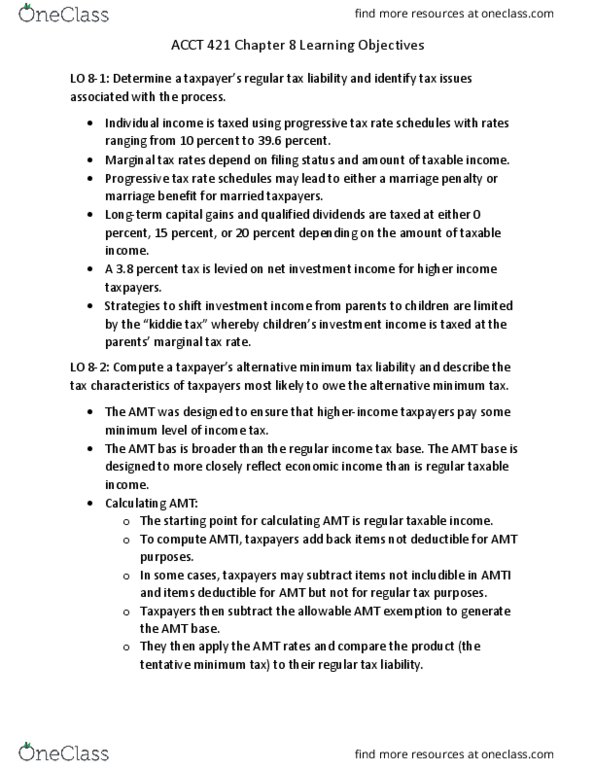

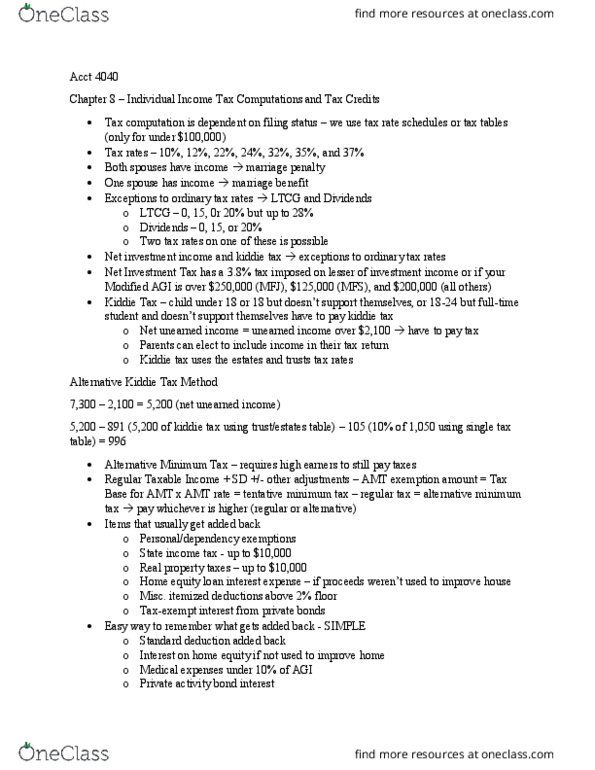

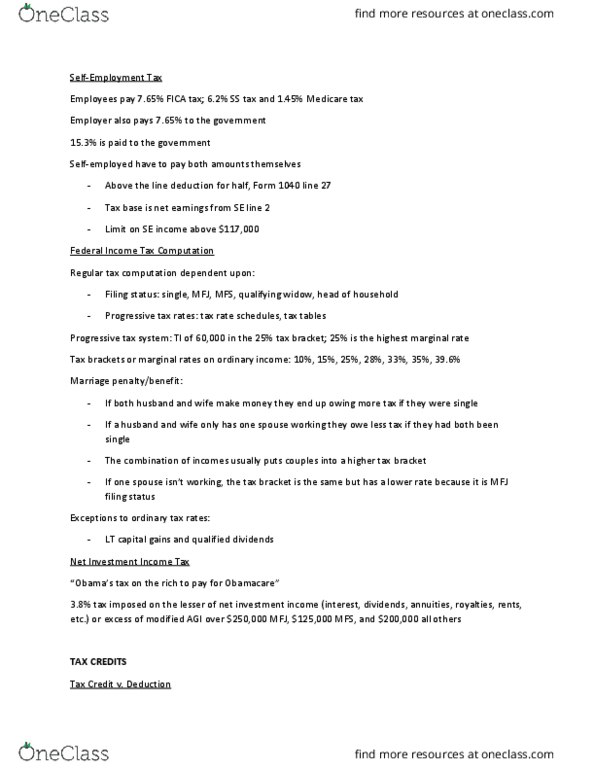

from South Western Individual income Tax 2016 vol 39

Chapter 4, problem 58

58. Daniel B. Butler and Freida C. Butler, husband and wife,file a joint return. The Butlers live at 625 Oak Street in Corbin,KY 40707. Danâs SSN is 111-11-1111, and Frediaâs is 123-45-6789.Dan was born on 01/15/1964. Frieda was born on August 20, 1965.

During 2014 Dan and Freida furnished over half of the totalsupport of each of the following individuals, all of whom stilllive at home:

Gina, their daughter 22 a full time student who married on12/21/14 has no income of her own and for 2014 did not file a jointreturn with her husband Casey, who earned $10,600.00 during 2014.Ginaâs SSN is 123-45-6788

Sam their son is 20 who had a gross income of 6300 in 2014dropped out of college in October 2014. He had graduated highschool in May 2014. Samâs SSN is 123-45-6787.

Ben their oldest son age 26 is a full time graduate student withgross income of 5200. Benâs SSN is 123-45-6786

Dan was employed as a manager by WJJJ, Inc. EIN # 11-11111111,604 Franklin Street Corbin KY 40702, and Freida was employed as asalesperson for Corbin Realty KY 40701. Selected information fromthe W-2 forms provided by the employers is presented below. Dan andFreida use the cash method.

Line Description Dan Freida

1 Wages,tips, othercompensation 74,000 86,000

2 Federal income taxwithheld 11,000 12,400

17 State income taxwithheld 2,960 3,440

Freida sold a house on 12/30/14 and will be paid a commission of$3100(not included in the 86k reported on W-2) on the January 10,2015 closing date.

Other income (as reported on 1099forms) for 2014 consisted of the following:

Dividends on CSX stock (qualified) $4,200

Interest on savings at Second Bank 1,600

Interest on City of Corbinbonds 900

Interest on First BankCD 382

