ACCTG 211 Lecture Notes - Lecture 4: Accrual, Income Statement, Financial Statement

Document Summary

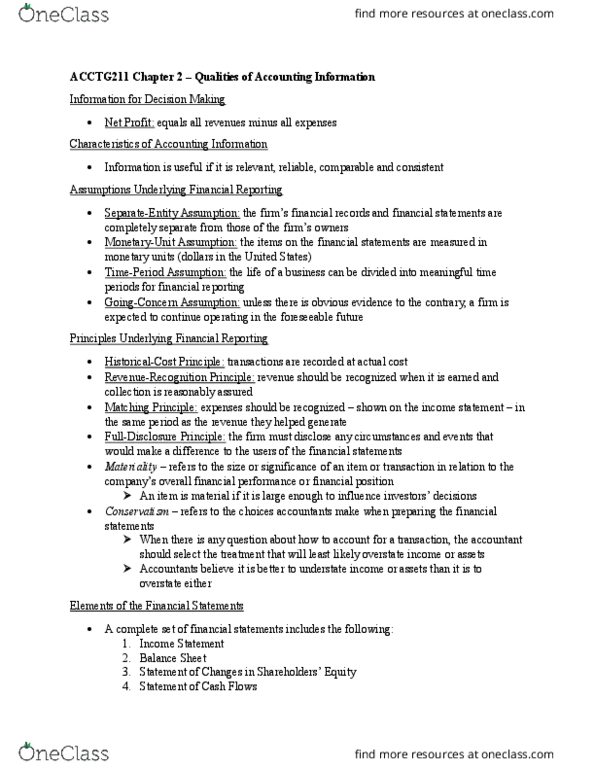

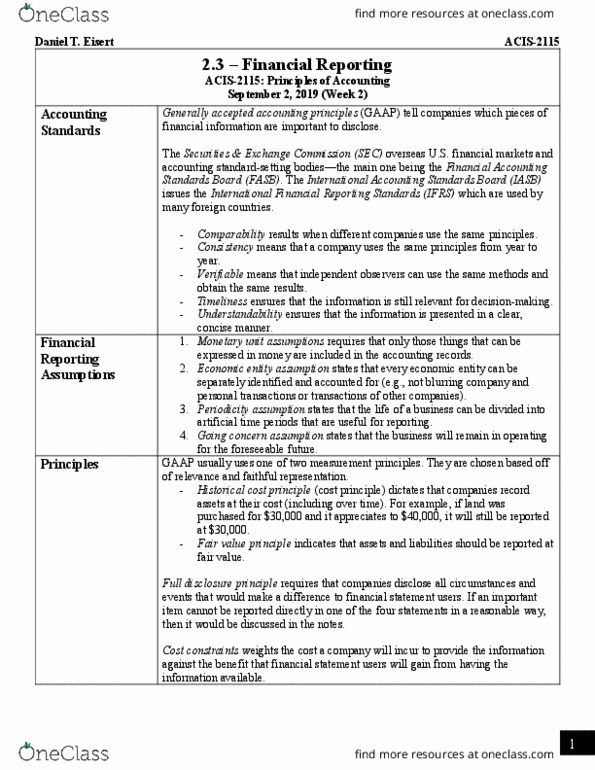

Acctg 211 - lecture 4 - qualities of accounting information & accruals and deferrals. The rules most companies follow in preparing financial. U. s. gaap is detailed, technical, and rules based. International financial reporting standards (ifrs) are characterized as concepts-based. One year or one operating cyclewhichever is longer ; for class - one year, if less than one year - current. Consistent - compare performance one year to next. Separate-entity assumption - firm"s financial records are separate from firm"s owners. Monetary-unit assumption - items measured in monetary units (dollars in u. s. ) Time period assumption - life of business divided into time periods. Going-concern assumption - firm expected to continue operating in foreseeable future. Historical cost - assets are recorded at cost. Revenue recognition - revenue is recognized when it is earned. Matching principle - recognize expenses in the same period as the revenue they help generate.