ACC 203 Lecture Notes - Lecture 3: Income Statement, Internal Revenue Service, Financial Statement

2 Mar 2017

School

Department

Course

Professor

Document Summary

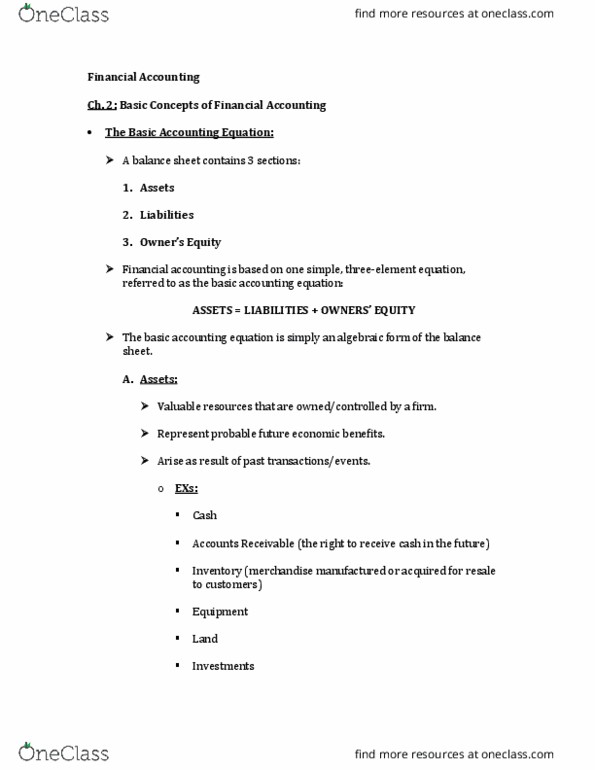

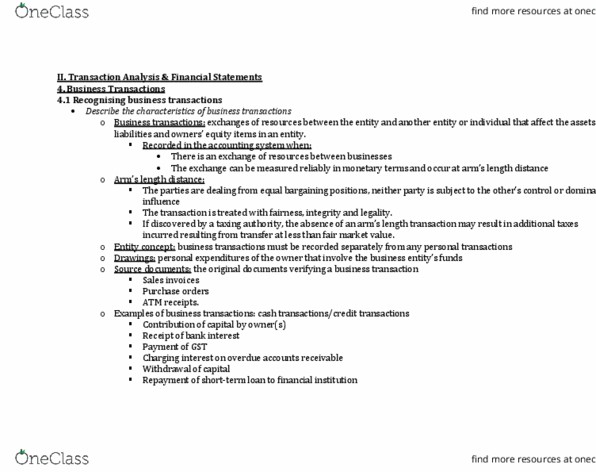

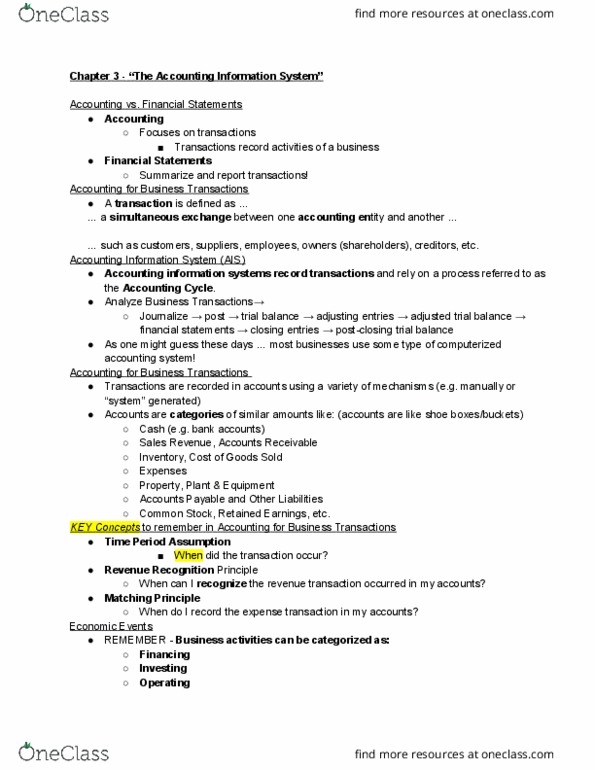

The financial accounting process: categorizing past transactions & events. Places transactions & events into categories that reflect their type/nature. Some of these categories include: purchases of inventory (merchandise acquired for resale), sales of inventory, wage payments to workers, measuring selected attributes of those transactions & events. The attribute measured is fair value of transaction on exchange date. Usually indicated by amount of cash that changes hands: ex: if equipment is purchased for k & paid w/ cash, the equipment is valued at k. The initial valuation is not subsequently changed. Original measure is called historical cost: recording & summarizing those measurements. Summarizing is necessary b/c otherwise decision makers would be overwhelmed w/ extremely large array of info. Financial statements: the end result of financial accounting process. Firms prepare 3 major financial statements: balance sheet: shows firm"s assets, liabilities & owner"s equity. Accounts receivable: amounts owned to company/firm by its customers; have value b/c they represent future cash inflows.