The 382 from First Bank was original issue discount. Dan andFreida collected 16k on the First Bank CD that matured on 09/30/14.The CD was purchased on 10/1/12 for $14,995.00 and the yield tomaturity was 3.3%

Dan received a Schedule K-1 from Falcon Partnership which showedhis distribution share of income as $7,000.00. In addition to theabove information, Dan and Freidaâs itemized deductions includedthe following:

Paid on 2014 Kentucky incometax 700.00

Personal property taxpaid 600.00

Real estate taxespaid 1,800.00

Interest on home mortgage (CorbinS&L) 4,900.00

Cash contributions to the BoyScouts 800.00

Sales tax from the sales tax table is $1,860. Dan and Freidamade estimated tax payments of $8000.00. The Kentucky income taxrate is 4%.

Part 1- Tax Computation

Compute Dan and Freidaâs 2014 income tax payable (or refund due)If you use tax forms for the computations you will need Form 1040and Schedules A, B and E. Suggested software H&R BLOCK Taxsoftware

Part 2 Tax Planning

Dan plans to reduce his work schedule and only work half timefor WJJJ in 2015. He has been writing songs for several years andwants to devote his time to developing a career as a songwriter.Because of the uncertainty in the music business, however, he wouldlike you to make all computations assuming that he will have noincome from song writing in 2015. To make up for the loss of incomeFreida plans to increase the amount of time she spends selling realestate. She estimates that she will be able to earn $90k in 2015.Assume that all other income and expense items will beapproximately the same as they were for 2014. Assume that Sam willbe in enrolled in college as a full time student for the summer andfall semesters. Will the Butlers have more or less disposableincome (after Federal income tax) in 2015? Write a letter to theButlers that contains your advice and prepare a memo for the taxfiles.