ACCTMIS 2300 Lecture 8: Standard Costing Notes

29 Oct 2017

School

Department

Course

Professor

Document Summary

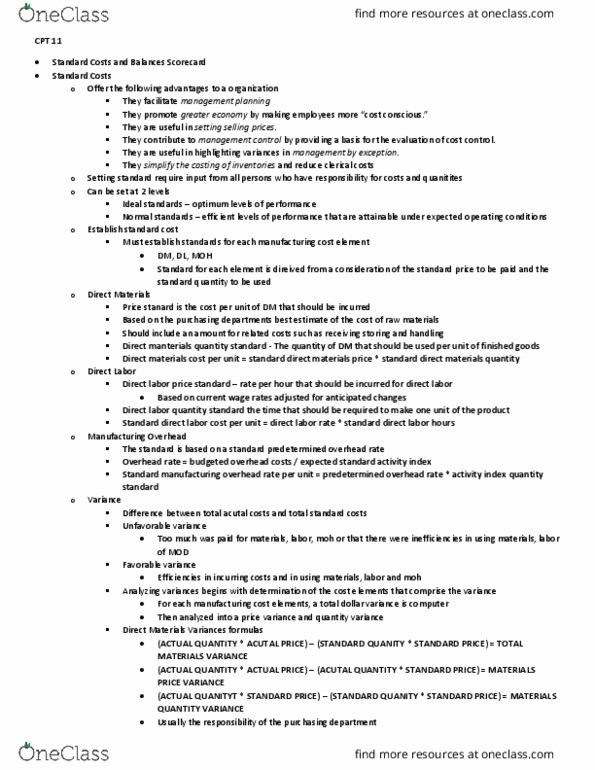

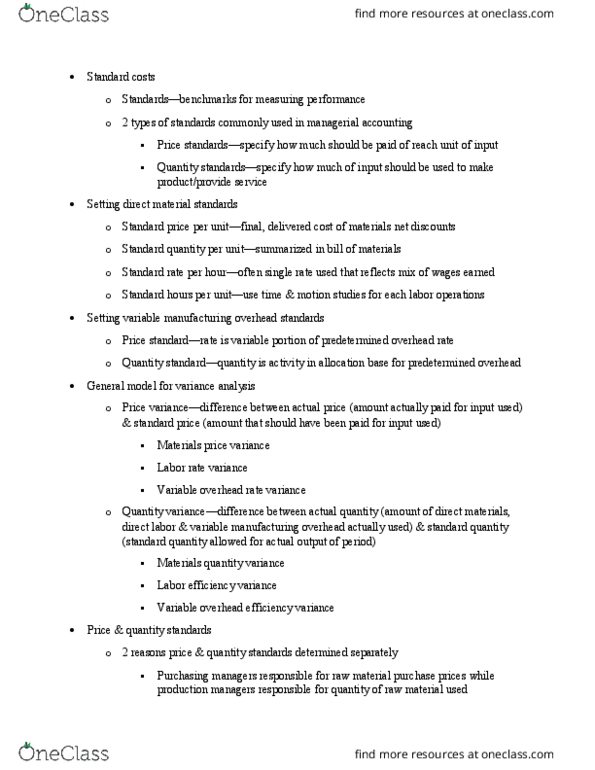

How much we should pay for an input. How much input we should use to make product or provide service. Variable manufacturing costs that have standards a) b) c) Detailed list of standards to make a unit of your product. Any differences deemed significant are brought to management. Price variance: difference between actual price and standard. Quantity variance: difference between actual quantity vs standard. Determined separately b/c: different managers responsible for buying and then using these inputs. Also buying and using activities occur at different points in time. Price variance: (aq * ap) - (aq*sp) b) Aq = actual quantity of dm purchased! i) ii) iii) iv) v) Quantity variance: (aq * sp) - (sq * sp) i) ii) iii) Aq = actual quantity of dm used in. Sq = (standard quantity of dm per unit * number of units produced) Rate variance: (ah * ar) - (ah * sr) i) ii) iii) iv)