receivable | - | - | ||||

| Merchandise Inventory | 340,000 | - | ||||

| Prepaid Insurance | - | - | ||||

| LIFO Reserve | - | 25,600 | ||||

| Prepaid Advertising | - | - | ||||

| Prepaid Rent | 13,600 | - | ||||

| Office Supplies | 4,800 | - | ||||

| Note Receivable | 20,000 | |||||

| Available for Sale Securities | 300,000 | - | ||||

| Office Building | 3,000,000 | - | ||||

| Accumulated Depreciation - Office Building | - | 70,000 | ||||

| Storage Building | 1,020,000 | - | ||||

| Accumulated Depreciation - Storage Building | - | - | ||||

| Land | 600,000 | - | ||||

| Leasehold Improvements | 180,000 | - | ||||

| Accumulated Depreciation - Leasehold Improvements | - | - | ||||

| Office Equipment | 260,000 | - | ||||

| Accumulated Depreciation - Office Equipment | - | 52,000 | ||||

| Patent | 120,000 | - | ||||

| Accounts Payable | - | 276,000 | ||||

| Sales Tax Payable | - | - | ||||

| Salaries Payable | - | 113,600 | ||||

| Payroll Taxes Payable | - | 20,000 | ||||

| Interest Payable | - | - | ||||

| Income Tax Payable | - | - | ||||

| Unearned Rent Revenue | - | - | ||||

| Loan Payable - First Trust | - | 520,000 | ||||

| Loan Payable - Coldwell Bank | - | 1,600,000 | ||||

| Common Stock | - | 520,000 | ||||

| Additional Paid in Capital | - | 1,599,000 | ||||

| Retained Earnings | - | 736,000 | ||||

| Accumulated Other Comprehensive Income | - | 20,000 | ||||

| Dividends | 67,800 | - | ||||

| Sales | - | 3,622,560 | ||||

| Sales Returns and Allowances | 33,800 | - | ||||

| Sales Discounts | 15,400 | - | ||||

| Cost of Goods Sold | 1,583,600 | - | ||||

| Sales Salaries Expense | 349,120 | - | ||||

| Office Salaries Expense | 219,200 | - | ||||

| Advertising Expense | 12,800 | - | ||||

| Depreciation Expense - Office Building | - | |||||

| Depreciation Expense - Leasehold Improvements | - | - | ||||

| Depreciation Expense - Office Equipment | - | - | ||||

| Leasing Expense - Stores | 105,600 | - | ||||

| Miscellaneous Selling Expense | 18400 | - | ||||

| Research & Development Expense | 12,000 | |||||

| Rent Expense - Storage Facility | - | - | ||||

| Insurance Expense | 12,000 | - | ||||

| Office Supplies Expense | 28,000 | - | ||||

| Miscellaneous Administrative Expense | 7,336 | - | ||||

| Rent Revenue | - | 60,000 | ||||

| Interest Revenue on Note Receivable | - | - | ||||

| Dividend Revenue on AFS Securities | - | 20,000 | ||||

| Interest Expense | - | - | ||||

| Bad Debt Expense | 28,000 | - | ||||

| Amortization Expense | - | - | ||||

| Income Tax Expense | - | - | ||||

| Payroll Taxes Expense | 96,920 | - | ||||

| Rebate Expense | - | - | ||||

| Unrealized holding loss | - | - | ||||

| Depreciation Expense-Storage Building | - | - | ||||

| Loss on Impairment | - | - | ||||

| Rebate Liability | - | - | ||||

| Restricted Cash for Future Expansion | - | - | ||||

| 9,268,360 | 9,268,360 | |||||

| Company Background & Scenario | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The Auto Zone Company is a well-established, publicly-held corporation, operating as a wholesaler in the auto parts industry. Specifically, Auto Zone purchases auto parts from manufacturers and sells them to large business customers. Most purchases and sales are on account, with trade credit terms (specified below). | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Youâre a Davenport University student pursuing a bachelorâs degree in business and employed at the Auto Zone Company this semester as an intern. Youâve worked in various departments and on several projects so far, learning a lot about the companyâs business operations. Management seems impressed with your enthusiasm and the quality of your work. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| The companyâs accountant has just been called away for a family emergency and will likely be absent for a month or so. The General Manager asks you to take over the accountantâs regular duties on an interim basis. Youâre nervous about doing so, but are confident that what youâve learned in accounting class, plus your personal problem-solving skills, will make this a successful experience. What a great learning opportunity, not to mention an enhancement to your resume! | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Part I | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Journal Entries | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| a. Within the "Transactions" worksheet you will find journal entry statements. Use those statements to write the corresponding journal entries. You are to write the journal entries in the proper special journal. The special journals included within this workbook include the Sales Journal, Purchases Journal, Cash Receipts Journal and Cash Payments Journal. Any transaction that does natually work within one of the special journals should be written into the General Journal. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| b.Within the "Transactions" worksheet you will find journal entry statements. At the end of this list you will find "adjusting" information. Use this "adjusting" information to write the respective adjusting journal entries. Write all adjusting entries in the worksheet labled "General Journal ADJ". | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| c. Before starting work, review the entire project: all instructions, business transactions descriptions, workbook sections, check figures, due dates, and submission requirements. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Credit Terms & Inventory Accounting | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| a. When Auto Zone purchases merchandise from a supplier or vendor on account, they receive credit terms of 2/15, net 30. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| b. When Auto Zone sells merchandise to a customer on account, they offer that customer credit terms of 2/30, net 45. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| c. Auto Zone uses a perpetual inventory accounting system and a last-in, first-out (LIFO) inventory costing method. Within this workbook there is a worksheet labeled "Inventory Control". You will need to use the "Inventory Control" worksheet to keep a perptual record of your inventory. As part of that process you will be calculating the value of CGS each time you generate a sale. Use the "Inventory Control" worksheet to calcluate your Cost of Goods Sold values. | |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| d. Auto Zone uses the "Gross" method of accounting for purchases and sales. The "Net" method assumes that discounts are taken at the point of sale or purchase.

| |||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||||