ECON-UA 1 Lecture Notes - Exogeny, Economic Equilibrium, Price Floor

8 May 2014

School

Department

Course

Professor

Document Summary

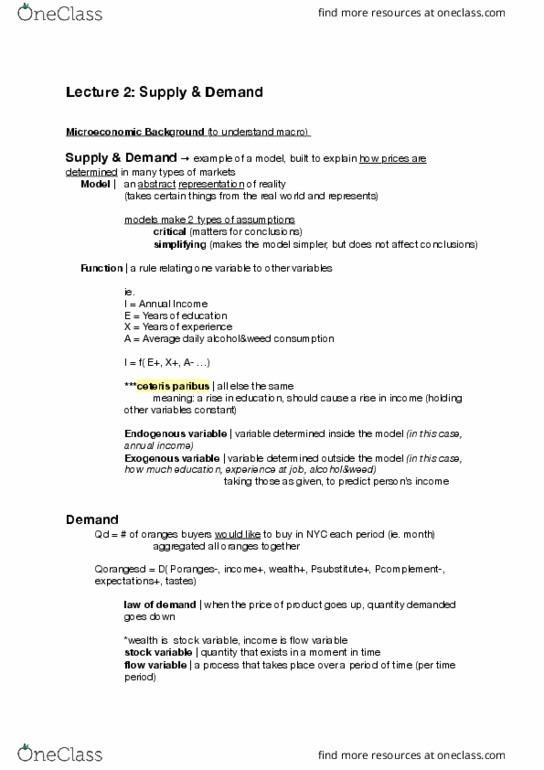

Economic model has two types of variables: exogenous: variable determined outside of model treat it as a given, don"t try to explain it, endogenous: variable determined in the model the reason for building the model. Price and quantity and endogenous variables, all others are exogenous. Equilibrium is a set of values for endogenous variables that won"t change unless exogenous variable changes. is the equilibrium price, qe is equilibrium demand. One or more exogenous variables and observe change in our endogenous variables. Suppose income rises: leads to a rise in equilibrium price and quantity. Suppose price of oil increases: leads to a rise in equilibrium price and decrease in equilibrium quantity. Suppose people think the price of gas will rise: raises equilibrium price but equilibrium quantity could go up or down. Price floor: a minimum price at which a product is allowed to sell makes things better for sellers (usually only used for agricultural products)